Biopharma SHAKTI is the government’s latest push to strengthen India’s position in biologics and biosimilars. It was proposed in the Union Budget 2026–27. The scheme has an outlay of Rs 10,000 crore over five years. The intent is clear. India does not want to stay limited to low-cost generics. It wants to build strength in high-value biopharma.

The scheme aims to support domestic development and manufacturing. It also looks to reduce import dependence. It wants to improve India’s position in global biologics supply chains.

The plan goes beyond funding companies. It looks at the full ecosystem needed for biologics to grow. This includes expanding National Institutes of Pharmaceutical Education and Research (NIPERs). These are government-run institutes. They train specialised talent for the pharma and biopharma industry.

Their focus areas include drug development, biotechnology, and regulatory science. The scheme also aims to build stronger clinical research capacity. It looks to improve regulatory systems. The goal is faster and more credible approvals. In simple terms, the focus is on talent, trials, and approvals, not just production.

This is where things get interesting. Biologics scale-up does not come from one breakthrough. It happens when research, manufacturing, clinical trials, and approvals move together. That alignment is what this scheme is trying to create. It also creates a better setup for companies working as Contract Development and Manufacturing Organisations (CDMOs).

These companies help global pharma firms develop and manufacture drugs. If execution holds, it can open up a stronger growth phase. This is especially true for companies working in advanced biologics, biosimilars, and complex therapies.

The stock selection reflects this shift. The focus is not on broad pharma names. It is also not on familiar CDMO stories. The idea is to stay close to the biologics value chain. One set of companies brings strong development and manufacturing capability. Another shows that biologics can be commercialised at scale. The third adds stability through proven execution and global outsourcing linkages. Together, they capture where the space is moving.

#1 Syngene International: Navigating the CDMO Transition

Syngene (established in 1993) as a Biocon subsidiary is India’s first Contract Research Organization (CRO) which expanded later to be an integrated service provider offering end-to-end drug discovery, development, and manufacturing services on a single platform (CRAMS).

Syngene International reported a lackluster third quarter. The impact came mainly from a single large molecule biologics product. This affected its CDMO business. Q3 revenue from operations declined to Rs 917 crore from Rs 944 crore reported a year ago. Profit after tax fell to Rs 15 crore compared to Rs 131 crore reported a year ago.

The company said the pressure was linked to one commercial-stage product of its largest biologics customer. This has been a recurring issue through the year. It also led to a cut in full-year guidance. However, management said the rest of the business is stable.

Overcoming the ‘Single Product’ Headwind

Excluding this one product, growth remains in high single digits to low double digits. Research services continue to add new clients. This includes chemistry, biology and clinical research. Capacity utilisation has also improved across small and large molecule manufacturing.

This matters in the context of the Biopharma SHAKTI theme. Biologics scale-up depends on depth, not one product. It needs stronger pipelines and better utilisation. Syngene appears to be moving in that direction. It has extended its partnership with Bristol Myers Squibb till 2035. The company supports this client with over 700 scientists in Bengaluru. It also expanded advanced chemistry labs in Hyderabad. A new commercial-scale facility for liquid-filled capsules has been commissioned.

Betting on the 10-Year BMS Horizon

The biologics build-out is still ongoing. The Bayview Biologics facility in the US has completed validation. Hiring is now in progress. The facility is expected to start operations soon. In Mangalore, utilisation is improving in both small and large molecules. A sterile fill-finish line has also been added. This allows the company to move from drug substance to drug product. The focus now is on building pipeline and filling capacity across locations.

The near-term outlook remains cautious. The impact from the single product is expected to continue into the next few quarters. This will weigh on reported growth. At the same time, the underlying business is holding steady. The next phase depends on scaling utilisation and diversifying revenue. In a biologics-led CDMO story, Syngene is not a clean growth play today. It is a company working through a transition.

