Distribution grew, availability increased, and volumes followed. Growth was noticeable, direct, and easy to track. That phase has silently ended.

Spirits is no longer a market waiting to be breached. It is already embedded across income segments, geographies, and price points.

The question is no longer whether people are consuming. It is what they are choosing to drink today.

The Shift Isn’t in Demand, It’s in What Demand Has Become

That shift does not show up where the market usually checks. It does not begin with volumes. Now, it starts with how companies earn.

Across the alcoholic beverages sector, a pattern is slowly emerging. Revenue growth has stabilised in a constant range. Volume expansion has moderated, but the profits are starting to outpace revenue in a way that does not look natural.

That difference is the sign. Because it tells you that growth is no longer led by expansion.

It is being driven by product mix, pricing power, and the talent to extract more value from the same consumer.And once that change begins, companies that appear identical on the surface start behaving very differently.

We’ve picked two companies, United Spirits and Radico Khaitan, to understand the difference.

Same Trend, Different Stages: Why the Comparison Matters

United Spirits Limited and Radico Khaitan operate in the same market and gain from the same underlying shift toward premiumisation. But they are not in the same lifecycle phase.

One has completed the changeover. The other is still in the middle of building it.

That variance, between a finished shift and an ongoing one, is changing how their numbers behave. And, more importantly, it decides how long their growth can be maintained.

#1 United Spirits: When the Shift Is Done, Growth Becomes Less Visible, But More Powerful

The numbers do not immediately suggest a dramatic change.

Fourth-quarter consolidated revenue was ₹3,054 crore, up from ₹2,946 crore a year earlier, marking a 3.67% YoY growth.

On the surface, it may still seem like a large consumption business growing steadily through pricing and portfolio strength rather than through any sharp acceleration in demand.

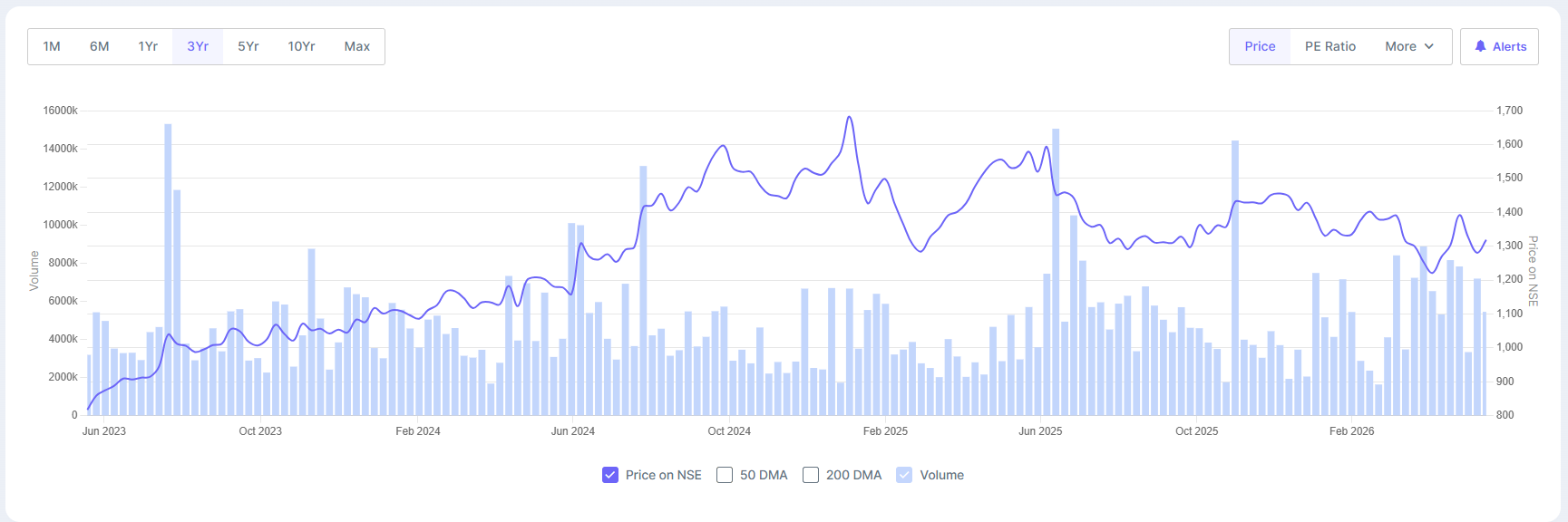

But the earnings profile is beginning to shift beneath the surface. The net profit, excluding exceptional items, was ₹596 crore, up 30% YoY from ₹458 crore in the year-ago quarter. The share price has grown at a compounded annual rate of 17% over the past three years, while the average return on equity (RoE) has been 21%.

