Most investors looking at Rossell Techsys would focus on its strong growth, rising order book, and ties with global aerospace companies such as Boeing and Lockheed Martin.

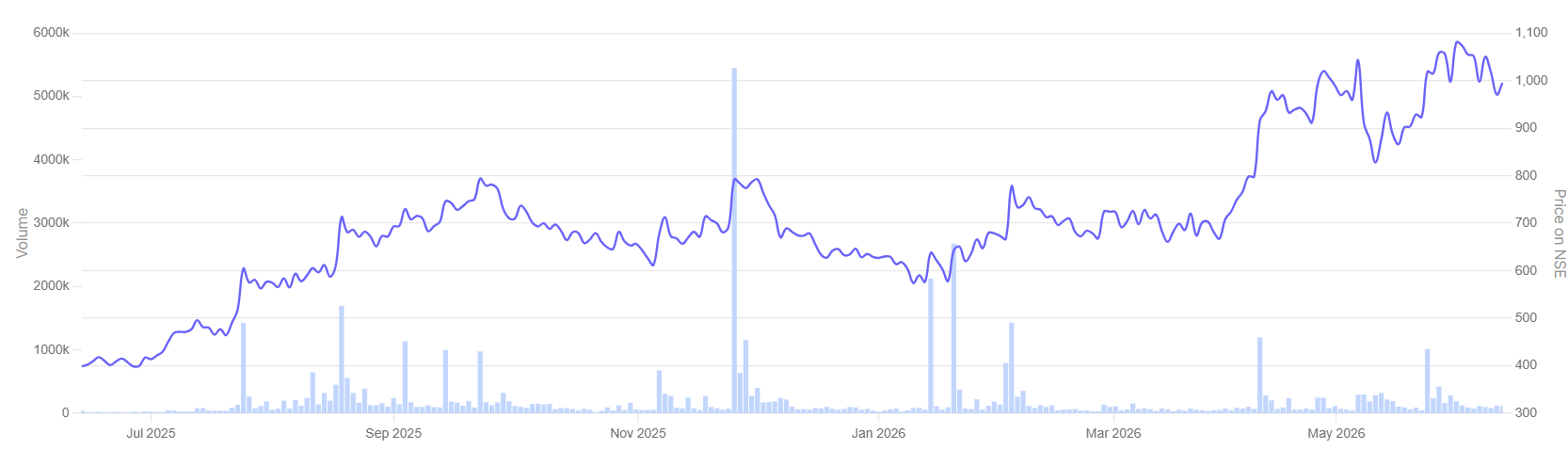

The numbers support that view. Revenue almost doubled in FY26, while exports account for almost all of the company’s sales. The stock has also more than doubled in the last one year.

Rossell Techsys 1-yr Stock Price Performance

But a larger story may be unfolding behind these numbers.

Rossell no longer wants to be just an aerospace supplier. The company is gradually building a presence across aerospace, defence, space, and semiconductors. Four sectors that are expected to attract significant investments over the next decade.

The key question for investors is no longer whether Rossell can grow. Growth is already visible. The bigger question is whether the company can leverage its expertise to become a broader high-technology manufacturing platform.

Aerospace Supply Chains Are Changing

For decades, global aerospace manufacturing was concentrated among a handful of countries and suppliers. That model is slowly changing.

Several factors are driving the shift. The increase in global defense spending, increased geopolitical risks, and supply chain disruptions during the pandemic have shown risks of depending on a narrow supplier base.

NATO countries, in particular, are under pressure to increase their defence spending from 2% to 5% of their GDP. That is driving fresh investments into defence platforms, missile systems, and related systems.

At the same time, aerospace manufacturers are struggling with labour shortages and supplier bottlenecks. Aircraft production is increasing, but many suppliers are finding it difficult to keep pace. This is creating opportunities for qualified suppliers in new regions.

India is emerging as one of the major beneficiaries, with its rapidly expanding domestic aerospace ecosystem. Rossell Techsys appears to be benefiting directly from this trend.

Where Does Rossell Techsys Fit in The Value Chain?

Rossell Techsys was founded in 2011 as the Aerospace and Defence division of Rossell India. The company initially worked as an offset partner for global aerospace and defence companies that had won contracts in India.

Today, Rossell manufactures wire harnesses, electrical interconnect systems, control panels, and automated test equipment used in fighter aircraft, defence platforms, satellites, and semiconductor manufacturing equipment.

These products may not appear complex at first glance. But they perform a critical function. They are the electrical nervous system of complex machines, carrying power, data, and signals between subsystems. A failure in one component can affect the performance of the entire platform.

In 2013, Rossell made the first breakthrough when Boeing selected it to supply wire harnesses for the F/A 18 Super Hornet fighter jets. For Rossell, it was not just an order. It validated their manufacturing capabilities before one of the world’s most demanding customers.

