Beyond the Bluechips: The Microcap Resilience in FY26

The Nifty 50 might be gasping for breath under the weight of premium valuations, but something different is happening in the oft ignored small-cap space. While the market favourites struggle to maintain single-digit growth, a few micro-cap players are quietly making strong moves.

And amidst all this, two manufacturing microcap penny stocks have achieved a rare financial feat. They have almost surpassed their entire FY25 net profit in just the first nine months of the current fiscal year (FY26). Mind you, these aren’t speculative ones driven by social media hype or “operator” pumps. Instead, they represent a fundamental shift where operational leverage is finally meeting market demand at scale.

What separates these two outliers from the typical “penny” trap is a combination of strong financial discipline, near zero debt and an enviable Return on Capital Employed (ROCE). As they head toward a stronger end FY26, these companies are slowly catching the eyes of smart investors.

Let us take a look at these stocks.

Kamdhenu Ltd: The TMT Brand Pivot to Zero Debt

Incorporated in 1994, Kamdhenu Ltd is into manufacture, marketing, and distribution of TMT Bars, structural steel and allied products.

With a market cap of Rs 627 cr, the company is the largest TMT selling brand in India, in the Retail Segment with 8,500+ Dealers, 250+ Distributors across India with 80+ Franchise Units to manufacture Steel Rebars, Structural Steel Products & Colour Coated Profile Sheets.

The company boasts of what we could call the trifecta of debt, dividend and dominance. Being the largest manufacturer of TMT bars, the company dominates the sector with ease. Add to that the company’s current virtually zero debt status (debt-to-equity ratio of 0) and a dividend yield of 1.12% while the industry median is a flat 0%.

Kamdhenu also boasts of a current ROCE of an enviable 29%, as that is more than double of the current industry median of 14%, which in simple words means for every Rs 100 the company uses as capital, it makes a profit of Rs 29 on it, while its peers average around just Rs 14.

The Operational Paradox: Stagnant Sales, Record Profits

The financials of the company say a lot about the company’s strong hold on capital efficiency. Let us take a look…

The company’s sales have seen a drop from Rs 924 cr in FY20 to Rs 747 cr in FY25, and for the 3 quarters of FY26 ending in December 2025, the company has logged sales of Rs 556 cr only.

However, despite the fall in sales, Kamdhenu has managed to grow its operating profit and the operating profit margins (13% at the end of December 2025)

The EBITDA (earnings before interest, taxes, depreciation, and amortization) grew from Rs 45 cr in FY20 to Rs 75 cr in FY25, recording a 11% CAGR. And for the 3 quarters of FY26 the company has logged an EBITDA of Rs 67 cr already.

Net profits are what has grabbed the attention of smart investors as it has grown from Rs 2 cr in FY20 to Rs 61 cr in FY25, logging compound growth of 97%. Between April and December 2025, profits of Rs 61 cr have been recorded already.

So, the company has hit the FY25 profit number in just 3 months of FY26, implying that it will have a strong end to FY26.

As you can see, the company’s sales have dropped, but thanks to the solid capital efficiency, the company has managed to log impressive EBITDA and Net Profits, while maintaining zero debt and a good dividend yield.

Market Correction: A 67% Discount from Peak?

