Ace Investor Akash Bhanshali has quietly built over Rs 800 cr position that sits on both sides of India’s energy shift. He owns the company that builds the wind turbines, and the one that makes the kit to plug them into the grid. It is a two-handed bet that most retail investors have walked straight past.

The Rs 800 cr Power Grid Bet by The ENAM Veteran

While much of the market spent the past year chasing flashy solar and power names at eye-watering valuations, ace investor Akash Bhanshali has been doing something far less crowded. He has been silently trusting the plumbing of India’s power system. Bhanshali, who carries an Enam pedigree and is known for taking a handful of concentrated, long-term bets rather than spraying money thinly, now sits on a disclosed equity pile worth over Rs 6,590 cr per Trendlyne.

Two of his holdings stand out because they tell one story. One is a relatively fresh entry that is in the business of manufacturing Wind Turbine Generators (WTGs) and is a wind energy solutions provider. The other is a much older holding, which is engaged in the business of manufacturing, designing, building and servicing technologically advanced products and systems for the electricity network

So, while the country is generating a lot more green energy, every unit of it has to be carried, stepped up and pushed safely into the grid. And these two favourites of Bhanshali do that. One company makes the power and the other one moves it.

But the two stocks could not look more different on paper. One is a turnaround story that almost went under a few years ago. The other is a high-quality compounder trading at a price that makes value investors interested, which Bhanshali has been quietly trimming. So, is this a clean play on India’s grid build-out, or two very different risk bets wearing the same green jacket? Let us dig into both.

Inox Wind Ltd: The Wind Turbine Turnaround

Inox Wind is part of the INOXGFL group and is one of the few fully integrated wind energy players in India. In plain terms, it does not just sell turbines. It handles the whole job, from picking the site to building the wind farm and then maintaining it for years afterwards.

With a market cap of around Rs 14,569 cr, the company is a fully integrated player in the wind energy market and provides end-to-end turnkey solutions.

Bhanshali is a relatively new face on this share register. He stepped in around the middle of 2025 and, as per trendlyne, now holds a 1.8% stake of close to 3.03 cr shares, worth Rs 255 crore. What makes the timing interesting is that he bought after the stock had taken a heavy beating, not during the hype.

Financials: Analyzing the Turnaround Metrics

The financials explain why a value-minded investor would even look.

| Financial Year | FY21 | FY22 | FY23 | FY24 | FY25 | FY26 | 5-Yr CAGR |

| Sales (Rs cr) | 711 | 625 | 733 | 1,746 | 3,557 | 4,397 | 44% |

| EBITDA (Rs cr) | -191 | -300 | -193 | 262 | 757 | 891 | Turnaround |

| Net Profit (Rs cr) | -307 | -483 | -712 | -48 | 438 | 449 | Turnaround |

The sales of the company jumped from Rs 711 crore in FY21 to Rs 4,397 crore in FY25, a compound growth of 44% over five years. However, the bigger story sits below the top line. Back in FY21 the operating profit was a loss of Rs 191 crore. By FY26 it had flipped to a positive Rs 891 crore, with margins climbing past 20%. Because the starting point was a loss, a neat EBITDA growth number does not really exist here. What exists is a full turnaround.

The bottom line followed the same arc. The company lost Rs 307 crore in FY21 and ended FY26 with a net profit of Rs 449 crore, which once again is a turnaround. This is not steady compounding. It is a business that was bleeding and then stopped, which is exactly the kind of inflection a patient investor likes to catch early.

