In this edition of Dividend Hunter, we turn our attention to an Indian subsidiary of a UK-based parent company and one of India’s leading lubricant manufacturers. It consistently generates stable operating cash flows and follows a structured Dividend Distribution Policy.

Traditionally, this week’s Dividend Hunter stock manufactures engine oils, transmission fluids, and industrial lubricants for various vehicles and machinery. Today, its expansion is supported by growing rural consumption and an increasing vehicle footprint across the country.

The management is also preparing for technological shifts. They are developing specific fluids for electric vehicles and testing advanced cooling solutions for data centers. These emerging segments provide clear structural support for future business volumes.

The company blends its products locally across three facilities in India. It is also broadening its product portfolio to include everyday auto care accessories and application-led industrial solutions.

The company in focus today is Castrol India Limited.

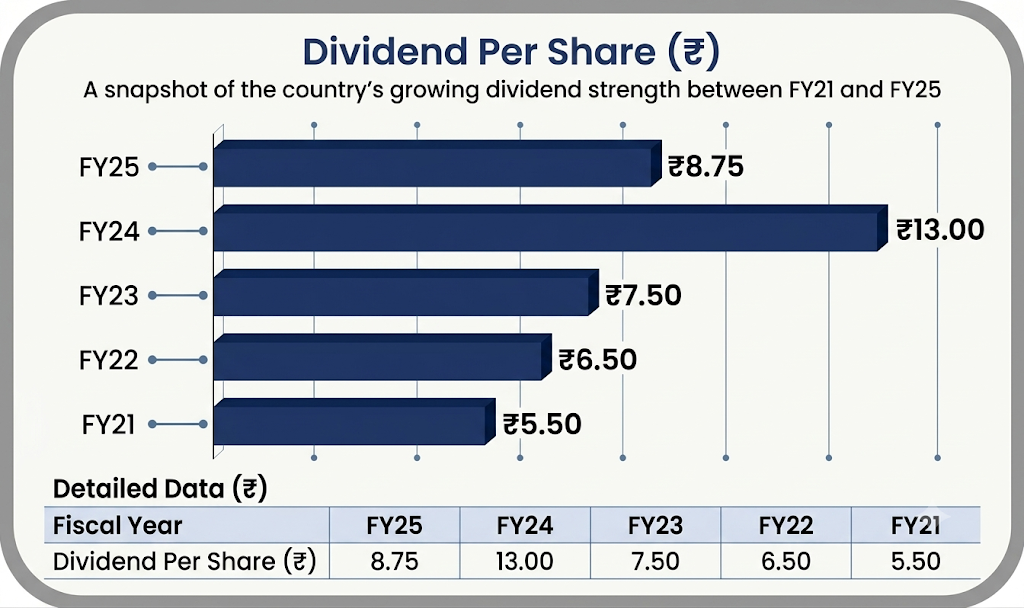

Castrol paid a total dividend of ₹13.0 per share last year in FY24, its highest annual payout on record since FY21, followed by another ₹8.75 per share as a dividend in FY25. The company’s 12-month period ends in December 2025. Looking closely, Castrol India has maintained a consistent track record of returning capital over the last several years.

For income-focused investors, this indicates a reliable, well-planned dividend strategy. However, the core question remains: can Castrol India continue to fuel these dividend payments over the long run?

Deconstructing Castrol India’s Automotive and Industrial Revenue Mix

Castrol, part of the global BP Group, manufactures automotive and industrial lubricants with a presence in India spanning more than 115 years. Its product offerings are diversified, spanning 12 industries through 45 brands and roughly 600 brand variants.

Mobility Solutions (Automotive) is the core revenue driver, accounting for 87-90% of Castrol’s business. While it is the mature core of the company, it still delivers healthy high-single-digit growth. Within this, the company supplies engine oils, transmission fluids, brake fluids, and coolants for various vehicle types.

The second segment, Industrial Lubricants and Fluids, serves heavy industries such as steel, cement, automotive, textiles, and energy. This segment accounts for 10-13% of the business today. This segment is growing faster than the automotive side, delivering double-digit volume growth.

To future-proof its operations and tap into emerging structural tailwinds, Castrol is building additional business around the core lubricants business. This also helps in retaining customers.

To this end, the company has launched a comprehensive auto-care range featuring mechanical care (brake and throttle-body cleaners), aesthetic care (shampoos, waxes, glass cleaners), and rider care (helmet cleaners and chain lubes).