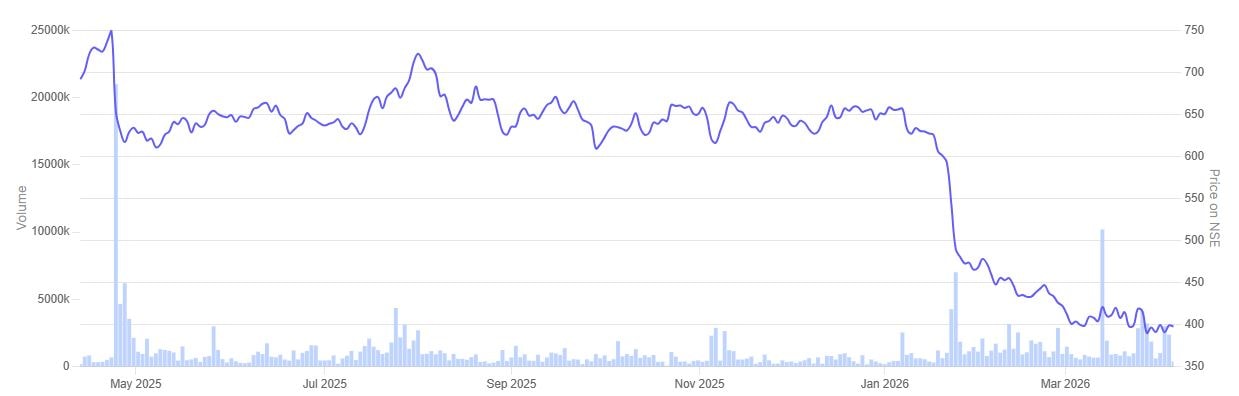

In the past year, the share price of Syngene International tumbled 41.9%.

Syngene International 1 Year Share Price Chart

#2 Biocon: Scaling Global Biosimilars

Biocon is engaged in the business of manufacture of biotechnology products and research services.

Biocon’s Q3FY26 performance showed its relevance in a biologics-led growth cycle. The group reported operating revenue of Rs 4,173 crore. This was up 9% YoY. Reported net loss stood at Rs 52 crore which is significantly lower than the net profit of Rs 81 crore reported over a year ago.

Generics and Biosimilars Powering the Mix

The quarter was driven by biosimilars and generics. Biosimilars revenue rose 9% to Rs 2,497 crore. Generics revenue grew 24% to Rs 851 crore. This helped offset weakness in the Contract Research, Development and Manufacturing Organisation (CRDMO) business. CRDMO revenue fell 3% YoY. The mix shift is important. It shows how biologics scale is playing out through products, filings and market access.

Biocon has been aligning itself with India’s push in biologics and biosimilars. It has invested in R&D talent and global manufacturing over the years. The planned merger of Biocon Biologics with Biocon is a key step. It aims to create a single integrated platform. This platform will combine biosimilars and specialty generics at scale.

The global pipeline also moved forward in Q3. Three oncology biosimilars were disclosed. These include subcutaneous trastuzumab, nivolumab and pembrolizumab. These are large molecules nearing loss of exclusivity. Biosimilar pertuzumab has been submitted to the US FDA. In metabolic therapies, generic liraglutide was launched in the Netherlands. An out-licensing deal was signed with Ajanta Pharma for semaglutide. The deal covers 26 countries across Africa, the Middle East and Central Asia.

Regulatory progress also supported the quarter. Patent settlements were finalized with Regeneron, Bayer and Amgen. This clears the way for aflibercept and denosumab launches. In the US, the ustekinumab biosimilar crossed 70% market access coverage. In Europe, approvals came for Yesafili prefilled syringe and the Yesintek auto-injector. In Turkey, Yesafili reached nearly 20% market share after launch.

Strategic QIP and the Oncology Pipeline Wave

Capacity and execution remain key. Manufacturing and quality systems were upgraded during the quarter. This supports higher demand and future launches. Major capex is now largely behind the company. Insulin drug product capacity is expected to double in the coming fiscal year. The Malaysia expansion is likely to turn commercial in FY27. Annual capex has already moderated to below $225 million. Earlier levels were above $275 million.

The overall picture is steady. Biocon is moving beyond early-stage capacity building. It is scaling products across global markets. The focus is on improving margins and cash flows. The next phase depends on execution. The direction remains tied to biologics growth and global expansion.