United Spirits 3-Year Share Price Trend

That distinction matters. Because it suggests the business is no longer dependent purely on volume-led increase to improve profitability.

A larger share of earnings is now coming from product mix improvement and premiumisation within the portfolio itself.

The Portfolio Has Already Shifted

The lower end of the business, which once drove scale-led expansion, is no longer central to United Spirits’ growth.

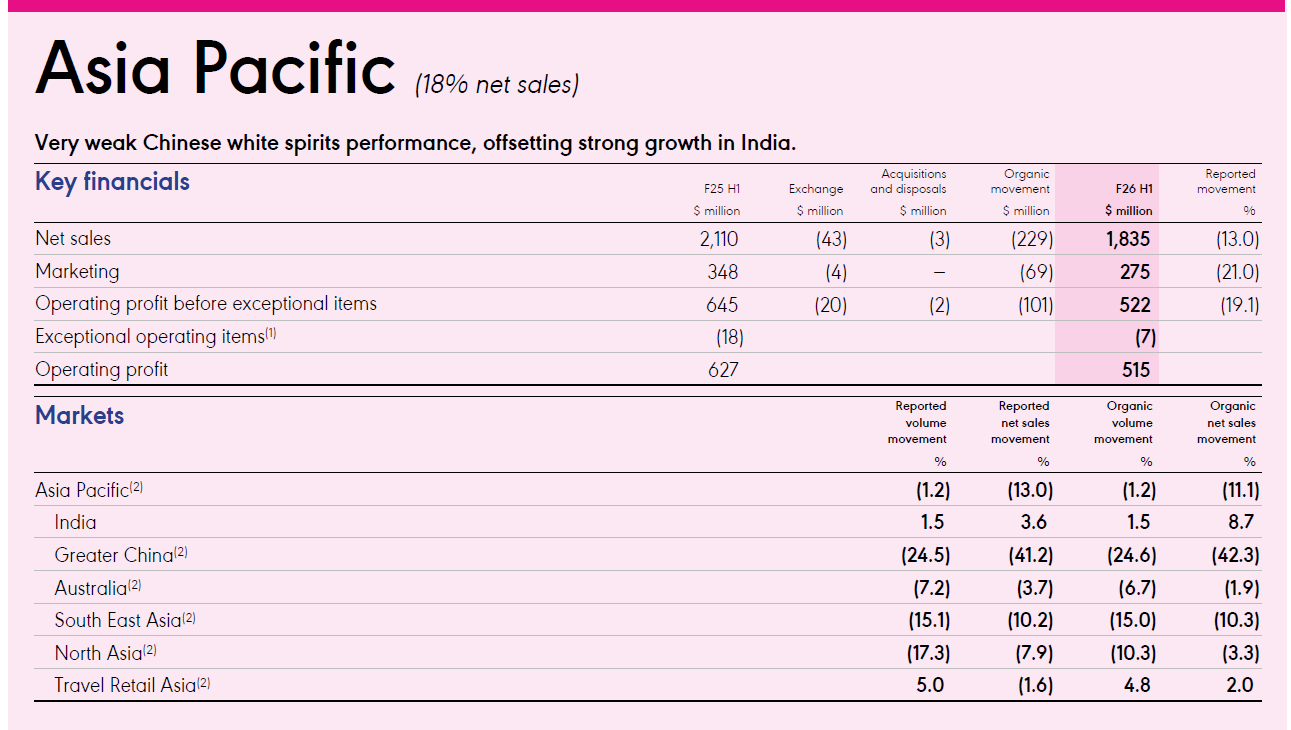

United Spirits’ parent, Diageo, in its FY26 interim commentary showed India’s organic net sales grew 8.7%, driven by broad-based growth in Prestige & Above brands, backed by the product, packaging, innovative flavours, and a reasonable price mix.