Valuation Paradox: Analyzing the Recent 50% Correction

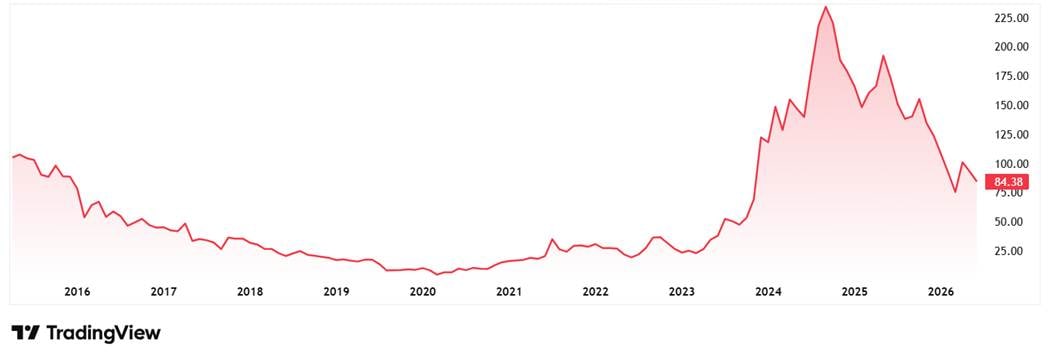

The share prices of Inox Wind say a lot about the rough ride in between. The price was around Rs 20 in June 2021 and as of closing on 2nd June 2026 it was Rs 84, which is a jump of 320% in 5 years.

Inox Wind Long Term Share Price Chart

Going by the stock’s five-year price CAGR of 33% on screener, Rs 1 lac put into the shares five years ago would be worth roughly Rs 4.2 lac today. Yet the same stock is down about 50% over the last year, swinging between a 52-week high of Rs 187 and a low of Rs 75. So, the long-term chart looks great while the recent one looks not so good, and Bhanshali possibly used this second part to get in.

On valuation, the stock trades at PE of about 36x and the industry median currently is also 36x. The 10-Year media PE for the company is 26x while the industry median for the same period is 40x.

Operating Efficiency: Cleaner Balance Sheets, Stretched Promoters

The return on capital employed (ROCE), which tells you how much profit the company squeezes out of the capital it puts to work, is about 11%, and the return on equity (ROE) is close to 7%. Decent, not dazzling. The company has also cut debt, though it is worth flagging that promoter holding has slid from roughly 73% to around 44% over three years, which is something to keep an eye on.

The recent numbers keep the turnaround story alive. At the group level, INOXGFL is moving to absorb Wind World’s 600 MW power-producing assets and a 4.5 GW maintenance book, while the company readies a new, larger turbine platform. With India still pushing hard on its renewable energy capacity targets, the demand backdrop is real. The question is whether Inox can stay disciplined this time.

Schneider Electric Infrastructure: High-Moat Compounding at a Premium

If Inox Wind is the risky turnaround, Schneider Electric Infrastructure is the polished one. Incorporated in 2011, the company makes the heavy electrical gear that sits between a power source and your switch: transformers, switchgear, protection relays, and the automation and smart-grid software that keeps it all stable. It is the equipment that captures volatile wind and solar power and steps it safely into the grid. The company is 75% owned by its French parent, Schneider Electric, so what trades in the market is a fairly thin slice of the float.

With a market cap of Rs 28,226 cr, the product portfolio of the company includes Transformers, Power Transformers, Switchgears (Primary & Secondary Switchgears), Medium Voltage Switchgear, Protection Relays, Differential Relay, Electricity distribution management systems, a software suite for self-healing smart grid, e-House & smart cities applications.

Bhanshali originally accumulated this stock in March 2018; according to Trendlyne. He currently holds about 2% of the company, roughly 47.2 lakh shares worth Rs 557 crore. Here is the twist that the headlines miss: he has been cutting, not adding. He trimmed the stake from 2.3% down to under 2% in the latest quarter, booking some profit after a big run.

The Numbers That Possibly Caught Bhanshali’s Eye

The reason for that run you read above is in the financials.

| Financial Year | FY21 | FY22 | FY23 | FY24 | FY25 | FY26 | 5-Yr CAGR |

| Sales (Rs cr) | 1,297 | 1,530 | 1,777 | 2,207 | 2,637 | 2,891 | 17% |

| EBITDA (Rs cr) | 64 | 86 | 168 | 296 | 383 | 371 | 42% |

| Net Profit (Rs cr) | -1 | 28 | 124 | 172 | 268 | 213 | 194% |

Sales rose from Rs 1,297 crore in FY21 to Rs 2,891 crore in FY26, a compound growth of 17% over five years. The profit engine, though, did far more of the heavy lifting. EBITDA climbed from Rs 64 crore in FY21 to Rs 371 crore in FY26 logging a compound growth of 42%, with margins jumping from about 5% to 13%. When it comes to net profits, the company logged losses of Rs 1 cr in FY21 and for FY26 it was Rs 213 cr, which is a big turnaround story.

