India’s retail market is entering a phase of structural expansion, backed by rising consumption, digital adoption, and changing consumer behaviour. In fact, India’s consumption growth has been 10.6%, the highest among the top five economies, according to Boston Consulting Group (BCG).

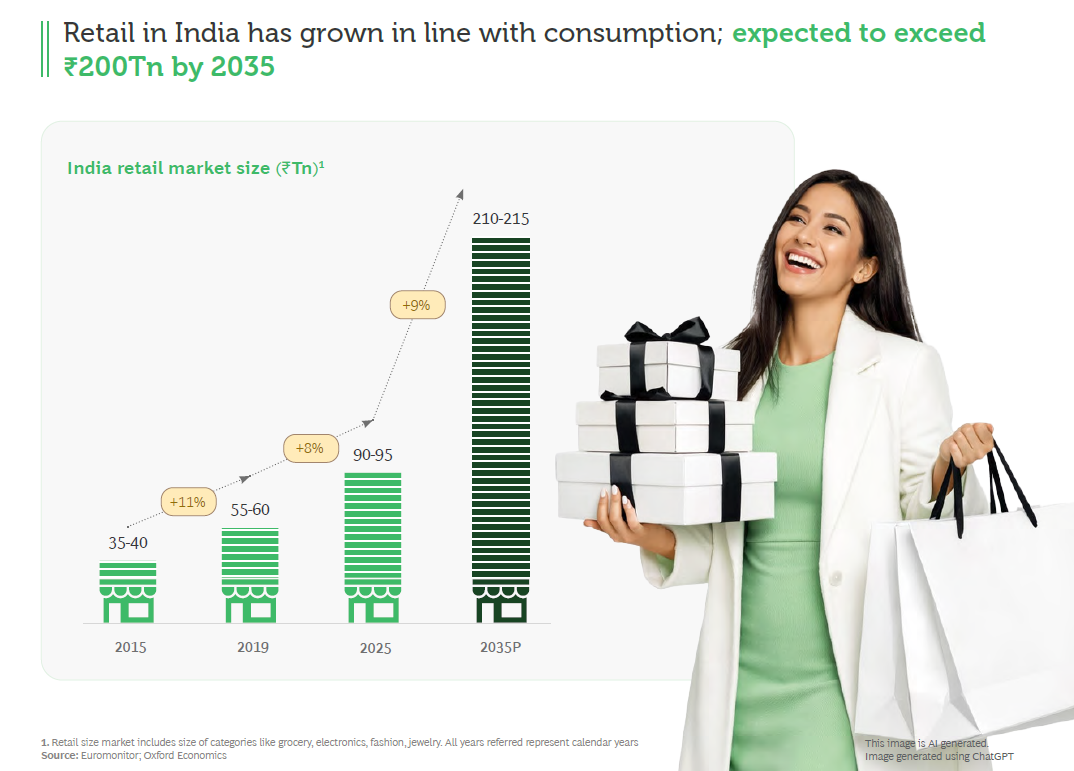

The joint report by BCG and the Retailers Association of India projects the market to more than double from ₹90-95 lakh crore in 2025 to ₹210-215 lakh crore by 2035, making India one of the world’s fastest-growing consumption stories.

The shift is not only about higher spending but also about how consumers shop, with AI-led discovery, omnichannel retail, and digital payments reshaping purchasing patterns. The report also highlights that India’s strong GDP growth and rising internet penetration are creating fertile ground for organised retailers to scale faster.

At the same time, demand from tier-II and tier-III cities, premiumisation trends, and greater preference for convenience are expanding the addressable market.

This is creating a long runway for companies operating across retail, fashion, grocery, electronics, and discretionary consumption.

Against this backdrop, this article examines three stocks that could benefit from the tailwind…

#1 Sai Silks (Kalamandir)

Sai Silks (SSKL) is one of the largest ethnic clothing retailers in South India, specialising primarily in sarees and value fashion. It offers ultra-premium and premium saris, lehengas, men’s ethnic wear, children’s ethnic wear, and affordable value fashion. Sarees are the main segment of its business, contributing 71.5% of its revenue (FY25).

Multi-Format Strategy: Mapping the ₹200 to ₹3.5 Lakh Product Spectrum

To cater to different market segments, SSKL operates through five different brand formats: Kalamandir (₹1,000-100,000), Mandir (₹6,000-350,000), Kanchipuram Varamahalakshmi Silks (₹4,000-250,000), KLM Fashion Mall (₹200-75,000), and Valli Silks (₹250-35,000).