Rossell Sells Reliability, Not Wire Harnesses

Many assume Rossell’s business is simply manufacturing wire harnesses. But that view is incomplete and misses the competitive advantage.

In aerospace and defence, customers don’t pay for the product. They pay for reliability. Every component must meet strict quality standards. Every part must be traceable. Every process must be documented. Failure is rarely an option.

As a result, becoming an approved supplier can take years, which acts as a strong entry barrier.

Certifications play a key part in creating these barriers. Rossell is accredited to AS9100 and NADCAP and holds customer-specific accreditations required by leading aerospace and defence OEMs. It is also a CEMILAC-approved design house and a member of IPC, RTCA, and ERAI. These approvals signal the ability to meet stringent standards for quality, traceability, reliability, and process control.

Now, Rossell is attempting to leverage the same qualification-driven playbook to pursue its next phase of growth.

Growth Is No Longer Coming From Aerospace Alone

The most significant development at Rossell may not be happening inside its aerospace business. It is happening outside.

Today, aerospace & defence contribute roughly 70% of revenue. Management expects this share to fall to around 50% by FY27. This doesn’t mean the aerospace growth is slowing. It’s because newer businesses are growing faster. The company is expanding into space and semiconductor equipment manufacturing.

In the space segment, Rossell has secured a multi-year contract from Amazon valued at approximately ₹400 crores.

In semiconductors, the company has partnered with a customer that has a large supply chain base in South Korea and is in discussion with another major player. Management has set a target of generating $200 million in revenue from this segment over the next three to five years.

In FY27 alone, management is expecting 300 to 400% growth from the semiconductor and space segments.

Aerospace, however, remains the key growth pillar. Through its partnership with Boeing, it is participating in the Boeing T-7 Red Hawk trainer aircraft program and has disclosed strategic agreements worth approximately $200 million linked to the platform.

As a result, Rossell is gradually evolving from a pure-play aerospace supplier into a high-technology diversified manufacturing company.

Capacity Expansion Reflects Confidence in Demand

Management’s biggest vote of confidence isn’t in words. It’s in capacity expansion.

Rossell currently operates from a 225,000 sq ft facility in Bangalore’s Defence and Aerospace Park. During previous earnings calls, the management stated that the facility was already running at 1.5 shifts and had little room left to accommodate additional work. The original plan was to construct another facility of 150,000 sq ft on the existing campus at an investment of ₹70 crore over an 18-month construction timeline.

A few months later, management changed its mind and decided to lease a 210,000 sq ft facility adjacent to its existing facility from April 2026 rather than waiting for construction. The rationale was simple. A new facility would take time to build, and could hold up growth plans.

This change is noteworthy. Companies rarely commit to such a large increase in capacity unless they have reasonable visibility into future demand.

The new facility will house the semiconductor and space programs. More importantly, management believes the new facility could eventually generate revenue comparable to the existing operation.

Financials Reflect Aggressive Business Scale-up

Rossell’s financial performance is hard to ignore. However, if you had looked at the company a year ago, the numbers might not have excited you. Revenue and profit were growing at a measured pace and were largely linear. That sharply changed in FY26.

Rossell Techsys Financial Performance

| FY24 | FY25 | FY26 | |

| Sales (₹ crores) | 217 | 260 | 485 |

| Operating Profit (₹ crores) | 32 | 35 | 63 |

| Operating Margin (%) | 15 | 14 | 13 |

| Net Profit (₹ crores) | 11 | 8 | 22 |

Revenue jumped 86% to ₹485 crores from ₹260 crores in FY25, while net profit nearly tripled to ₹22 crores. Operating margins, however, declined by one percentage point to 13%.

Most importantly, the management feels this is only the beginning. During a recent earnings call, Managing Director Rishab Gupta particularly said, from its founding in 2011 through March 2025, Rossell generated roughly ₹1,300 crore in cumulative revenue over 14 years. It now expects to generate a similar amount of revenue in just the next two financial years.

But this should not stop you from going deeper into the cash flows, where the real problem lies.

The Cash Flow Question Deserves Attention

Despite strong revenue growth, Rossell has reported negative operating cash flow in each of the last two financial years.

Rossell Techsys: Cash Flow Statement (in ₹ crore)

| FY24 | FY25 | FY26 | |

| Cash From Operating Activity | 1 | -42 | -83 |

| Cash From Investing Activity | -11 | -14 | -23 |

| Cash From Financing Activity | 11 | 59 | 149 |

Cash flow from operations declined from ₹1 crore in FY24 to negative ₹42 crore in FY25 and further to negative ₹83 crore in FY26. This means profits are not turning into cash.