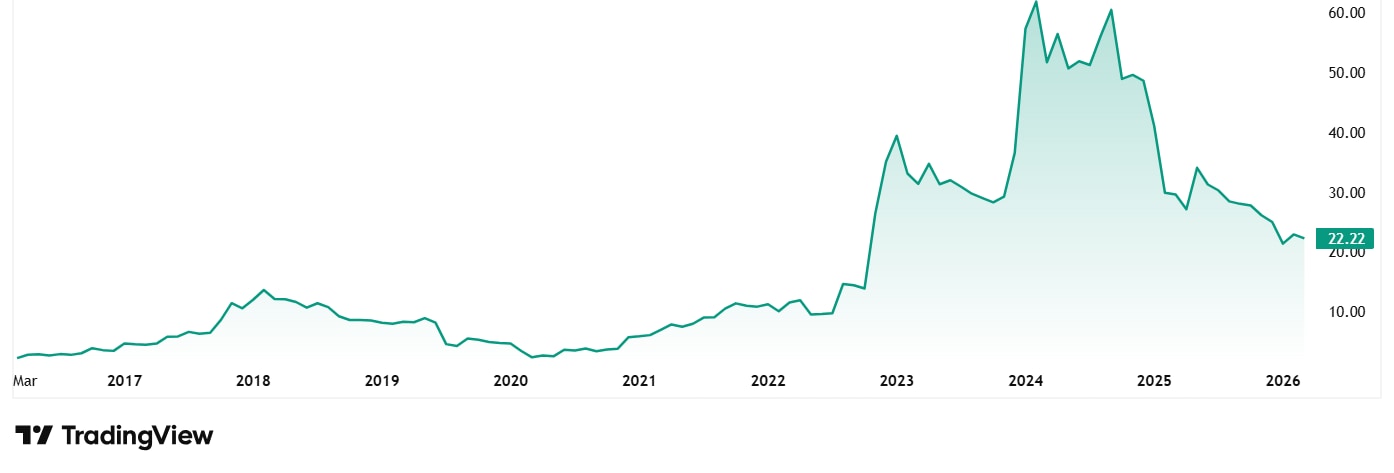

The share prices for Kamdhenu Ltd were around Rs 7 in March 2021 and as of closing on 6th March 2026, it was Rs 22.

While this might be over a 200% jump in 5 years, the stock has corrected sharply by 27% in just the last 6 months and is now trading close to its 52-week low of Rs 20. This decline reflects a sobering market recalibration, rooted in decaying top-line performance. A 3.5% contraction in operational revenue suggests that profit growth is being driven by fiscal discipline rather than market share expansion.

At the current price of Rs 22, the stock is trading at a discount of over 67% from all its all-time high price of Rs 67.

As for valuations, the company’s share is trading at a PE of 8x, and the current industry median is 18x. The 10-year median PE for Kamdhenu is however 12x and the industry median for the same period is 19x.

From Commodity Player to Brand Powerhouse: The Kamdhenu Shift

Kamdhenu seems to be shifting from a traditional manufacturer to a high-margin brand leader. Its asset-light franchise model explains the high ROCE and the Zero debt status, a rare feat in the steel industry. While the market has cooled on the stock due to flat sales, the massive jump in net profit proves its operational strength.

At the current valuation, the stock is trading significantly lower than the industry average. However, if the company can reignite revenue growth to match its profit margins, it could become a lean, efficient alternative to the sector’s heavyweights.

Premier Polyfilm: High-Efficiency Manufacturing in Vinyl & PVC

Incorporated in 1992, Premier Polyfilm Ltd manufactures vinyl flooring, PVC Sheeting and Artificial leather cloth which are used for a variety of industrial and consumer applications.

With a market cap of Rs 608 cr, the company is a manufacturer of Specialty Calendared Films and Sheets which are used for various industrial and consumer applications. It is also capable of Coating, Calendaring, Printing, Lamination, Embossing, Complete inhouse testing with own fabric manufacturing.

Just like Kamdhenu above, Premier Polyfilm also has a zero-debt status currently, along with a current ROCE of 30%, while peers average around 17%.

Earning Power: Nearing FY25 Totals in Three Quarters

Looking at the financials, the sales of the company have grown at a compounded rate of 12% from Rs 147 cr in FY20 to Rs 263 cr in FY25. And for the first 3 quarters of FY26, the sales logged by the company is Rs 218 cr,

As for the EBITDA, the company saw a compounded growth of 22% from Rs 14 cr in FY20 to Rs 38 cr in FY25. And between April and December 2025, EBITDA of Rs 35 cr was recorded helping the company almost match its entire previous year’s EBITDA in just three quarters.

The net profits of the company grew at a compound rate of 34% between Rs 6 cr in FY20 and Rs 26 cr in FY25. And for the 3 quarters of FY26, profits of Rs 23 cr have been logged already by the company indicating a strong bottom line.