The Regional Moat: Bridging Physical and Digital Footprints

The Kanchipuram brand is the largest contributor, accounting for 52% of the company’s revenue (FY26). SSKL operates 81 physical stores across 24 cities. With concentrated presence in South India, it serves customers across 25 states and 6 Union Territories. It sees 7,570 online visits per day with an average order value of ₹5,673.

FY26 Financials: Net Profit Surges 65% Amid Modest 3% SSSG

Coming to its financial performance, SSKL revenue rose by 13% year-on-year to ₹1,654 crore in FY26. Same Store Sales Growth (SSSG) grew by a modest 3% during the year. The SSSG for the year was primarily led by the Varamahalakshmi Silks and Valli Silks formats.

Average revenue per sq ft. stood at ₹21,070, and revenue per store (₹20.4 crore). EBITDA increased 23% to ₹261 crore, while margin expanded 128 bps to 15.8%. Consequently, net profit increased 65% to ₹141 crore.

Capital Expenditure Strategy: Regional Diversification and the Shift to Maharashtra

The company plans to add about 100,000 sq. ft. of net retail area in the coming year (currently 784,853 sq. ft.). Kalamandir format will drive this growth, mainly in Karnataka and Bangalore. Additionally, SSKL plans to diversify by entering at least one new state, such as Maharashtra.

Balance Sheet Safety: The 0-Debt Catalyst and 18% EBITDA Target

SSKL is debt-free. Thus, internal cash generation will fund this expansion without borrowing for the next 2-3 years. It expects an improved EBITDA margin of 17.5%-18%. Management expects future revenue growth to exceed the recent 13%.

SSSG is expected to be similar or slightly better, given the more wedding dates. Interestingly, management notes that higher gold prices could act as an indirect catalyst for the apparel segment. To attract footfall, the company plans to maintain an advertising budget of around 4% of revenue.

Risk Ledger: Aggressive Regional Over-Expansion and the Fast-Fashion Threat

On the risk side, SSKL faces heightened industry competition and a faster fashion cycle. Further, KLM Fashion Mall’s recent underperformance dragged down Telangana’s growth, where 60-65% of the brand stores are located. Also, over-expansion inherently risks future store consolidation.

Sai Silks Share Price

#2 Vishal Mega Mart

Vishal Mega Mart (VMM) is a diversified value retail chain catering to India’s mass market. By bridging the affordability gap, it mainly targets India’s largest consumer segments. The company operated a total of 795 stores across 535 cities by the end of FY26.

Scaling Up Store Infrastructure

The infrastructure spans a trading area of 13.45 million square feet. Its geographic footprint is diversified, with 305 stores in the North, the East (213), the South (197), and 80 in the West. It maintains deeper penetration into smaller towns, with 401 stores in Tier III cities, compared to 189 in Tier II and 205 in Tier I.

Notably, the company added 105 new stores in FY26 alone, with a significant focus on Southern states such as Kerala, Andhra Pradesh, and Karnataka. Furthermore, VMM is successfully scaling up its small-format stores, which now total 13 and demonstrate comparable per-square-foot productivity to their larger counterparts.

In FY26, Vishal Mega Mart’s revenue from operations grew 20% year-on-year to ₹12,906 crore. This was supported by a strong adjusted SSSG of 11%. On the profitability front, the company achieved an adjusted EBITDA of ₹1,321 crore, expanding its EBITDA margin to 10.2%. Net profit rose 33% to ₹839 crore.

Driving Growth through Private Labels & Premiumization

Private labels (own brands) remain central to the retailer’s strategy, contributing 74% of the revenue in FY26 (up 100 bps). This robust mix grants Vishal superior control over supply chains and pricing. This enables it to cushion consumers against inflation by offering products that are 30% to 50% cheaper than market-leading third-party brands.

It now has 26 brands in its portfolio, two of which have sales exceeding ₹1,000 crore, and six more crossing the ₹500 crore mark. Using a structured pricing ladder, VMM is encouraging customer upgrades. In Q4FY26, entry-level clothing grew 11.1%, and the highest-priced fashion segment outperformed it with a 14.7% SSSG. This reflects a shift towards premiumization.

The 16.9 Crore Loyal Customers Driving 95% of Revenue

VMM’s loyal customer base is its competitive moat. Its mobile-based loyalty program has reached around 16.9 crore registered users, making it the 12th largest loyalty program worldwide. This loyal group accounts for approximately 95% of the company’s total revenue.

Simultaneously, its Quick Commerce platform expanded its reach to 745 stores across 505 cities. It now has nearly 1.3 crore registered users. Management remains optimistic about the long-term consumption story. It plans to aggressively expand its stores.

