Let’s start with Meta’s latest quarterly results. On the surface, they were spectacular.

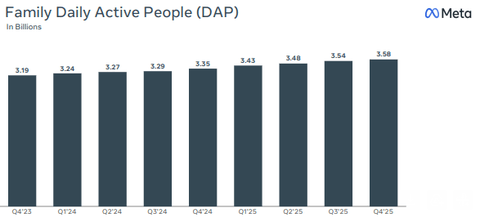

Daily active users across Facebook, Instagram, WhatsApp, and Threads hit 3.58 billion people. That’s 43% of everyone on planet Earth using Meta’s apps every single day. Revenue per user jumped 16% to $16.56. Ad impressions accelerated even as prices went up, which is basically the holy grail of advertising businesses.

The stock initially shot up over 10% after the earnings announcement. Investors loved what they saw.

Then something strange happened. By the end of the day, all those gains had evaporated. Meta’s stock was right back where it started. Over the past year, it’s actually down about 7%.

What killed the excitement? Two words that make investors sweat: capital expenditure.

The $135 billion question

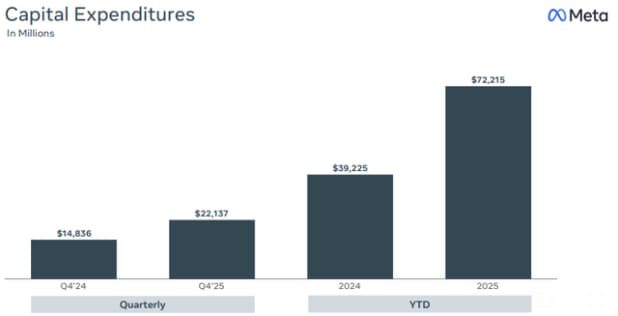

Meta announced it plans to spend between $115 billion and $135 billion in 2026 on building AI infrastructure and conducting AI research. To give you context, that’s roughly double of what it spent in 2025, which itself was nearly double what it spent the year before.

This isn’t normal tech company spending. This is Meta spending at the same level as Amazon Web Services or Google Cloud, except there’s a crucial difference. Those companies build cloud infrastructure and rent it out to other businesses. Meta is building all this capacity purely for internal use.

The skeptics ask a fair question: what exactly are you building, Mark?

During the earnings call, CEO Mark Zuckerberg was surprisingly candid about how little he could actually share. He told investors upfront that his answers would be “somewhat unfulfilling” because they’re only six months into rebuilding their AI effort. He promised to share more about models, products, and businesses “over the coming months.”

That’s not exactly reassuring after committing over $100 billion to the project.

Enter Bill Ackman

While most investors were getting cold feet, Bill Ackman was doing the opposite.

In November 2025, Ackman’s Pershing Square fund quietly started buying Meta shares at around $625 each. By the end of December, the position had grown to represent 10% of the fund’s capital, roughly $2 billion.

For context, Ackman typically holds only about a dozen stocks at any given time. He’s famous for making concentrated, high-conviction bets and holding them for years. So a $2 billion bet on Meta is a serious statement.

His investor presentation laid out the thesis clearly: “We believe Meta’s current share price underappreciates the company’s long-term upside potential from AI and represents a deeply discounted valuation for one of the world’s greatest businesses.”

The bet has worked so far. Meta shares gained 11% from when Ackman started buying through the end of 2025, plus another 3% in early 2026.

What Ackman Sees

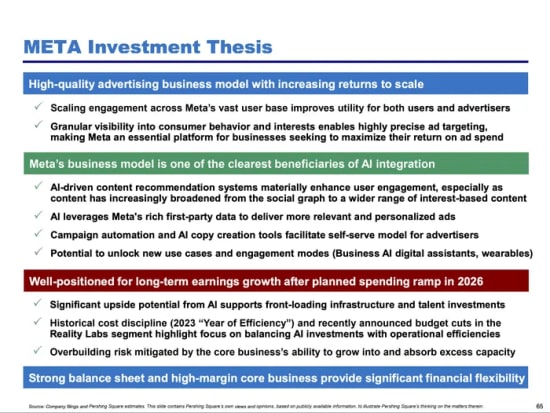

Pershing Square’s case for Meta rests on a simple idea: AI isn’t just an expense, it’s the future revenue engine.