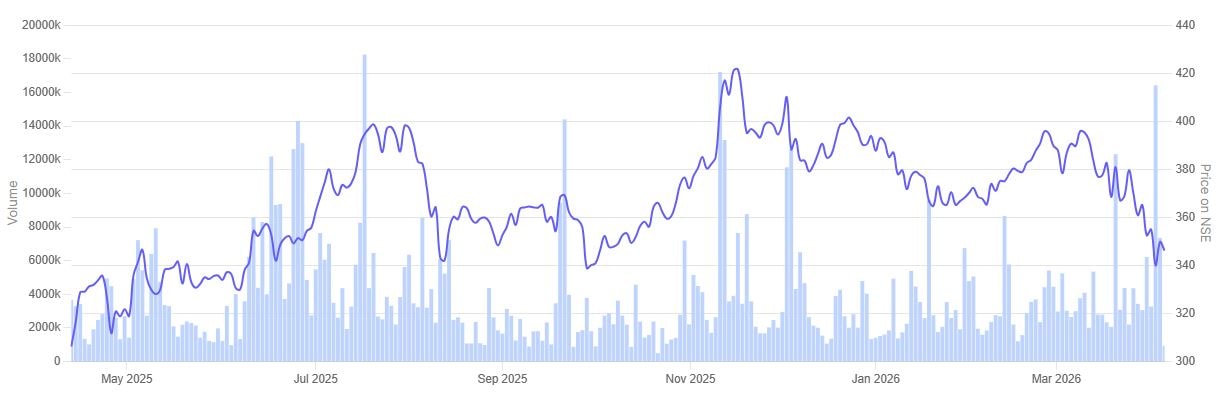

In the past year, the share price of Biocon is up 13%.

Biocon 1 Year Share Price Chart

#3 Divi’s Laboratories: Powering Global Custom Synthesis

Incorporated in 1990, Divi’s Laboratories manufactures and exports active pharmaceutical ingredients (APIs), intermediates and nutraceutical ingredients.

Divi’s Laboratories reported a mixed third quarter. Consolidated total income stood at Rs 2,692 crore, up 12.3% YoY. Profit after tax stood at Rs 583 crore. This was slightly lower than Rs 589 crore in the same quarter last year.

The quarter was supported by custom synthesis. The product mix stood at 57% custom synthesis and 43% generics. That matters in the current CDMO frame. Divi’s is not a pure biologics company. But it remains relevant because global innovators are increasingly looking for large-scale, compliant and reliable manufacturing partners.

The company was active in several request for proposals (RFPs) and customer visits during the quarter. Multiple projects are moving through development and validation. A few are expected to move closer to commercial volumes over the next one year.

The Pivot to Peptides and GLP-1 Capacity

Peptides remain an important growth area. Divi’s has been working in peptide chemistry for years. During the quarter, it supported multiple customer programs across clinical phases. Work continued in complex building blocks and fragments. Protected amino acids are also becoming more important again.

Supply has already moved from smaller validation quantities to larger commercial volumes in some cases. This keeps Divi’s tied to the broader biologics and peptide manufacturing opportunity, even if the model is different from a biosimilars player.

Capacity creation is moving ahead. A pilot plant for GLP-1-related work has already been built. One commercial building with several large-scale solid-phase peptide synthesis reactors has also been completed. Validations are under way.

Commercial volumes from the three dedicated custom synthesis projects are expected around the third or fourth quarter of calendar year 2027, subject to regulatory approvals and customer timelines.

The Backbone of Backward Integration

Unit 3 at Kakinada is also becoming more important. It is being used for starting materials and intermediates under the backward integration plan. This is helping free up capacity at older units for new GMP work. Expansion and transfer activities are still under way. A second phase at Kakinada, with four production blocks, is under evaluation. Capital work in progress stood at Rs 2,394 crore at the end of December 2025.

Regulatory execution remained steady. The company completed a US FDA general CGMP inspection at its Unit 1 Choutuppal facility during the quarter. The outcome was positive. Exports continued to account for around 89% of sales revenue. Europe and the US together contributed 73% of export sales. That underlines how dependent this business remains on regulated global markets and on execution consistency.

The broader picture is fairly clear. Divi’s is not the direct commercial face of India’s biologics push. Its role is different. It sits in the manufacturing backbone. It is building capabilities in peptides, custom synthesis and backward integration.

The next phase depends on how quickly validations turn into approvals and how these dedicated projects scale into commercial supply. For now, the company looks less like a near-term volume jump story and more like a steady platform being readied for the next wave of global CDMO demand.