Royal Challenge, Black & White, Signature, and Smirnoff brought double-digit growth, while the Johnnie Walker portfolio maintained its high single-digit growth.

Such expansion becomes more crucial when compared globally.

Globally, Diageo’s organic net sales and profit declined 2.8% in the first half of FY26. A fall in the US spirits and Chinese white spirits sales affected overall performance.

India, however, remained one of the few large markets still showing high single-digit growth, supported largely by premium consumption rather than broad-based volume expansion.

This inference is crucial.

United Spirits is no longer in the phase where consumers are purely entering premium categories. Much of that change has already happened.

The business is now operating within a premium-heavy spirit range, where growth depends on consumers moving further upward within the same network.

The Growth Engine Has Changed

Earlier, expansion came from pushing consumers upward, from mass-market brands into premium offerings. That established noticeable thrust through higher volumes, wider distribution, and quicker topline growth.

Now, over time, growth is coming from expanding mix within the premium segment itself, through stronger realisations, better pricing power, and consumers moving toward higher-value labels within the portfolio.

This is a narrower growth lever. Which is why topline growth looks steadier rather than explosive. But it is also a more profitable lever over time.

Because once a portfolio becomes premium-heavy, even modest upgrades in pricing and mix begin to support earnings growth disproportionately versus revenue.

That is exactly what the latest quarter is beginning to reflect. Revenue grew over 7%, but profit growth outpaced it despite margins staying steady.

The earnings are beginning to move from scale-led increase to value extraction.

Margins No Longer Moved Cleanly

This is also why margins stopped behaving in a completely linear way.

Gross margins remained essentially strong, but operating margins did not expand sharply every quarter because the company was still reinvesting aggressively in premium brands.

Diageo’s interim results showed the global marketing investment declining 9.7% organically, even as spending continued to focus on higher-growth premium brands and premium-focused markets like India.

That created a business where premiumization continued to improve earnings and expand pricing power. However, the margin growth remained jagged as brand investment never fully slackened.

This isn’t an enterprise optimising solely for magnitude.

It is a business, adjusting for brand strength, pricing power, and long-term premium positioning.

And once a company reaches that stage, growth will look fundamentally different from a conventional volume-led liquor business.

The Constraint, though, has changed.

At this stage, United Spirits is no longer hampered by product reach.

Its brands are already deeply embedded across markets, distribution is deeply established, and the premium portfolio already rules the business mix.

The challenge is no longer about finding new consumers at scale. It is about getting more value from consumers already inside the portfolio.

That is a very different kind of growth problem.

Once premiumization reaches a certain level, the updates become smaller and harder to achieve. Moving a consumer from a mass whisky to a Prestige & Above label initiates a visible jump in realizations.

Moving that same consumer from one premium label to a slightly higher premium label creates a much narrower gain.

Which is why growth begins to change character.

Volumes stop growing meaningfully. Revenue growth settles into a stable range. But profitability continues to increase because the product mix keeps growing underneath.

That pattern is already visible in the numbers. Despite topline and operating margin growth in the fourth quarter, the profit growth was still stronger than revenue growth.

The implication is important.

United Spirits is no longer in the high-expansion phase of premiumisation. It is entering the monetisation phase, where growth comes less from adding consumers and more from increasing value per consumer over time.

Radico Khaitan: When the Shift Is Still Happening, Growth Still Looks Like Growth

If United Spirits reflects what happens after premiumisation matures, Radico Khaitan shows what the changeover looks like while it is still growing.

The difference is visible almost immediately in the numbers.

