In this edition of Dividend Hunter, we analyze a Navratna-turned-Maharatna public-sector giant that is a major financier of India’s modernizing economy. This company has consistently generated strong cash flows and has just paid a 5.4% dividend yield following higher annual net profits.

With ambitious national targets to become a developed nation by 2047, the build-up of physical infrastructure and the expansion of the manufacturing base are in full swing.

As infrastructure scales, the demand for energy is rising rapidly. Data centers are also triggering a ₹3 lakh crore grid upgrade.

Why India’s Energy Transition Drives Capital Deployment

To meet this demand and fulfill its ‘Panchamrit’ climate commitments, India aims to scale its renewable energy capacity, targeting 500 gigawatts (GW) of non-fossil fuel capacity by 2030. As of 31 March 2026, with a capacity of 283.5 GW, India ranks as the world’s third-largest renewable energy market.

Furthermore, modernization efforts like the Revamped Distribution Sector Scheme and the PM Surya Ghar Muft Bijli Yojana are completely reshaping India’s power grid. This exact need creates an opportunity.

While engineering and construction players focus on building physical assets such as solar parks, metro lines, and smart grids, they cannot operate without the most fundamental raw material of all: Capital.

REC: One of India’s Largest NBFCs

One dominant market player in this niche is REC Limited, which ensures that this capital is mobilized and deployed.

REC is a Maharatna Central Public Sector Enterprise (CPSE) under the Ministry of Power. It is a systemically important Non-Banking Financial Company (NBFC) and is among India’s largest Infrastructure Finance Companies.

Operational Profile: The Nodal Machinery for Infrastructure Capital

REC sits right at the critical juncture of energy security, climate transition, and industrial growth. It provides cost-effective, long-term funding to power utilities and private-sector developers to scale their operations.

It doesn’t just lend money. It serves as a key nodal agency for government-led power sector schemes. It is now diversifying into non-power sectors, including metro rail, airports, roads, highways, ports, and healthcare facilities.

This ensures that the country avoids capital bottlenecks across major growth sectors. This strength translates into stable financial growth, driven by surging demand for infrastructure development. It generates strong profitability while maintaining a clean balance sheet.

On top of that, REC pays out almost 30% of its net profit as dividends to shareholders. It boasts a track record of consistent dividend payments and even increasing the payout every year. For instance, for FY25, REC paid a total dividend of ₹18.00 per equity share, and even increased that in FY26.

But as REC rapidly scales its loan book into new domains like green hydrogen, electric mobility, and non-power logistics, will these cash flows and dividend payments remain sustainable in the long run?

Core Product Suite: Driving Smart Metering and Solar Mandates

At its core, REC mobilizes funds at competitive rates from both the domestic and international markets. It then lends these funds as interest-bearing loans to state electricity boards, power utilities, and private sector developers.

The company offers a suite of financial products for large-scale development. This includes Long-Term Loans, Short- and Medium-Term Loans & Working Capital, and Debt Refinancing.