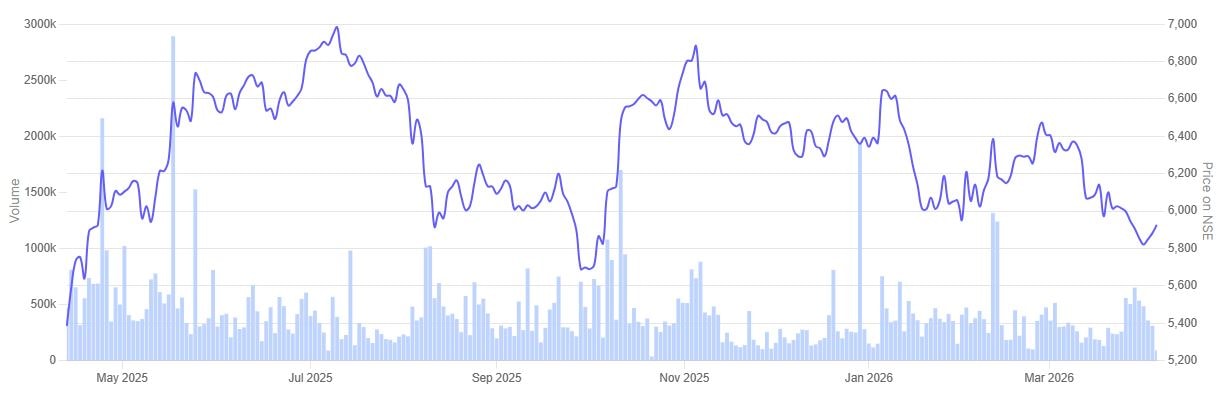

In the past year, the share price of Divi’s Laboratories is up 10.2%.

Divi’s Laboratories 1 Year Share Price Chart

Valuations

Let’s now turn to the valuations of the companies in focus, using the Enterprise Value to EBITDA multiple as a yardstick.

Valuations of Companies in focus

| Sr No | Company | EV/EBITDA Ratio | 5-Year Average EV/EBITDA | Industry Median | ROCE | ROE |

| 1 | Syngene International | 15.7 | 27.3 | 15.9 | 13.5% | 10.5% |

| 2 | Biocon | 17.8 | 16.6 | 6.2% | 4.8% | |

| 3 | Divi’s Laboratories | 40.3 | 41.2 | 20.4% | 15.4% |

Divi’s Laboratories stands out on return ratios. Return on Capital Employed (ROCE) is 20.4% and return on equity (ROE) is 15.4%. Syngene International is lower, with ROCE at 13.5% and ROE at 10.5%. Biocon is the weakest on this metric, with ROCE at 6.2% and ROE at 4.8%. The gap here is quite visible.

Valuations also show a difference. Syngene is trading at 15.7 times EV/EBITDA. This is close to the industry median of 15.9 and well below its five-year average of 27.3. Biocon is at 17.8 times, slightly above its five-year average of 16.6. Divi’s is at 40.3 times. This is slightly lower than its five-year average of 41.2, but still much higher than the other two.

Each company is playing a different role. Biocon is selling biologics in global markets. Syngene is working with clients on development and manufacturing. Divi’s is more focused on large-scale manufacturing and custom synthesis. All three are linked to the same space, but their positioning is not the same.

The numbers reflect this difference. Divi’s is already delivering strong returns, so it trades at a premium. Syngene looks fairly priced, but returns are still improving. Biocon has scale, but returns remain low. From here, execution will decide how these numbers move.

Conclusion

The shift towards biologics and more complex pharma work is clearly underway. But this is not a straight-line story. It will take time to reflect fully in numbers. Capacity is getting built. Pipelines are improving. But conversion into steady revenues and margins is still playing out.

Each company is coming from a different starting point. One is already strong on return ratios and execution. Another has built scale but is still working on improving returns. The third sits somewhere in between, with capabilities in place but consistency still evolving. That is why the gap in numbers is visible today.

From here, the focus is quite basic. How well new capacities are used. Whether margins improve as volumes scale up. And whether returns remain stable as businesses grow. These are not one-time factors. They will show up gradually over the next few years.

This space is still evolving. There will be phases of strong growth and phases of slowdown. What matters is how these companies manage that cycle. Tracking execution, rather than just announcements, will give a clearer picture of who benefits the most from this shift.

You can track how these are progressing by adding stocks to your watchlist.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ekta Sonecha Desai has a passion for writing and a deep interest in the equity markets. Combined with an analytical approach, she likes to deep dive into the world of companies, studying their performance, and uncovering insights that bring value to her readers.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.