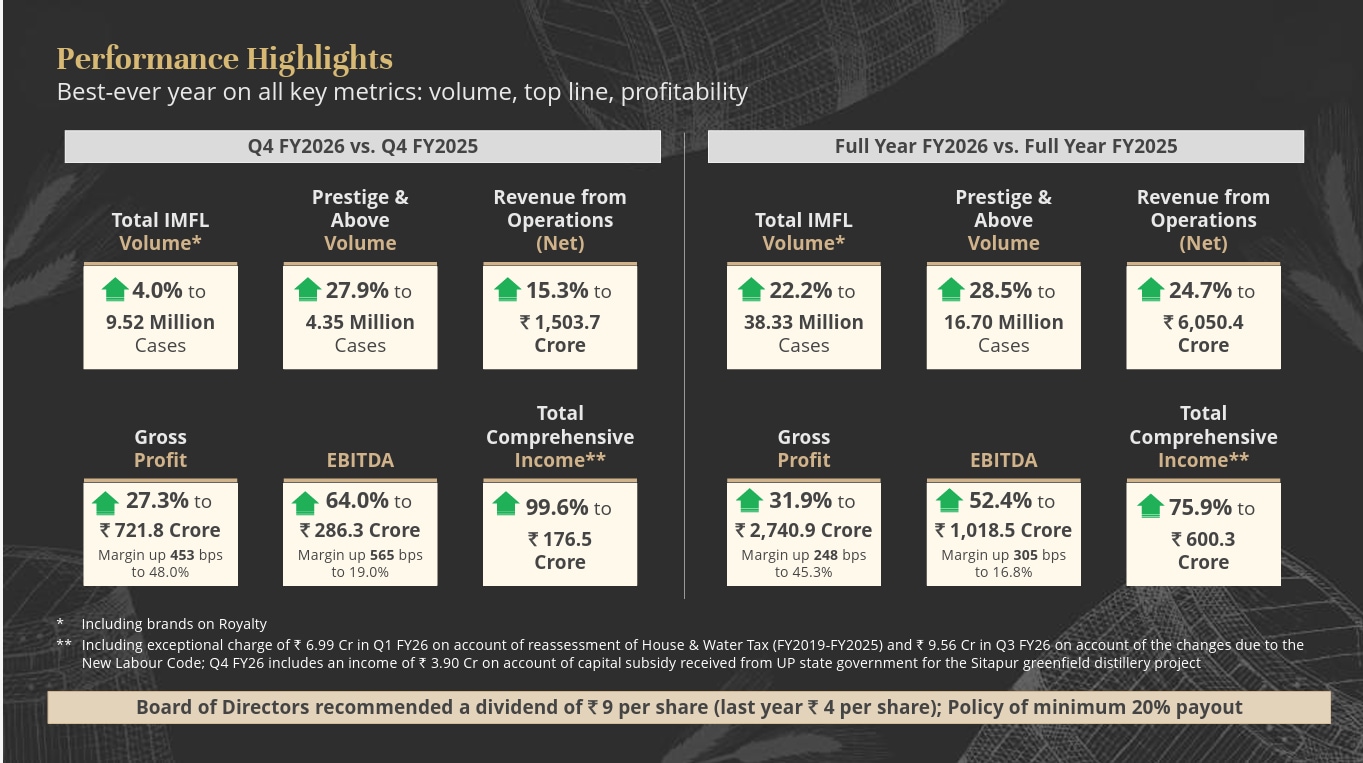

Fourth-quarter net revenue from operations reached ₹1,503.7 crore, growing ~15.31% YoY, while the operating profit jumped 64% to ₹286.3 crore. The total income nearly rose 99.6% to ₹176.5 crore.

Radico Performance Q4 and FY26

That is not the earnings summary of an established portfolio getting incremental benefit from an already premium-heavy base. It is the profile of a business whose product mix is still changing quickly.

And the scale of that transition becomes clearer when volumes are broken down.

The Indian Made Foreign Liquor total volume in Q4 FY26 rose just 4% to 9.52 million cases. But Prestige & Above volumes rose 27.9% YoY to 4.35 million cases. However, the Regular & Others category volumes declined 10.2% YoY.

That deviation is the real story.

Because it shows that growth is no longer being driven uniformly across the portfolio.

The premium segment is now carrying an unequal share of both revenue growth and improved profitability.

The Portfolio Is Still Moving Upward

Unlike United Spirits, Radico is not yet functioning within a fully premiumised collection. The evolution is still happening.

That is visible in how quickly the mix itself is changing. Prestige & Above brands now account for 47.8% of Radico’s own volume, up from 39.1% a year earlier.