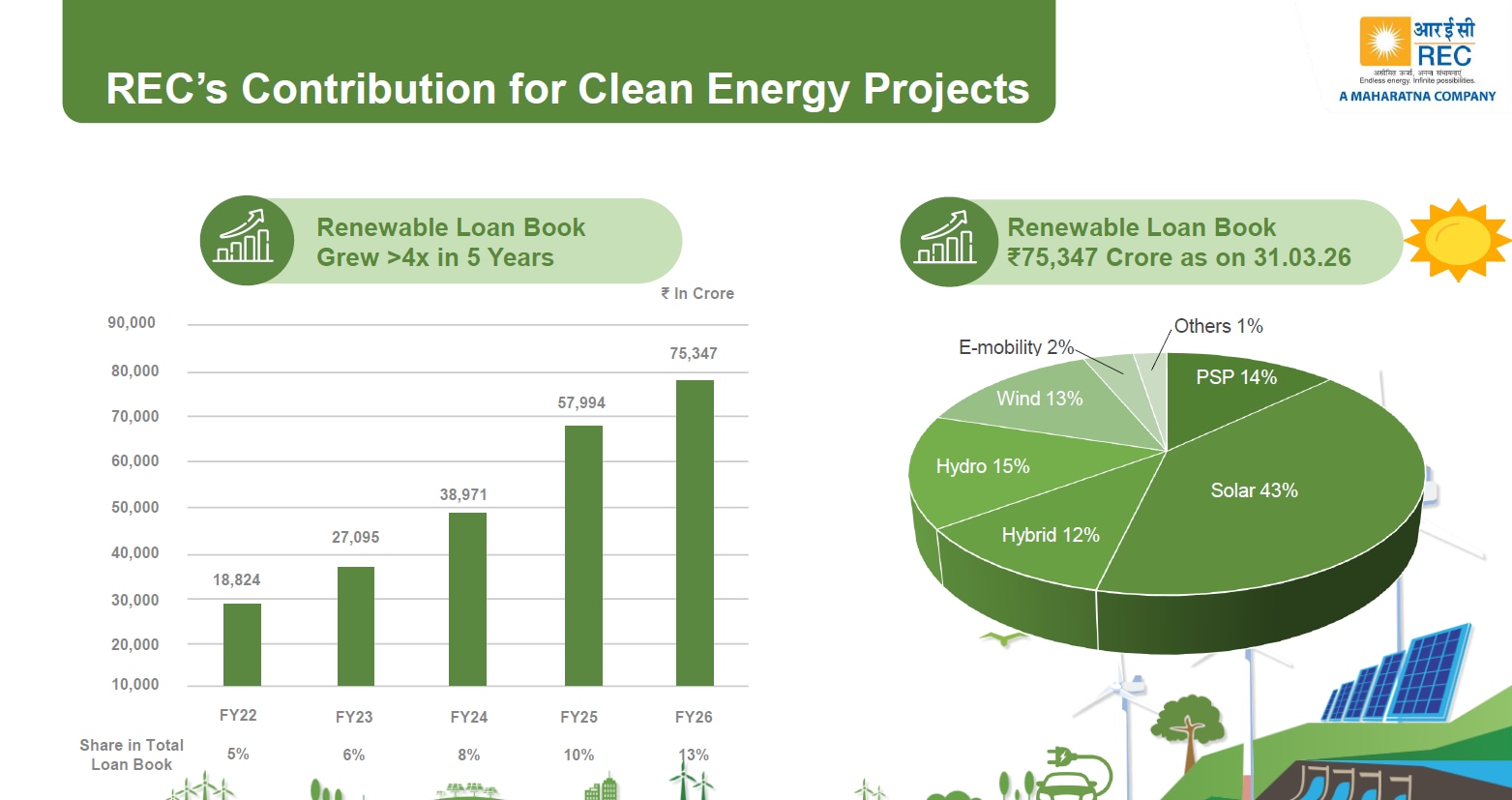

Traditionally, REC is the financier to the power sector value chain. It is currently a dominant player in India’s renewable energy transition, funding solar, wind, pumped storage, and green hydrogen projects. It aims to expand its clean energy portfolio to 30% of its total loan book by 2030.

However, the big boost for REC’s growth trajectory occurred recently.

Asset Diversification: Venturing Into Non-Power Logistics Infrastructure

Leveraging its Maharatna status, REC has broadened its mandate to finance the Non-Power Infrastructure and Logistics sectors. It is now funding Roads and Expressways, Metro Rail and Airports, Ports and Waterways, IT infrastructure, fiber optics, and E-Mobility.

Operational Mechanics: Inside the Quasi-Sovereign Capital Engine

Unlike typical commercial lenders, REC operates with a quasi-sovereign mandate. REC serves as the trusted implementation arm for the Government of India’s most ambitious national development schemes.

It is the lead Nodal Agency for the ₹3.0 lakh crore Revamped Distribution Sector Scheme. The project aims to drive smart-metering and infrastructure upgrades to reduce losses in state DISCOMs.

It is also the National Implementing Agency for the PM Surya Ghar Muft Bijli Yojana. This is a national mission to install rooftop solar systems on one crore households.