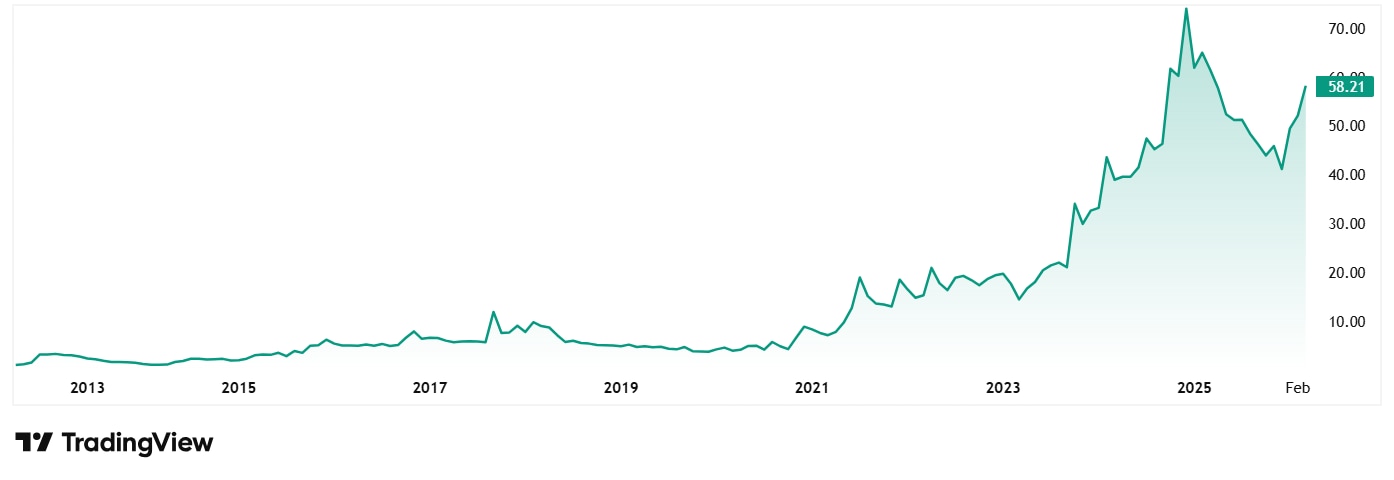

The share price of Premier Polyfilm Ltd in March 2021 was around Rs 8 and as of closing on 6th March 2026 it was Rs 58, which is a jump of 625%.

However, at the current price of Rs 58, the stock is trading at a discount of over 32% from its all-time high of Rs 86.

The company’s share is trading at a PE of 21x which is same as the current industry median. The 10-Year median PE of the company is 18x while the industry median for the same period is 23x.

Premier Polyfilm: Efficiency vs. Valuation Balance

Premier Polyfilm’s debt free status combined with its high ROCE proves that management can generate high returns while maintaining a lean balance sheet. Even though the stock price has dipped 32% from its peak, the company’s earning power remains strong.

With nine-month profits already nearing last year’s full-year total, the business seems to be gaining momentum. At the current valuation, the stock looks like priced fairly compared to its peers. But will it be able to sustain these positives and get back to its highs is something only time will tell.

From Defensive Efficiency to Growth Engines

The traditional playbook for small-cap investing usually demands a tolerance for high leverage and erratic cash flows. However, Kamdhenu Ltd and Premier Polyfilm are rewriting this narrative by swapping breakneck expansion for cold, hard operational efficiency. By keeping their balance sheets debt-free and getting record profits out of flat or modest revenues, these micro-caps have hit their full-year FY25 profit targets with an entire quarter to spare.

However, a fundamental question remains for the final stretch of FY26. Can these companies transition from being defensive masters of cost-control to aggressive engines of top-line growth? If they can pair their current capital efficiency with a genuine recovery in sales volume, the recent share price corrections might eventually look less like a retreat and more like a coiled spring.

For now, they stand as a potent reminder that in the world of micro-caps, a clean ledger is often the best precursor to a record year. So, it will be fascinating to watch the trajectory of these stocks. Add them to a watchlist and keep an eye on them to ensure you do not miss out on any action.

Disclaimer:

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.