On the revenue side, Prestige & Above accounted for 72.2% of IMFL revenue in Q4 FY26, up from 63.4% a year ago.

Those are strangely sharp changes for a liquor business.

And they explain why profits are moving much faster than topline growth.

Gross profit rose 453 basis points YoY to 48%, while the operating margins increased from 13.4% to 19%.

This is not just pricing support. It is a portfolio transformation.

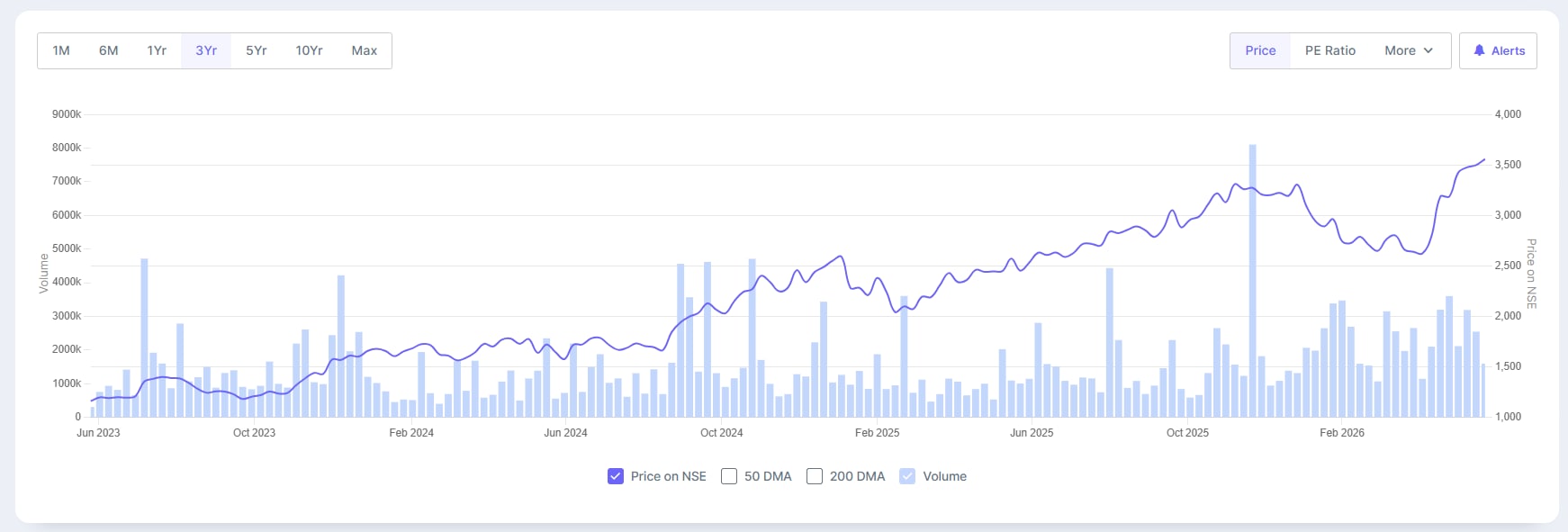

The business is moving from scale-led growth toward value-led growth in real time, and its share price growth reflects the same growth at a CAGR of 45% over the past three years.

Radico Khaitan 3-Year Share Price Trend

Two Growth Levers

Because the premium shift is still in motion, Radico still has two growth levers operating concurrently.

The first is premiumisation itself, moving consumers’ consumption up from regular brands into Prestige & Above offerings.

The second is scale extension within those premium categories.

That combination creates a much more visible growth curve than what a mature premium business usually produces.

Management commentary reflects exactly that positioning. Chairman Lalit Khaitan said the company’s “persistent focus on premiumisation continues to deliver tangible results,” with Prestige & Above volume growth crossing 28% during FY26.

Managing Director Abhishek Khaitan described FY26 as “a clear inflection point,” underlining that Radico crossed both ~₹6,000 crore in net revenue and ₹1,000 crore in Earnings before interest, taxes, depreciation and amortisations (EBITDA) in FY26.

That language shows the company trusts it is in the cycle, not in optimisation mode, but still in growth mode.