Deconstructing REC’s Standalone Net Profit Expansion Profile

The company’s market cap is ₹91,057 crore, as of 15 May 2026.

REC Share Price

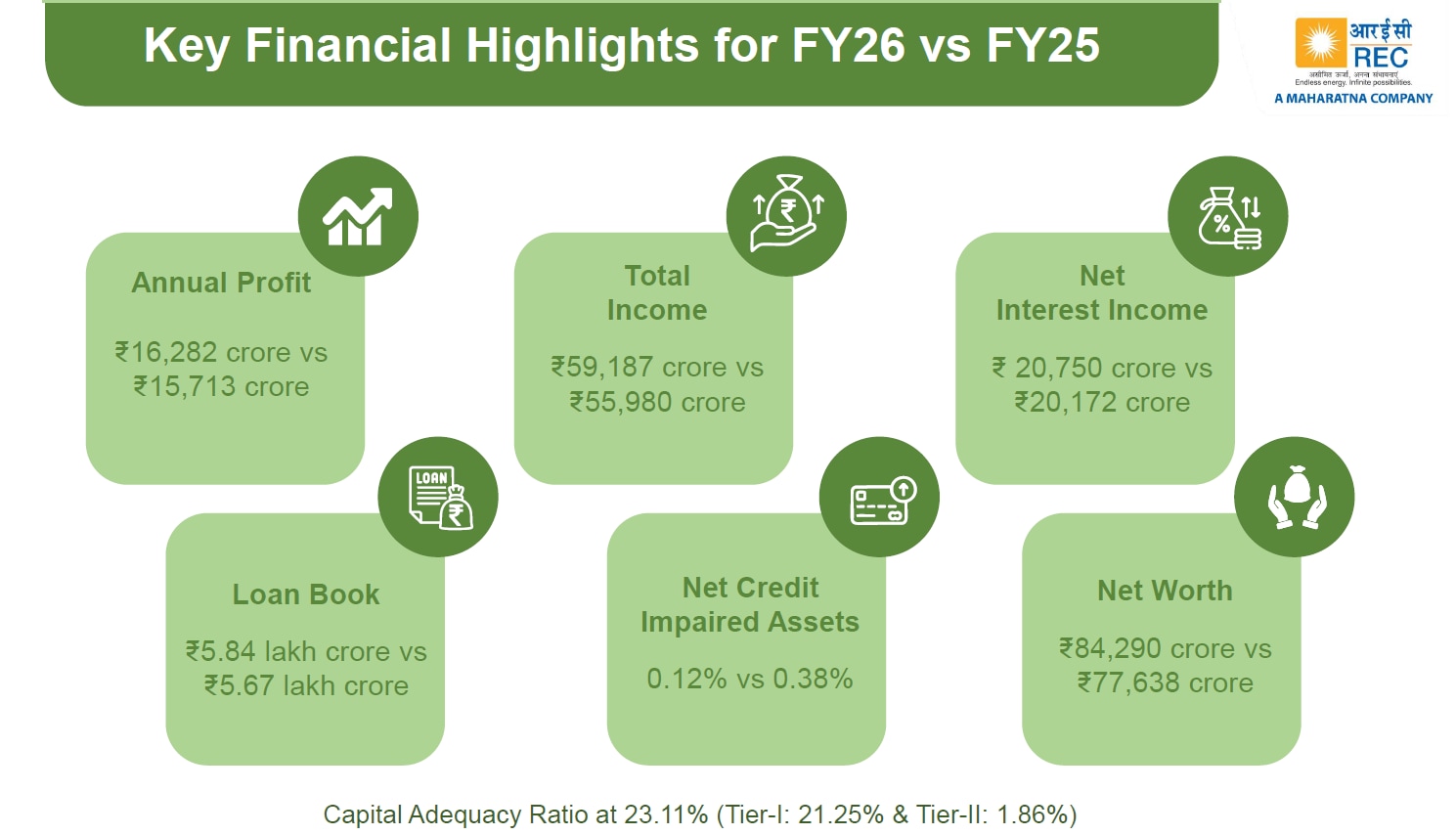

Over the last 5 years, REC’s standalone net profit grew at a 14% CAGR, reaching ₹16,282 crore in FY26.

