Welcome to the latest edition of Dividend Hunter. Over the past few weeks, we have analyzed companies in which strong cash flows could translate into consistent dividends going forward. In our previous edition, we covered an MNC tech giant offering 4.5% yield. In this edition of Dividend Hunter, we analyze the India-listed subsidiary of another MNC tech giant that has long generated cash and has once again resumed dividend payout.

Our Dividend Hunter stock of this week is capitalizing on the global pivot toward cloud infrastructure and artificial intelligence (AI). Thus, legacy modernization is a major ongoing theme.

This is especially true in the Banking, Financial Services, and Insurance (BFSI) sector, where companies are upgrading their legacy core banking platforms by adopting cloud technologies and generative AI.

However, this shift poses risks, as deploying advanced models or upgrading core banking platforms leaves no room for error. This is because reliability and security are just as important as speed.

This exact need creates an opportunity for specific sets of technology companies. While many players focus purely on building software, a select few specialize in ensuring those complex systems actually work flawlessly.

One strong player in this niche is Expleo Solutions Limited.

Expleo is part of the Expleo Group and is effectively a subsidiary of Expleo Technology Germany GmbH (the German entity within the group).

Expleo sits right at the critical juncture of quality assurance and digital transformation. It helps global financial institutions, aerospace companies, and automotive giants safely shift to modern operating models by infusing AI.

It does not just build technology. Expleo specializes in digital assurance and software validation to ensure every innovation withstands intense scrutiny. This helps catch flaws before they become costly failures.

Expleo’s business model translates into financial strength. Thanks to a surging demand for their specialized testing and AI-backed validation services, they are generating high cash flows and maintaining a pristine balance sheet.

Even better, they are actively sharing this wealth with investors. Recently, they declared an interim dividend of ₹50 per share.

But will such a payout be sustainable? Let’s find out.