The fund argues that Meta’s 3.58 billion daily users make it “one of the clearest beneficiaries of AI integration.” Here’s their thinking:

First, AI improves the core advertising business. Better content recommendations keep people scrolling longer. Smarter ad targeting means advertisers get better results and will pay more for each ad. We’re already seeing this play out in Meta’s numbers, with ad impressions accelerating even as prices rise.

Second, AI could unlock entirely new revenue streams. Think AI-powered digital assistants for businesses, smart glasses that actually work, or new ways to engage with content that we haven’t even imagined yet.

Third, the valuation looks attractive. At 22 times forward earnings, Meta is trading at levels we haven’t seen since 2023. Remember what happened after 2023? The stock went on a massive run.

Ackman is basically saying: yes, the spending is scary, but you’re getting one of the best businesses in the world at a discount because everyone is too focused on the near-term costs.

What the skeptics see

Not everyone is convinced. In fact, many analysts who like Meta’s core business are deeply worried about where this is all heading.

The biggest concern is free cash flow. For years, Meta was a cash-generating machine. Now? The company is spending its entire operating cash flow on capital expenditures. Free cash flow is essentially heading to zero as spend.

Then there’s Reality Labs, Meta’s division that builds VR headsets and smart glasses. It loses roughly $19 billion every year. That’s $19 billion in losses, annually, with no clear path to profitability. The Ray-Ban Meta glasses have seen strong sales growth, but they’re sold at a loss and heavily subsidized.

Add it all up, and Meta is pouring tens of billions into two separate bets (AI research and Reality Labs) with uncertain payoffs, while the one thing that actually makes money (the advertising business) has to fund everything.

Some analysts also point out an uncomfortable timing issue. After Meta announced its spending plans, both Amazon and Google revealed even higher capital expenditure budgets than expected. This matters because Meta is trying to build a frontier-level AI model to compete with ChatGPT, Google’s Gemini, and Anthropic’s Claude.

The problem? Amazon and Google have their own custom chips (Trainium and TPUs) that cost less than the Nvidia GPUs that Meta has to buy. They can spend more efficiently than Meta can. And in AI, where compute power still matters enormously, that’s a real disadvantage.

Multiple analysts now expect Meta won’t just hit the high end of its spending guidance, they think Meta might actually raise it further when Q1 results come out.

The irony nobody talks about

Here’s what makes this situation fascinating: Meta’s core advertising business is phenomenal. Not good. Not great. Phenomenal.

Consider what’s happening right now. Meta is showing people more ads than ever before. Normally, when you flood the market with more supply, prices drop. Economics 101.

But Meta’s ad prices are going up. They’re showing more ads AND charging more for each one. That only happens when your targeting is so good that advertisers see better returns even at higher prices.

The company just guided for 26% to 34% revenue growth in Q1. For a business of Meta’s scale (over $150 billion in annual revenue), that kind of acceleration is almost unheard of.

So here’s the irony: Ackman is betting $2 billion that a nearly perfect advertising business will successfully transform into something beyond advertising. He’s not buying Meta for what it is, he’s buying it for what it might become.

So who’s right?

This comes down to a question of faith, really.

Do you believe Mark Zuckerberg when he says Meta needs to spend $135 billion to stay competitive in AI, even though he can’t yet articulate exactly how it will make money?

Do you trust that Reality Labs will eventually find a sustainable business model after burning through nearly $100 billion cumulatively with nothing profitable to show for it?

Do you think Meta can catch up to OpenAI, Google, and Anthropic in the AI race when those competitors have structural advantages and head starts?

Ackman is clearly betting yes on all counts. He’s taking a multi-year view that Meta’s management will figure out how to monetize these massive investments, and when they do, today’s valuation will look cheap.

The skeptics aren’t saying Meta’s core business is bad. They’re saying that even the world’s best business can become a mediocre investment if management burns enough cash on projects that never pay off.

At 22 times earnings, Meta isn’t expensive for what it is today. But is it cheap enough to justify the risk of what Zuckerberg is trying to build tomorrow?

That’s the $2 billion question Bill Ackman just answered with his wallet. Wall Street is still making up its mind.

Sonia Boolchandani is a seasoned financial writer She has written for prominent firms like Vested Finance, and Finology, where she has crafted content that simplifies complex financial concepts for diverse audiences.

Disclosure: The writer and her his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.