Disbursement Dynamics: Deconstructing the FY26 Growth Spurt

REC’s capital deployment reached record highs in FY26. It disbursed ₹2.1 lakh crore, up 10.4% YoY, with the distribution and conventional segment accounting for the majority (43%) of the total loan book exposure.

Precisely, the book is diversified, with the Distribution segment contributing 31%, followed by RBPF (31%), Renewable (14%), Conventional Generation (12%), and others (12%).

In fact, loan disbursements (excluding the Revamped Distribution Sector Scheme) surged by 28%.

This was driven by distribution funding, which grew to ₹67,258 crore from ₹24,489 crore. On the loan assets side, the loan book expanded to around ₹5.8 lakh crore, from ₹5.7 lakh crore in FY25. The share of renewable energy in loan assets was 13%, while distribution contributed 38%.

How Cost of Funds and Yield Compression Pressured NIM

Yield on loan assets stood at almost 10%. However, the cost of funds grew slightly by 23 bps to 7.3%. With a healthy disbursement, net interest income surged by 2.9% to ₹20,750 crore. While total income grew by 5.7% to ₹59,187 crore.

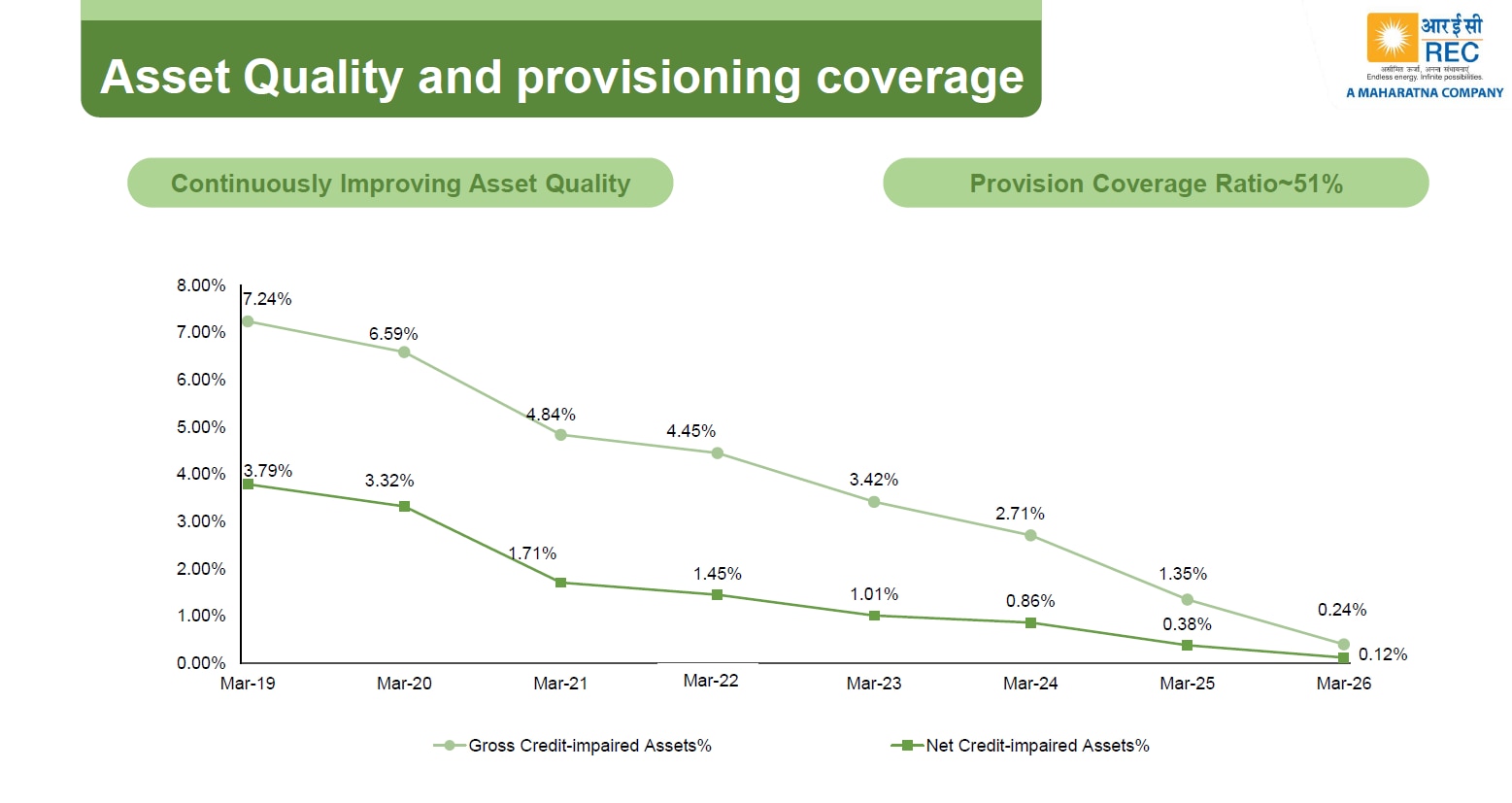

Asset Quality Peak: Net NPAs Plunge to an 8-Year Record Low

However, net interest margin fell 20 bps to 3.4%, due to a decline in interest spread. On the asset-quality side, net credit-impaired assets fell to an 8-year low to 0.12%. As a result, net profit rose modestly by 3.6% to ₹16,282 crore in FY26.