The BFSI Growth Engine Defying Sector Slowdown

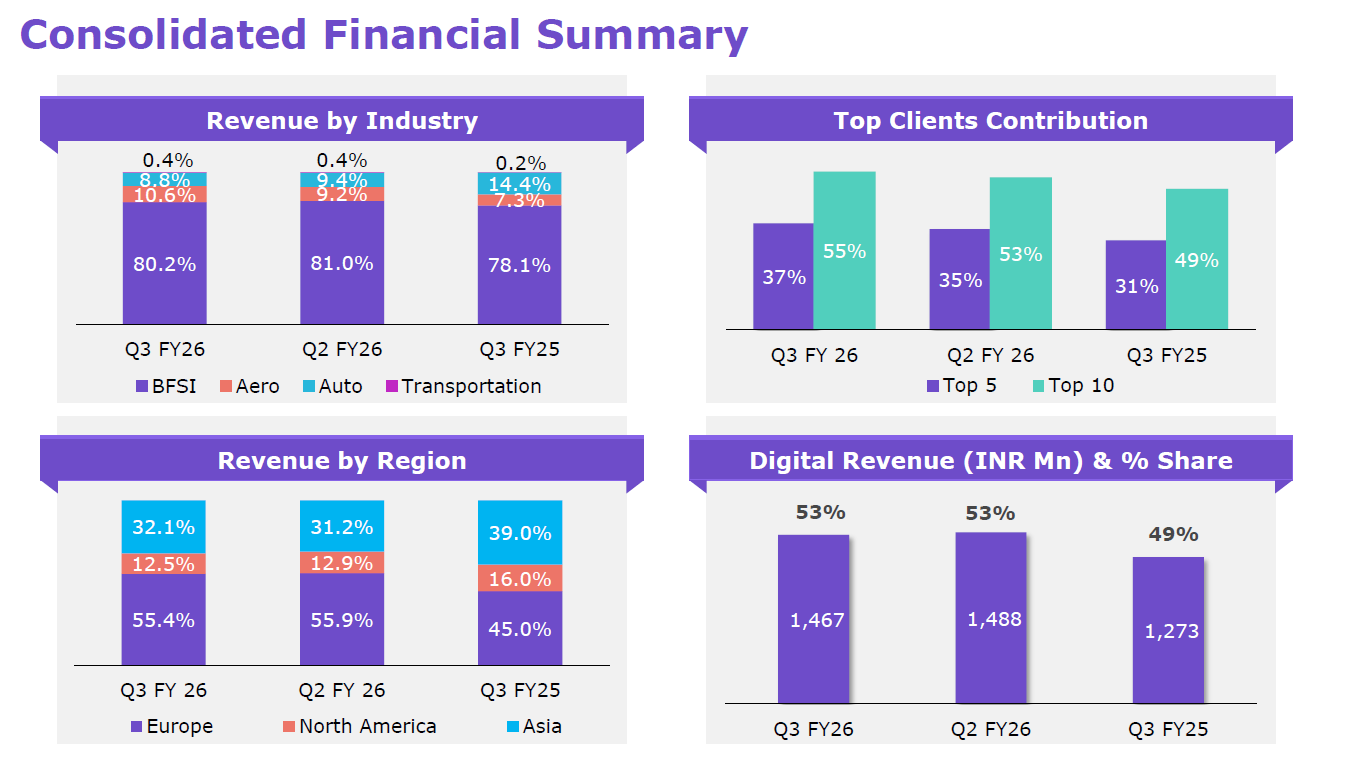

Expleo Solutions is a global leader in providing engineering and quality assurance solutions. In Industry-mix, it primarily serves the Banking, Financial Services, and Insurance (BFSI) sector, which contributed 80% of revenue in Q3FY26.

Key Performance Indicators

Aerospace (10.6%), Auto (8.8%), and Transportation (0.4%) account for the remaining 20%. The company has 203 active clients. 30 customers contribute revenue above US$1 million in the rolling 12-month period, and 11 contribute between US$ 0.5 and US$ 1 million.

The Client Concentration Risk: A Double-Edged Sword

However, it has a high client concentration. The top 5 clients account for 37% of revenue, and the top 10 (55%). Thus, a loss of any client could impact its financials.

Europe is the largest region, contributing 55.4% of revenue, followed by Asia (32.1%) and North America (12.5%). The company’s operations are effectively divided into two main growth engines: Digital Services and Engineering Services.

Digital Services vs. Engineering: The Margin Story

The digital services segment has become a major growth driver for Expleo, accounting for over half (53%) of its total revenue.

This includes comprehensive AI and cloud transformations, featuring industry-leading internal platforms such as Expleo Sophia and Teresa.

This is a highly profitable area that allows the company to scale its revenues significantly without requiring proportional increases in headcount, a win for profitability.

To this end, the strong global backing and positioning of its German parent organization, Expleo Technology, provides an advantage in securing top-tier clients, particularly for mission-critical legacy modernization deals.

This success is supported by advanced quality assurance and digital resilience solutions that leverage AI, machine learning, and deep data analytics. This aims to detect system flaws, manage risk, and deliver better customer experiences.

On the other hand, their core engineering division provides expert consulting, testing services, and intelligent automation. The segment guides global firms in navigating shifts in information technology and cloud migrations.

FY25 Profitability Audit: The 17.7% Margin Secured the ₹50 Dividend

The company’s market cap is ₹1,264 crore, as of 30 April 2026.

Expleo Share Price

Over the last 3/5 years, net profit grew at a 14%/21% CAGR, reaching ₹103 crore in FY25.

Gross operating revenue in FY25 rose by 6% year-on-year to ₹1,025 crore. What is even more impressive is how efficiently Expleo managed its operations to drive profitability.

The company’s EBITDA (Earnings Before Interest, Tax, Depreciation and Amortisation) surged 17% to ₹182 crore, while margin expanded by 160 bps to 17.7%. This operational growth trickled down to the bottom line, with net profit jumping 14% to ₹103 crore.

So what exactly is driving this growth for Expleo?

First and foremost is their strategic pivot toward digital innovation. For FY25, digital services accounted for 48% of total business. The revenue contribution has even increased to 53% in Q3FY26.

Global clients are increasingly relying on Expleo for complex application modernization, AI integration, and secure cloud services. This shift is not just bringing in more revenue but is also highly profitable for the business.

Sector Diversification: Decoding the 51% Surge in Retail Revenue

Secondly, their domain expertise is translating into outstanding growth across key industries. While the broader technology market faced headwinds, Expleo saw a 25% growth in its Banking segment.

The Insurance segment followed closely with a 27% growth, while the Retail and Consumer Goods space grew by 51%.

9MFY26 Performance Audit

Financials were also good in 9MFY26. Revenue increased 7% year-over-year to ₹822 crore. Operating profit increased 2% to ₹123 crore, while margins fell 60 bps to 15%. As a result, net profit, however, increased by just 4% to ₹79 crore.

