Summary: The biggest beneficiaries of India’s strategic manufacturing push may not build missiles or aircraft. They supply the critical materials that make them possible.

India’s defence manufacturing story is no longer a secret. Investors who identified the theme early have been richly rewarded. The Nifty India Defence index has delivered annualized returns of nearly 57% over the past five years.

Having said that, in the defence universe of stocks, not all companies make fighter jets, missiles, or warships. Instead, they operate much deeper in the value chain, producing advanced alloys, titanium products, and specialty materials that make these defence systems possible. As India aims for being Atma-Nirbhar in defence, aerospace, and nuclear energy, this materials layer could become one of the most important segments of manufacturing.

Two companies stand out in this niche: MIDHANI and PTC Industries.

Not Just Another Defence and Aerospace Story

India has several listed players that have exposure to these strategic sectors. Larsen &Toubro manufactures nuclear reactors. Godrej Aerospace supplies critical components of PSLV. Bharat Forge is a leader in forgings and other defence platforms. MTAR Technologies manufactures highly precise assemblies for space and nuclear applications.

However, MIDHANI and PTC Industries occupy different positions in the value chain. Instead of building finished systems, they operate closer to the advanced materials and metallurgical layer. One of the most technologically demanding segments of manufacturing, where India has historically depended on imports.

MIDHANI – The Materials Backbone

Established under the Ministry of Defence in 1973, MIDHANI is one of India’s leading producers of titanium alloys, superalloys, specialty steels, and other advanced materials used in defence, aerospace, space, and nuclear applications.

This is where MIDHANI’s competitive advantage is evident. Its 10 superalloy product types are certified by NADCAP and CEMILAC, a critical qualification for supplying aerospace and defence programs. Getting these certifications often takes years, which is a big barrier to entry.

PTC Industries – Moving up the Manufacturing Stack

PTC Industries, established in 1963, was a traditional supplier of precision castings to the oil & gas, marine, energy, and petrochemical industries.

In 2020, the company launched its subsidiary Aerolloy Technologies Limited (ATL) and started its journey to become an advanced materials company. PTC is developing capabilities in titanium melting, superalloy manufacturing, and precision-engineered aerospace components with ATL, where India has been heavily import-dependent.

As Aerolloy grows, aerospace and defence become a larger portion of the PTC business mix.

Unlike Midhani, PTC Industries is still in a heavy investment phase.

Last year, PTC commissioned a 6,000-tonne titanium melting and superalloy manufacturing facility, strengthening its capabilities in aerospace-grade materials. Last year, it secured a major order from Safran Aircraft Engines for the supply of aero-engine components that are to be used in Airbus A-320neo and Boeing 737 MAX programs.

Around the same time, PTC received an order worth over ₹100 crores from BrahMos Aerospace for critical titanium components.

Qualification is the Real Moat

In aerospace component manufacturing, the real challenge is not producing a component but becoming an approved supplier. Companies such as Safran, GE Aerospace, and Rolls-Royce require years of testing, audits, and process validation before certifying a vendor.

Once qualified, suppliers often remain part of programs for long periods because switching vendors is not that easy. This creates a strong competitive moat, making contracts from global aerospace players far more valuable than ordinary purchase orders. They signal that a company has crossed one of the industry’s highest entry barriers.

Two Companies, Two Different Stages of the Same Opportunity

At first glance, MIDHANI and PTC Industries seem to be in the same business. But the way they make money is quite different.

MIDHANI is an established strategic materials company with over five decades of operational experience. Today, specialty alloys and metals for government programs are their primary source of revenue.

Meanwhile, PTC Industries is still in the process of building capabilities. Aerolloy Technologies is investing heavily in titanium melting, superalloy, and advanced aerospace components manufacturing. The company is looking to move beyond precision castings and establish itself as a global supplier of strategic materials and high-value components.

The difference is also apparent in the financials and valuations.

Financial Comparison: MIDHANI vs PTC Industries

MIDHANI vs PTC: Scale vs Growth

| Metric | MIDHANI | PTC Industries |

| Market Cap (2nd June 2026) | ₹7,751 Crore | ₹29,013 Crore |

| 5-yr Compounded Sales Growth | 12% | 30% |

| 5-yr Compounded Profit Growth | -6% | 101% |

| Operating Margin – FY26 | 20% | 22% |

| ROCE- FY26 | 11% | 8% |

| Order Book | ₹2,290 Crore | – |

| Order Book-to-Revenue Ratio | 1.9 | – |

MIDHANI’s numbers reflect a mature business. Revenue has grown at a 12% CAGR over the last five years, and profits have declined at a 6% CAGR.

Despite its dominant position in specialty alloys and strategic materials, growth has remained limited by low asset utilization. Its asset turnover ratio improved marginally to 0.39x in FY26 from 0.37x in FY25, indicating that a significant portion of its capacity remains unutilized. So the healthy operating margins of about 20% have not translated into correspondingly strong returns.

PTC Industries is an entirely different story. Revenue has grown at a robust 30% CAGR over the past five years, while profits have expanded at 101% CAGR.