In light of the evolving mobility landscape, Castrol is introducing advanced EV fluids, including the Castrol ON EV Transmission Fluid and specialized EV greases, to support e-motors and batteries. The company is actively collaborating with EV manufacturers, such as Ather Energy and Tata Motors, to integrate into their product development.

Further, Castrol is pioneering immersion-cooling fluids for advanced thermal management in data centers.

The scale of its operations can be gauged from the fact that approximately 8 liters of Castrol products are sold in India every second. Castrol boasts a significant national footprint, with its products available across approximately 150,000 retail outlets.

Rural Execution: Deep-Value Penetration as a Defensive Growth Anchor

A major growth driver for the business today is its deep push into India’s rural markets. The company has expanded its rural distribution to 43,000 outlets across 9,000 villages, supported by a network of 700 “Rural Service Express” centers.

This rural strategy is highly profitable and is largely driven by the rising demand for personal mobility, particularly two-wheelers and pre-owned cars in these regions.

Why Robust Volume Growth Pushed FY25 Revenues to ₹5,721.5 crore

Over the last 5 years, Castrol’s net profit grew at a robust 10% CAGR, reaching ₹950 crore in the 12 months ended December 2025 (FY25). Revenue in FY25 rose by 7% year-on-year to ₹5,721.5 crore, driven by an 8% increase in overall sales volume.

Profitability also showed a steady upward trend. The company’s operating EBITDA grew by 5% to ₹1,347.5 Crore for the full year, with margins at 23.6%. In FY25, Net profit also rose slightly to ₹949.9 crore, up 2.5%.

The company’s market cap is ₹18,279 crore, as of 19th June 2026.

Castrol India Share Price

Unlocking 67% ROCE: Assessing Capital Allocation Efficiencies

This consistent profit growth, paired with a debt-free balance sheet, ensures that the company maintains strong return ratios. The company’s return on equity (ROE) was nearly 50% in FY25, indicating that the business efficiently converts its retained earnings and shareholders’ equity into profit.

The company also demonstrates efficient capital utilization, with a Return on Capital Employed (ROCE) of approximately 67%. This highlights that Castrol consistently generates value relative to the capital it deploys. This gives it the financial strength to sustain its dividend payouts.

Deconstructing the Strong Cash Conversion Behind Castrol’s ₹1,090 Crore Operating Inflow

Castrol’s stated dividend policy is to pay sustainable dividends that are funded primarily by its internal cash accruals. Thus, we must examine the relationship between the conversion of profits into actual cash and the liquid reserves on its balance sheet.

It reported net cash from operations of ₹1,090.1 crore in FY25. According to management, disciplined cost management and working capital management drove healthy operating cash flow. This robust trend reflects high-quality earnings and provides the financial flexibility to sustain consistent shareholder returns.

At the same time, Castrol operates a highly efficient business model that does not require big capital reinvestment to maintain its operations. In FY25, the company spent ₹94 crore net on the purchase of property, plant, and equipment. This aligns perfectly with management’s commentary that their typical annual capex is around ₹100 crore.