Capital Efficiency at Scale

The company’s return ratios are better than the industry median. Return on Capital Employed stood at 21.8% (against the industry median of 16.4%) in FY25, while Return on Equity stood at 16.6% (against 12.5%). A key highlight of Expleo is its Return on Investment (ROI) of 35.5%, up from just 0.4% previously.

Treasury Management: Turning Surplus Cash into a 35% ROI Engine

The management attributes this ROI directly to new investments made in mutual funds. This allowed them to earn returns on their surplus treasury funds rather than keeping cash idle.

Like other IT companies, Expleo also operates a lean business model with absolutely zero debt on its balance sheet. This means they don’t have interest burdens eating into their profits.

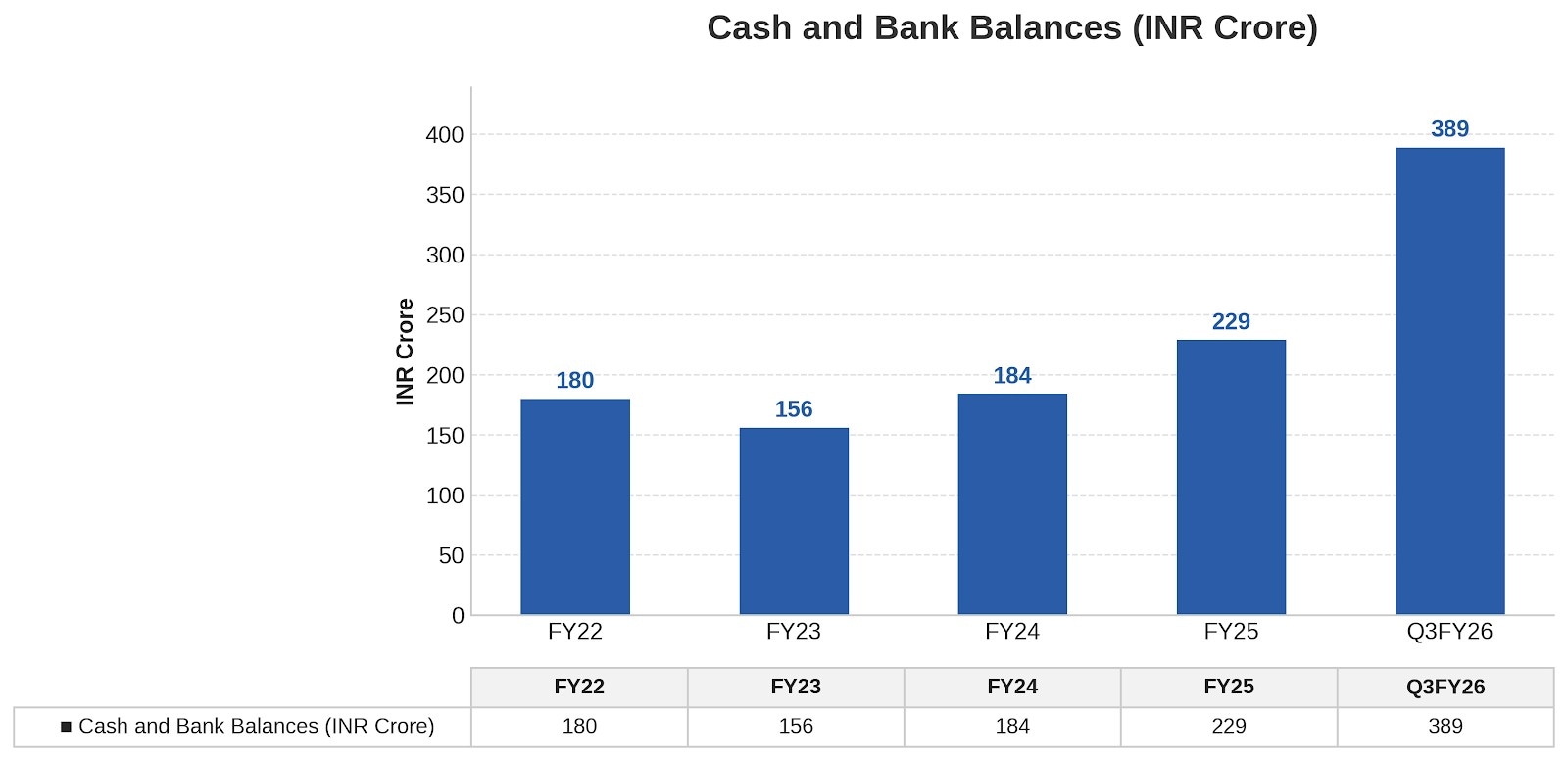

The Growing Cash Balance

This directly translates into a high cash flow. Expleo boasts a net cash position of ₹389 crore as of Q3FY26, up from ₹303 crore in Q2FY26 and ₹350 crore in Q3FY25. This reflects that Expleo is generating constant cash.