Capital Efficiency at Scale

The company generates a robust return on equity (ROE), underscoring its efficient capital allocation. Return on Net Worth stood at 21.5% in FY25 and remained strong at 20.1% in FY26.

Book value per share expanded to ₹320 per share, up from ₹295 in FY25. Current return on assets (ROA) stands at 2.7%, a very healthy level. For context, ICICI Bank has an ROA of 2.1%.

Unpacking the 99.3% Cash Collection Architecture

For an NBFC, the truest measure of cash generation isn’t traditional free cash flow. But rather its ability to collect the money it lends.

This is reflected in REC’s high cash recovery metrics. In FY25, REC achieved a cash recovery rate of 99.3%. In absolute terms, REC generated cash inflows (recovery) of ₹1,79,695 crore in principal and interest against dues from its standard assets.

Even from its bad loans, REC managed to recover ₹4,462 crore in cash during the year. This continuous, high cash inflow provides the liquidity required to sustain its cash dividend payments. We have used FY25 numbers where FY26 numbers are unavailable.

You cannot pay a growing dividend without a growing bottom line. REC’s payouts are backed by the highest profits in its history.

Assessing the Long-Term Sustainability of the 5.4% Dividend

In FY25, REC reported its highest-ever net profit of ₹15,713 crore, which further increased to ₹16,282 crore in FY26. A promise to pay dividends is only as good as the track record backing it up.