Pricing Power: Shielding Consumers Against Inflation

VMM anticipates benefiting from a down-trading phenomenon due to inflationary pressures. In this, consumers shift to Vishal’s affordable private labels to stretch their household budgets. To support this, management plans to maintain its steep 40% price discount relative to national brands.

Financially, VMM expects to continue benefiting from operating leverage, as long-term lease costs are increasing at a slower pace (5% annually) than its targeted double-digit SSSG. Furthermore, management is actively researching new retail formats and ventures to expand into additional product categories and gain further market share.

VMM Share Price

#3 Baazar Style Retail

Baazar Style Retail is a prominent value fashion retailer known for operating the Style Baazar and Express Baazar brands. The company offers readymade garments, footwear, cosmetics, toys, and home furnishings. Like its peers, it strategically targets the aspirational consumer base primarily in underpenetrated Tier-2, Tier-3, and Tier-4 markets.

As of 31 March 2026, Baazar Style has significantly scaled its operations to 263 stores covering 2.5 million rentable square feet. Its retail presence now spans across 191 cities in 9 states.

Core markets like West Bengal, Odisha, Assam, and Bihar remain the backbone of the business, generating around 82% of its revenue (₹1,516 crore) in FY26. The balance 18% comes from the focus states, Uttar Pradesh, Jharkhand, Andhra Pradesh, Tripura, and Arunachal Pradesh.

The 37% Revenue Surge: Unpacking Baazar Style’s Operating Leverage

The company concluded FY26 with its highest-ever annual revenue, surging 37% year-on-year to ₹1,841 crore. This top-line expansion was supported by a healthy 3% SSSG and the continuous addition of new store locations. Within its product mix, apparel remains the dominant category, accounting for 86% of total sales, while general merchandise accounts for the remaining 14%.

Why Private Labels Are Becoming a Key Growth Driver for Baazar Style

A major pillar of its brand-building and margin-expansion strategy is its robust portfolio of 11 private labels. It also has a strong customer loyalty. Private labels accounted for 53% of overall revenue in FY26, up from 45% in FY25.

On the profitability front, it delivered strong results. EBITDA rose by 40% year-on-year to ₹264 crore, with the EBITDA margin expanding to 14.3%. Net exceptional gain of ₹32.5 crore boosted net profit by 220% to ₹47 crore. Excluding the exceptional gain, net profit remained flat at ₹14.4 crore, compared with ₹15 crore in FY25.

Targets 500 Stores as Expansion Pace Accelerates

Looking forward, Baazar Style is accelerating its growth roadmap with a vision to surpass 500 stores within the next three years. This aggressive expansion is fueled by Cupid Limited’s recent strategic investment of ₹331.5 crore. This will also aid in debt reduction and the introduction of new FMCG and personal care categories.

The company now targets 60 to 80 new stores annually, up from its previous goal of 40 to 50. To optimize supply chain efficiencies and local brand visibility, the retailer relies on a cluster-based expansion approach. Around 77% of its current footprint is concentrated in Tier-2, Tier-3, and Tier-4 markets, while the remaining 23% is in Metro and Tier-1 cities.

Bazaar Style Share Price

The Valuation Gap: Peer Comparison

VMM has stronger return ratios, including return on capital employed (ROCE) and return on equity (ROE), followed by Sai Silks. Bazaar-style return ratios are low due to volatile profitability.

Valuation-wise, Sai Silks trades at a discount to both the historical and industry median P/E. VMM is trading at a premium to the industry multiple, while Bazaar Style is at a premium to the industry median.

| Valuation Comparison (X) | |||||

| Price-to-Earnings (P/E) Multiple | Return Ratios | ||||

| Company | Company | Median | Industry | ROCE (%) | ROE (%) |

| Sai Silks | 11.3 | 28.5 (2.8Y) | 44.0 | 14.0 | 11.8 |

| Vishal Mega Mart | 68.7 | 99.2 (1.6Y) | 40.5 | 14.8 | 12.2 |

| Bazaar Style | 116.0 | 82.8 (1.6Y) | 51.1 | 7.4 | 5.2 |

| Source: Screener.in (Data as of 21st May 2026) | |||||

India’s retail market is projected to more than double from ₹90-95 lakh crore in 2025 to ₹210-215 lakh crore by 2035. Historical consumption growth of 10.6%, digital adoption, and rising demand from smaller cities are expected to drive market expansion.

Against this backdrop, these three retailers offer different ways to play the theme through store expansion, private labels, and value positioning. However, positioning will depend on execution, SSSG, margin expansion, and whether growth justifies current valuations.

Nonetheless, these three can be added to a watch list to track their execution.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data was unavailable have we used an alternative, widely used, and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.