Regarding quality metrics, the ROCE is about 30% while the industry median is 24%. The ROE is 36%, meaning for every Rs 100 of shareholder money in the business, the company has lately been generating around Rs 36 of profit. The industry median is about 19%. This is what a high-moat industrial looks like when it finally fires.

Why a 127x PE Limits Room for Error

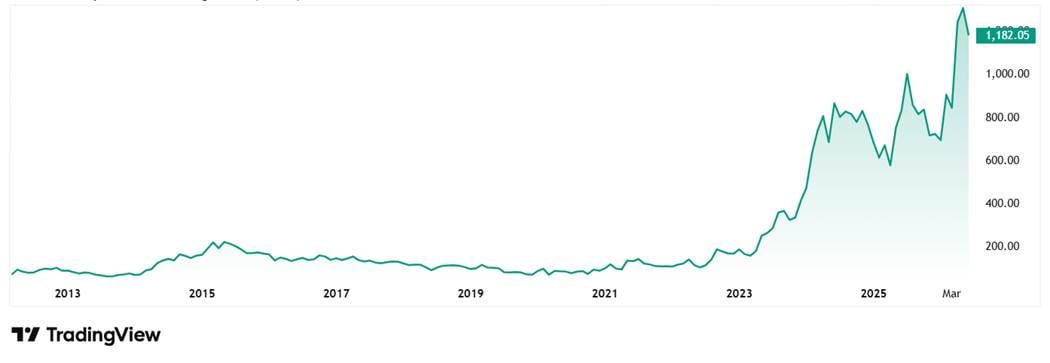

The share price of Schneider Electric was about Rs 123 in June 2021 and as of closing on 2nd June 2026 it was Rs 1,181, which is a jump of 860% in 5 years. Rs 1 lac invested in the stock 5 years ago would have been around Rs 9.6 lacs today.

The stock is trading at a PE of around 127x, well above the current industry median of 36x. The 10-year median PE for the company is 80x and the industry median for the same period us 40x. The simple read is that this is a strong business at a far-from-wonderful price, which is most likely why Bhanshali chose to take some money off the table rather than buy more. But the point is, he still holds 2%, which shows his trust in the stock.

In recent news about the company, it approved its FY26 results in late May 2026 and reappointed Udai Singh as Managing Director and CEO, and it carries a healthy .

The company secured a robust Rs 3,430 cr in new order inflows during the full fiscal year (up 27.4% YoY), including Rs 772 cr bagged during Q4FY26 alone.

Following the Buyer or the Capital Allocator?

Seen side by side, Bhanshali’s pair of bets is less about picking one winner and more about funding both ends of the same shift. Inox Wind generates the green power. Schneider Electric Infrastructure carries and controls it. You cannot scale one without the other, and he owns a piece of each.

There is a deeper thread too. His single largest holding is Gujarat Fluorochemicals, worth nearly Rs 1,907 crore, which is also part of the INOX group, the same house as Inox Wind. So, his tilt towards the energy transition runs through more than one door.

What is striking is how differently he treats the two grid stocks. With Inox Wind he is the bargain-hunter, stepping into a beaten-down turnaround and waiting for the recovery to play out. With Schneider he is the disciplined seller, locking in gains on a quality name that has simply got too expensive. The risks are equally split. Inox carries a patchy history, stretched receivables and a falling promoter stake, while Schneider carries a price tag that leaves almost no room for a stumble.

The real question for the rest of us is which version of Bhanshali to follow. The one buying the cheap, messy turbine maker, or the one quietly selling the expensive, brilliant grid company? He is doing both at once, and only the next few quarters will show which hand was the smarter one.

Add these stocks to a watchlist and keep an eye on them so you do not miss any big moves.

Note: We have relied on data from http://www.screener.in and http://www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, he was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article. The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.