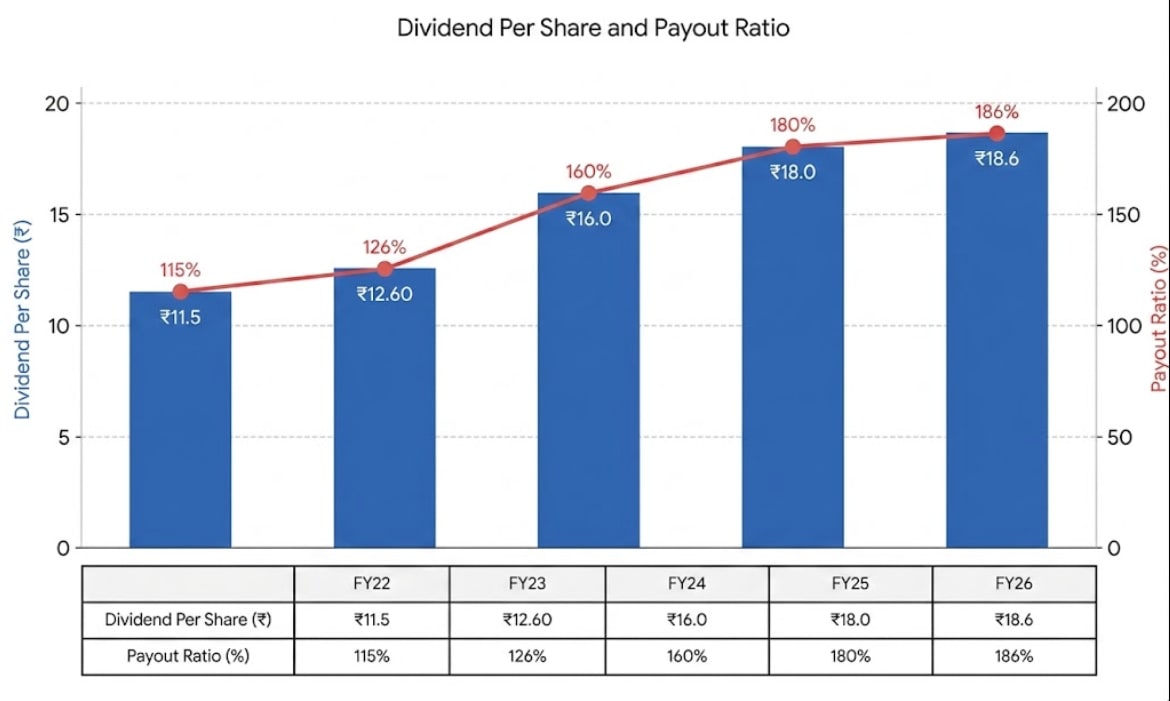

For REC, the historical data reveal a stable trajectory of consistently increasing annual per-share dividends. Over the last 5 financial years, it has not only maintained its payouts but has consistently increased its dividend per share year-on-year.

In FY22, the company distributed a dividend of ₹11.5 per share (115% of the face value), which rose to ₹12.6 (126%) in FY23, further increased to ₹16 (160%) in FY24, reached ₹18 (180%) in FY25, and finally reached ₹18.6 (186%) in FY26.

At the current share price of ₹346, FY26 payout translates into a dividend yield of 5.4%.