Source: Annual Report/Investor Presentation

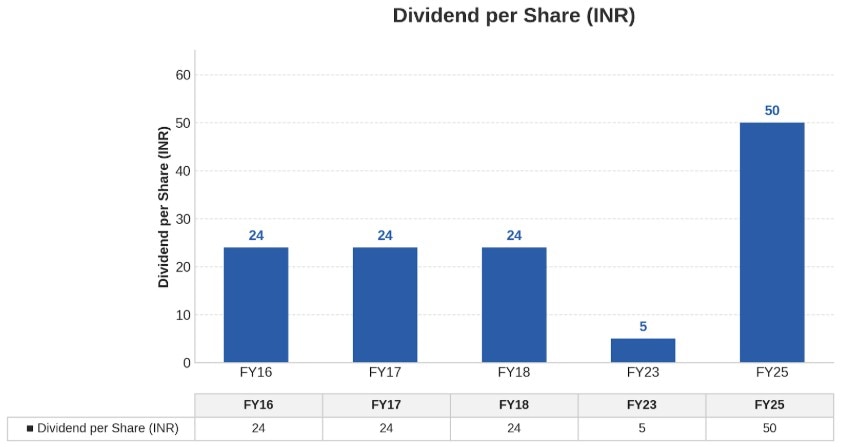

With such cash flows, the company paid an interim dividend of ₹50 per share for FY25. This translates to a dividend yield (at a price of ₹814 per share) of 6.1% in FY25. The FY25 payout was a massive increase from ₹5 per share declared in FY23.

Dividend Per Share

Historically, Expleo had a consistent track record of dividend payments until FY18. It returned ₹24 per share consistently from FY16 to FY18. However, after that, it stopped paying dividends to shareholders, likely due to stagnant growth. As growth returned in FY21, it paid dividends in FY23 and FY25.

This also means that dividend payouts can be volatile going forward.

The M&A Wildcard: Balancing Dividend Against Q1FY27 Acquisitions

According to management, future dividend payouts will be balanced against ongoing evaluations of potential acquisitions. This is because the leadership is actively putting this capital to work to fuel inorganic growth.

They have narrowed down their merger and acquisition targets to a couple of specific assets and are currently doing due diligence. A final decision on these strategic acquisitions is expected by Q1FY27.

These acquisitions can fill capability gaps, such as new geographies or adding niche service lines. Thus, any subsequent dividend payout will align with the CapEx for these strategic acquisitions.

Operational Resilience: The Roadmap to 100% AI Literacy by FY27

As said above, the core engine powering Expleo’s growth is its pivot toward AI. Legacy modernization is a major ongoing theme, especially in BFSI, where institutions are upgrading their legacy core banking platforms.

To ensure they remain the absolute market leaders in quality assurance, Expleo is deeply integrating AI from test case generation through execution.

To support this technological transition, Expleo aims to make 100% of its workforce AI literate by the end of FY27. This ensures they can fulfill complex client demands internally without hunting for expensive outside talent.

Valuation Arbitrage: Comparing Expleo’s 10.8x P/E to Sector Peers

Valuation-wise, Expleo trades at a price-to-earnings (P/E) multiple of 10.8x, at a discount to the 10-year historical median of 16.2x. The valuation is not just a discount to the industry P/E (26.0) but also to larger domestic peers such as Black Box (41.5), Affle 3i (45.7), and Tata Tech (36.0).

The “Dividend Hunter” Verdict: Is This a Long-Term Income Fortress?

Expleo meets the key Dividend Hunter filters. It has shown strong profit growth despite turbulent sectoral trends, strong cash flows, and a payout ratio within thresholds.

Given a yield of 6.1%, consistent increases in cash flow, an asset-light business model, and a resumption of dividend payments, it appears likely that the dividend payout trend will continue. However, acquisitions (if any) could divert cash, potentially slowing the payout and, at worst, even stalling once again.

Nonetheless, Dividend hunters should add this stock to their watchlist and see if it continues to reward shareholders with a lucrative dividend yield.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data were unavailable have we used an alternative, widely accepted, and widely used source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.