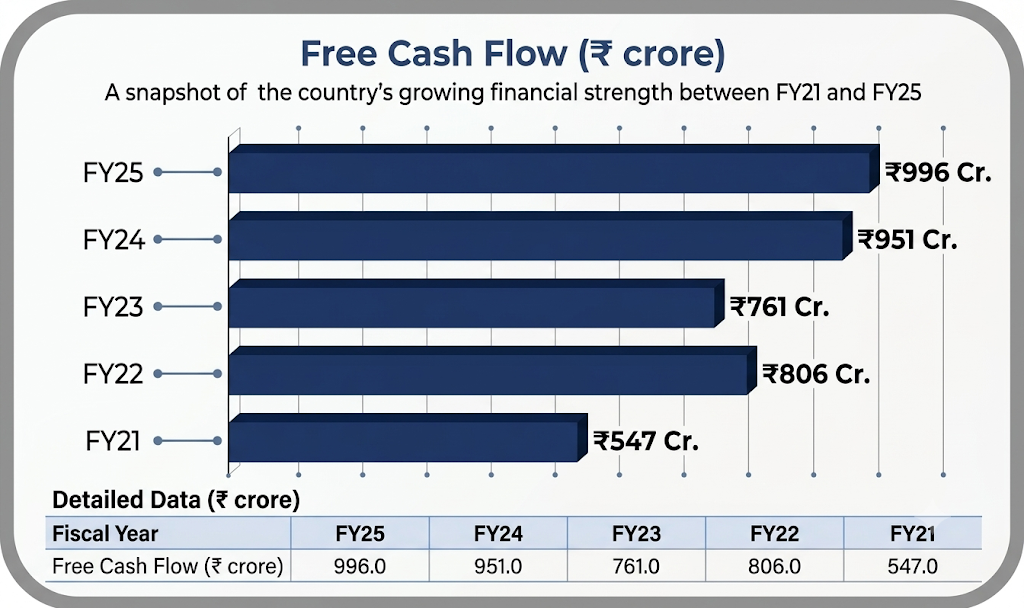

This means that Castrol generated its highest-ever free cash flow of ₹996 crore. This cash generation is not a one-off event, as the company has historically consistently generated over ₹472 crore in free cash since FY14.

Sustaining a 90% Payout: Can Free Cash Flow Cover the Capital Outflow?

Consequently, this strong buffer of free cash flow is the structural reason Castrol can sustain an industry-leading dividend payout ratio of around 90%. Additionally, since regular operations generate approximately ₹1,000 crore in free cash, the management emphasized that “Capex is not a constraint for us.”

The company easily self-funds all its strategic initiatives. This strong free cash flow generation is important because the company’s dividend policy explicitly states that it aims to pay sustainable dividends funded entirely through internal cash accruals.

Furthermore, this free cash flow fuels its cash and cash equivalents and its reserves. As of 31 December 2025, Castrol India holds over ₹1,140 Crore in highly liquid bank balances. Additionally, it held reserves of ₹1,405.7 crore to cover any shortfall in dividend payments.

For instance, in FY25, when cash dividends paid (₹1,285.9 crore) exceeded net operating cash flow generated during the year (₹1,090.1 crore), the company used its reserves to bridge the gap. Therefore, a ‘cash-cow’ business like Castrol, which holds substantial cash on its balance sheet, is likely to continue paying dividends to its shareholders.

Why a Growing ₹1,405.7 Cr Reserve Balance Makes Payouts Predictable

Regarding its dividend per share, the company paid ₹8.75 per share in FY25. At the current share price of ₹185, this translates into a dividend yield of 4.7%. The historical payout pattern is very interesting and has consistently grown over the years.

Castrol paid a dividend of ₹8.5 per share (ex-special dividend of ₹4.5) in FY24, up from ₹7.5 per share in FY23. The FY23 payout was also higher than the ₹6.5 per share distributed in FY22 and ₹5.5 per share in FY21.

Further, Castrol India’s regular dividend payout ratio has steadily climbed from around 71.8% in FY21 to 91% in FY25. This suggests that the company is returning a larger share of its earnings to shareholders. Looking ahead, Castrol aims to protect its highly profitable automotive business while aggressively expanding into industrial segments and future-ready adjacencies.

Automotive lubricants will remain the backbone in the medium term. Rural India will play a pivotal role in this. Management views it as a bright spot, with demand there remaining robust, particularly for two-wheelers and tractors.

The company has already expanded its rural distribution to 43,000 outlets and plans to continue expanding to drive trial volume growth.

Management anticipates continued rapid growth in the industrial segment, meaning it will account for a significantly larger share of the company’s total volume mix by 2030. This growth is heavily supported by India’s broader infrastructure buildout and manufacturing push across sectors such as steel, cement, textiles, and heavy engineering.

Its new, additional revenue sources are also growing rapidly. ‘Auto Care’ is now available at 60,000 outlets. The ‘Castrol Auto Service’ network has expanded to 750 workshops. This helps build long-term trust and retain customers. To establish a foothold in this emerging sector, the company is launching transmission, grease, and cooling fluids for EVs.

Evaluating the Valuation Premium: How Castrol Weighs Against Gulf Oil and Veedol

Valuation-wise, Castrol trades at a price-to-equity (P/E) multiple of 18.76x, a discount to its 10-year historical median (20.2x) but at a premium to the sector median (13.7x). Relatively, it trades at a premium to its closest peer, Gulf Oil (13.8x) and Veedol Corporation (13.7x).

The “Dividend Hunter” Verdict: Is This a Long-Term Income Fortress?

The key takeaway is that Castrol is well-positioned to sustain its dividend payouts. Its stable profitability, strong cash balance and reserves, high free cash flow generation every year, and dividend distribution policy could support future dividend payout.

As long as those strengths remain intact, the payout appears well protected. Dividend hunters should add this stock to their watchlist.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation and conference call. Only in cases where the data were unavailable have we used an alternative, widely accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.