The Brands Are Scaling — And That Changes the Earnings Structure

The premium portfolio is no longer contingent on a single breakout label. Multiple brands are now scaling at once across categories.

Magic Moments reached ₹1,500 crore in revenue while volumes reached 8.6 million case sales in FY26, maintaining its large share of India’s vodka market.

After Dark grew 60% during the year and crossed 3.1 million cases. Royal Ranthambore crossed ₹200 crore in revenues, while Rampur and Jaisalmer continued growing globally.

That breadth is important.

Because businesses shifting towards premiumisation often struggle when expansion hangs on only one or two flagship brands.

Radico’s portfolio is now expanding across vodka, luxury whisky, gin, and premium brown spirits concurrently.

That divergence makes the shift to premium more durable and scalable.

Why Margins Are Expanding Faster Here

This is where the contrast with United Spirits becomes clearest.

United Spirits is operating within an already premium-heavy base, where incremental upgrades create smaller jumps in profitability. Radico, by contrast, is still moving consumers through the premium curve itself.

Which means every product mix enhancement generates a larger financial impact.

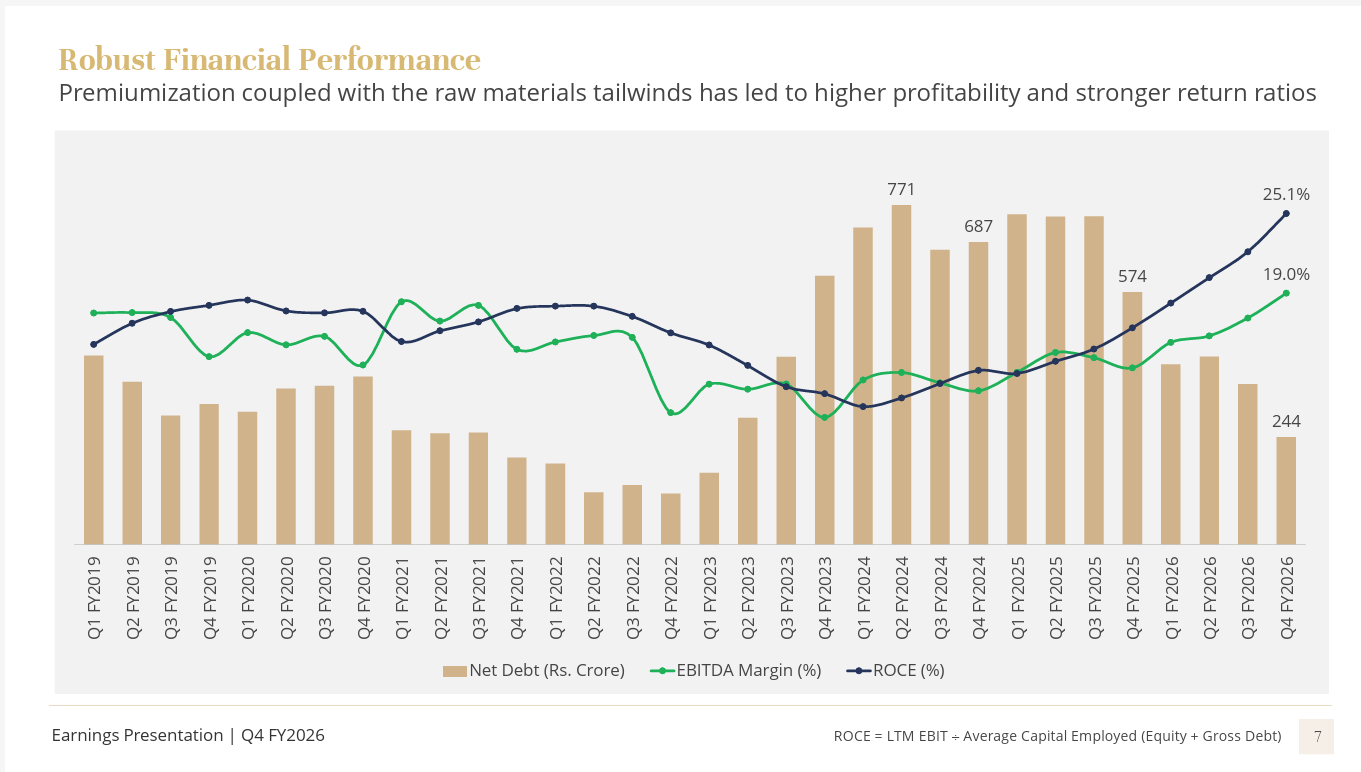

That effect is already visible in the numbers. The operating profits rose even faster, helped by premium product mix advancement, operating leverage, and fairly benign raw material costs.