At the same time, the company continued investing in capacity expansion and new programs. Cash flow from financing activities rose from ₹11 crore in FY24 to ₹149 crore in FY26, indicating that a significant portion of growth is currently being funded through external borrowings.

The root cause is the company’s inventory-heavy business model. Rossell ended FY26 with ₹289 crore of inventory against annual revenue of ₹485 crore, equivalent to about 7 months of sales, resulting in higher cash conversion cycles. Aerospace programs require the company to procure materials well in advance, often 12-18 months before delivery, which locks up large amounts of capital.

Even large aerospace and defence companies like Hindustan Aeronautics have cash conversion cycles of more than 700 days. Bharat Electronics and Data Pattern have cash conversion cycles of 342 days and 499 days, respectively.

Higher Working Capital Requirement Fix

Management has outlined several initiatives to address higher inventory days and working capital requirements.

They are adopting a distributor-held inventory model, where inventory remains with the distributor until it is needed for production. This reduces the amount of capital locked up on Rossell’s balance sheet while maintaining supply-chain reliability.

The company is also negotiating advance payments from customers and adding price-adjustment clauses to contracts. The most important change, however, could come from the evolving business mix. As the share of revenue from space and semiconductor increases, it could meaningfully reduce the working capital requirements.

Going forward, the business mix may be one of the most important metrics to track.

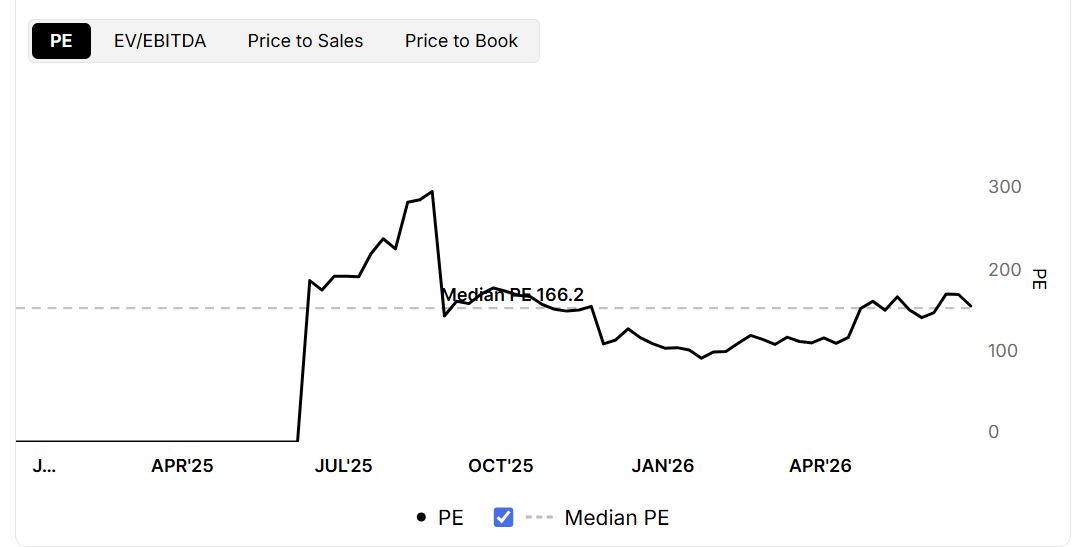

Valuation: The Market Is Already Pricing in Strong Growth

Rossell’s valuation reflects the market’s optimism about its future growth potential.

Rossell Techsys: P/E Multiple Trend Chart

The stock currently trades at around 170 times trailing earnings, broadly in line with its median valuation of 166x over the last year. On a conventional basis, this may look expensive. However, it’s important to note that the earnings base is still small and the company is still in an investment phase. A high-growth aerospace supplier can look expensive on trailing earnings but become much cheaper when growth materializes.

A Different Kind Of Aerospace Story

Most aerospace ancillary companies spend years trying to secure a place inside global supply chains. Rossell has already crossed that hurdle and has become a preferred supply chain partner.

However, the next phase of growth is more challenging. The debate has moved from whether it can win customers to execution. Can the company expand successfully across aerospace, space, and semiconductor markets at the same time? Can it improve margins while scaling operations and translate into stronger cash generation?

Management is attempting to transform Rossell from an aerospace supplier into a diversified high-technology manufacturing company. If successful, Rossell could become one of India’s most important engineering exporters over the next decade.

If execution falls short, the current valuation leaves limited room for disappointment. The next few quarters will determine which path the company follows.

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Disclaimer:

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Deepan Datta has spent over a decade studying stocks and mutual funds. His passion is to uncover interesting stories in the financial markets and share them through his writings with investors at large. He is focused on delivering clear, easy to understand and research-backed insights. Deepan began his career as a Research Associate at S&P Global, where he developed a strong foundation in financial research and data analysis.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.