As the company is still in the middle of a major investment cycle, its ROCE remains modest at 8%.

Unlike MIDHANI, PTC doesn’t report a consolidated order backlog. Instead, visibility comes from individually announced contracts and long-term aerospace supply contracts.

The Hidden Margin Driver

The more interesting part of the PTC story lies beneath the headline growth numbers.

Aerolloy Technologies, PTC’s advanced materials subsidiary, contributed only about 22% of consolidated revenue in 9MFY26. Yet, it generated roughly 41% of consolidated EBITDA with margins of nearly 39%.

It has significant implications for future profitability. As Aerolloy’s share of revenue increases, PTC’s profitability could improve meaningfully, even if the legacy castings businesses do not see much material growth.

Valuations: A Story of Expectations vs Execution

The valuation gap between MIDHANI and PTC Industries is striking.

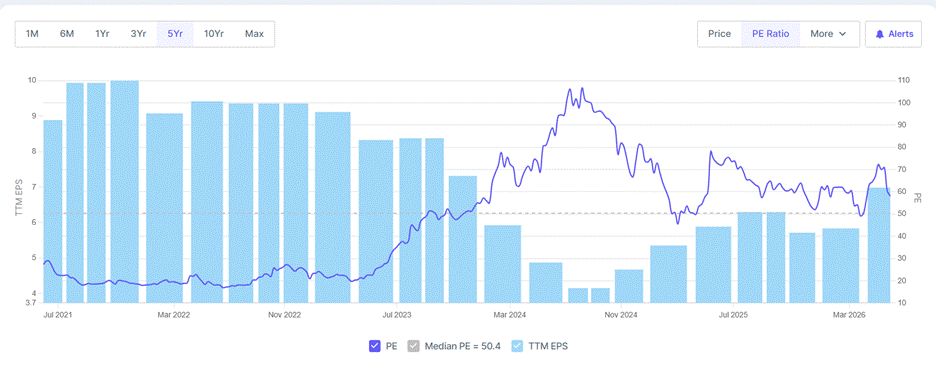

MIDHANI Price-to-Earnings Trend

As of 2nd June 2026, MIDHANI is trading at a PE of 59, near its 5-year historical median of 50x. The stock trades at a premium, but the market has not given it higher valuations due to its declining earnings profile and execution challenges.

PTC Industries, on the other hand, is a different story. The stock trades at a PE of 286, closer to its 5-year historical median PE of about 280, making it one of the most expensive industrial stocks in the market.

PTC Industries Price-to-Earnings Trend

At first glance, such valuations appear difficult to justify. However, investors are not valuing PTC based on its current earnings. They are valuing it based on the earnings they expect the company to generate once its titanium melting, superalloy manufacturing, and aerospace component businesses reach scale.

The recent results offer an example of this dynamic. PE fell sharply after a 3X jump in EPS (Earnings Per Share) in Q4FY26, from a near 360 level to around 280.

This highlights an important distinction. PTC’s investment thesis depends on earnings catching up with expectations. If the company continues to execute and the newly commissioned facilities achieve higher utilization, earnings growth could gradually justify the current valuation.

For MIDHANI, the challenge is different. The company already possesses strategic capabilities and an established customer base. What investors are waiting for is a meaningful acceleration in growth and profitability. Until that happens, valuations will be compressed relative to PTC Industries.

Why Nuclear Power Matters

By 2047, India wants to expand its nuclear power capacity to 100 GW from roughly about 9 GW, a more than 12-fold increase. Such an expansion would require a large volume of specialized materials for use in reactor vessels, steam generators, piping systems, and other critical components.

Unlike conventional industrial projects, nuclear plants operate under extreme temperature, pressure, and radiation conditions for decades, creating demand for high-performance alloys and specialty metals. For companies such as MIDHANI, which already supplies strategic materials to India’s nuclear and defence sectors, the opportunity extends beyond a single project cycle.

The Road Ahead

The investment case for both MIDHANI and PTC Industries ultimately rests on India’s ability to build globally competitive capabilities in advanced materials. Tailwinds are hard to ignore.

For MIDHANI, the opportunity lies in better utilization of the capacities it has already built. The company enjoys a strong position in strategic materials, but future shareholder returns will depend on whether demand from defence, aerospace, and nuclear sectors can translate into higher asset utilization and improved returns on capital.

For PTC Industries, the story is more execution-driven. If Aerolloy continues to scale and PTC secures additional global aerospace contracts, the company could emerge as a significant player in a niche segment where India has historically lacked.

The risks, however, are equally clear. While MIDHANI’s challenge is growth, PTC must justify its valuations through constant execution. Any delays in capacity ramp-up, customer qualification, or order conversion could test investor patience, leaving little room for error.

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Deepan Datta has spent over a decade studying stocks and mutual funds. His passion is to uncover interesting stories in the financial markets and share them through his writings with investors at large. He is focused on delivering clear, easy to understand and research-backed insights. Deepan began his career as a Research Associate at S&P Global, where he developed a strong foundation in financial research and data analysis.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.