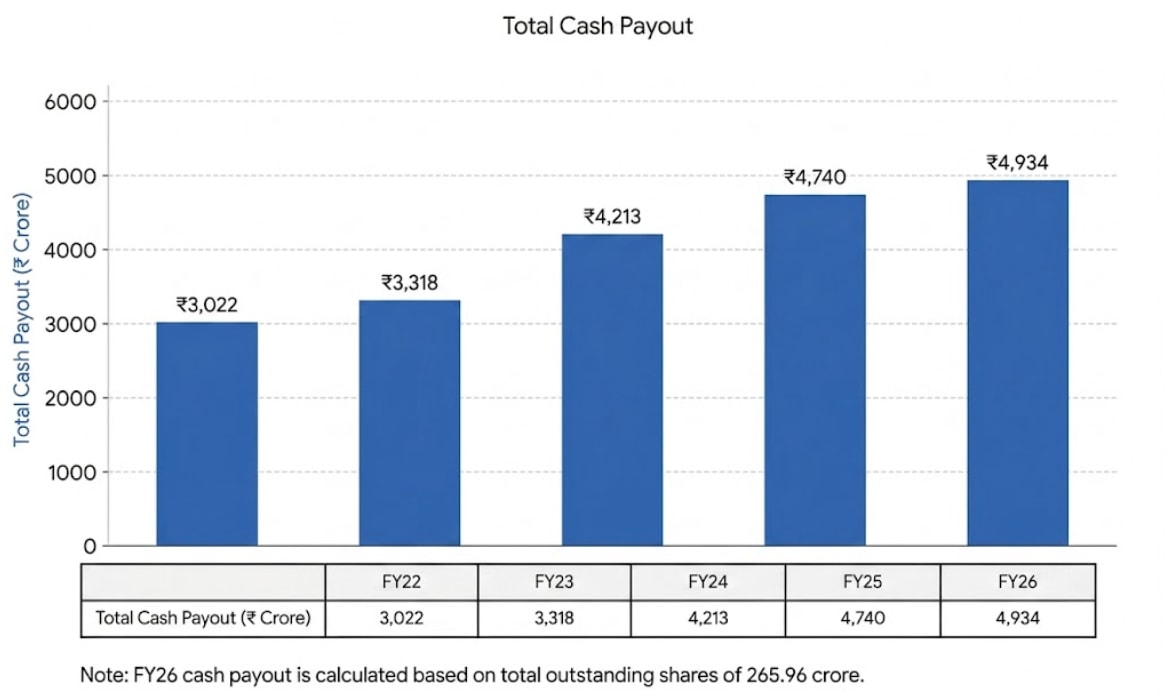

Similarly, the total cash dividend payout is expanding along with the bottom line. This data reveals that from ₹2,510 crore in FY21, the cash REC returned to investors has nearly doubled to ₹4,934 crore in FY26.

This also implies that a decline in net profit could reduce dividend payouts. Nevertheless, due to government mandate, a strong balance sheet, and liquidity, payouts could be sustained and even increased with profit growth.

Demystifying the 30% Sovereign Payout Mandate

As per the Government of India guidelines, REC is mandated to pay a minimum annual dividend of 30% of its net profit.

For instance, if you divide the FY25 dividend payout of ₹4,740 crore by the net profit (₹15,713 crore), you get roughly 30%. The same applies to FY26, during which it distributed 30% of its net profit (₹16,282 crore) as dividends (₹4,934 crore).

This reflects that REC is precisely following the payout threshold. Thus, as the profit continues to increase, the total cash available for distribution naturally scales up accordingly. This also enables REC to finance its loan book using the remaining 70% of its net profit.

Regulatory Buffers: Why High CRAR and LCR Insulate Dividend Payouts

To ensure that aggressive lending and dividend payouts do not trigger a cash crunch, the RBI mandates strict liquidity buffers.

In FY26, REC’s Liquidity Coverage Ratio (LCR) stood at 150%. This exceeds the regulatory requirement of 100%. This means REC holds High-Quality Liquid Assets, such as Government Securities and AAA-rated corporate bonds.

These fixed assets can be instantly converted to cash to meet 30-day stress obligations. With a high LCR, REC’s cash flow for dividends remains securely insulated from short-term market shocks.

How Capital Adequacy Buffers Prevent Dividend Shock

Before a financial institution can declare dividends, it must meet strict capital adequacy requirements. If capital drops too low, dividends get cut.

REC’s Capital to Risk-weighted Assets Ratio (CRAR) stood at 23.1% in FY26. This is well above the regulatory requirement of 15%.

This capital buffer provides ample headroom to absorb macro shocks, fund future loan book growth, and sustain dividend payouts without straining the balance sheet.

Valuation Arbitrage: Is REC Limited Trading at a Steep PSU Discount?

Valuation-wise, REC trades at a price-to-book (P/B) multiple of 1.1x, in line with the 5-year historical median of 1.1x. The valuation is not just at a discount to the industry P/B (2.1x) but also to other PSU financiers such as IRFC (2.3x), HUDCO (1.9x), and IREDA (2.8x).

The “Dividend Hunter” Verdict: Is This a Long-Term Income Fortress?

REC meets the key Dividend Hunter filters. It has shown profit growth, strong cash flows, and a payout ratio within thresholds.

Given a yield of 5.4%, consistent increases in cash flow, a government mandate of a 30% payout, and a historical dividend payout track record, it appears likely that the dividend payout trend could continue and increase.

The Integration Risk: Navigating the April 2027 PFC Merger Mandate

However, this assumption is contingent on new policies (if any) once the proposed merger of REC and PFC takes effect from April 2027. Nonetheless, dividend hunters should add this stock to their watchlist and see if it sustains its dividend yield.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data were unavailable have we used an alternative, widely accepted, and widely used source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.