Premiumisation, coupled with raw-material benefits, led to higher profitability and stronger return ratios.

Radico Net Debt, EBITDA Margins, and ROCE Trend

It’s still not in the stable monetisation stage seen in mature premium businesses.

This is still the high-operating-leverage phase of premiumisation, where the portfolio lift itself is leading outsized earnings expansion.

The Constraint Here Is Still Execution

That also means Radico’s growth comes with a different challenge. The limitation is not saturation. It is the speed of execution.

How quickly can premium brands grow countrywide?

How effectively can supply expand across states?

How long can the company maintain premium growth rates above 25%?

Those questions matter because the portfolio is still changing quickly.

The company continues to invest strongly in luxury positioning, experiential marketing, and premium storytelling. New launches like The Spirit of Kashmyr vodka, Rampur 1943 Virasat, and Morpheus Rare Luxury Whisky show that Radico is still developing the architecture of its premium business rather than just optimising an existing one.

Which is why the numbers still look aggressive. The business is not yet extracting value from a finished premium portfolio. It is still building that portfolio in real time.

The Divergence Is Already Visible, But Not Where the Market Is Looking

At first, both companies seem to be riding the same underlying trend. Premium brands are growing faster, margins are rising, and consumers are moving up across categories.

But the financial behaviour underneath is beginning to split.

At United Spirits Limited, the premium portfolio is now dominant. Incremental gains now come from pricing strength, premium updates within the portfolio, and robust monetisation of an already premium consumer base.

Radico Khaitan, however, is still going through a visible portfolio shift. Revenue growth stays stronger because the premium portfolio itself is still growing aggressively. Margins increase more sharply as the mix shift is occurring in real time.

Which means the profitability rises disproportionately when operating leverage begins to kick in, besides premiumisation. That kind of change alters the financial structure much faster.

The distinction is important.

One business is refining a premium portfolio, and the other is still restructuring one.

The Bigger Shift Is Not in Alcohol, It Is in Indian Consumption Itself

What makes this transition more important is that it is starting to show across consumer sectors in India.

The initial consumption cycle was led mostly by growth, with more consumers entering formal categories, extensive distribution, and first-time upgrades into branded products.

The next stage is increasingly about monetisation.

Companies are now trying to raise the value per consumer instead of increasing the number of consumers.

That shifts the focus toward premium positioning, stronger brand ecosystems, pricing power, and mix improvement.

Alcohol simply makes this transition easier to see because the separation between regular and premium portfolios is strangely noticeable in both volumes and margins.

And that is why the contrast between United Spirits and Radico matters beyond the liquor industry itself.

They are effectively reflecting two different stages of India’s broader premium consumption cycle.

The Question the Market Is Still Answering

The premiumisation trend itself is no longer the debate.

The more important question is how long different companies can continue multiplying once the easy migration stage starts reducing.

For businesses still experiencing a sharp portfolio evolution, growth can stay visibly strong for longer.

For businesses operating within an already premium-heavy base, the challenge turns toward sustaining pricing power, protecting margins, and continuing to deepen consumer value without depending on large volume growth.

That is the divide now emerging inside India’s alcohol market.

And over time, the market may stop valuing premiumisation as one broad theme and start valuing companies based on where they actually are within the cycle.

Want to keep an eye on these stocks? Add them to your watchlist

Disclaimer:

Note: We have relied on data from the Jan 2026 investor presentation, www.Screener.in, throughout this article. Only in cases where the data was not available have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Archana Chettiar is a writer with over a decade of experience in storytelling and, in particular, investor education. In a previous assignment at Equentis Wealth Advisory, she led innovation and communication initiatives. Here, she focused her writing on stocks and other investment avenues that could empower her readers to make potentially better investment decisions.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.