Despite recent stock corrections, JM Financial initiated coverage on Hindustan Aeronautics, with a ‘Buy’ recommendation. The brokerage said that the ‘risk-reward seems favourable at this stage’ and sets a target price of Rs 4,875, implying an upside of 25% from the current market price.

The analysts expect that the defence aeronautics firm will see significant revenue growth driven by a massive “induction wave,” as the Indian Air Force (IAF) attempts to fill up a depleting fleet and address a multi-billion dollar order pipeline.

Let’s deep dive a bit more on why JM Financial picked HAL –

JM Financial on HAL: Critical fleet shortage in the IAF

The IAF currently operates only 29 squadrons, well below its sanctioned strength of 42. With several legacy platforms like the MiG-29 and Jaguar set to retire in the 2030s, this is where HAL comes into play. The company is positioned as the primary indigenous provider to address this critical gap through new aircraft inductions and fleet upgrades.

JM Financial on HAL: Massive addressable order pipeline

The total addressable order prospects approximately Rs 9.2 lakh crore in the air defence segment over the next 6–7 years. In its “base case” scenario, JM Financial expects that HAL could see order inflows of roughly Rs 4.75 lakh crore from this pipeline.

JM Financial on HAL: Manufacturing-led revenue growth

HAL is likely to achieve an overall revenue CAGR of 21% over FY26–28. This growth is expected to be led by a 50% CAGR in the manufacturing segment, primarily backed by deliveries of the LCA Tejas Mk1A, the HTT-40 trainer aircraft, and the LCH Prachand helicopter.

JM Financial on HAL: Expected margin compression

As the company move towards manufacturing of large platforms, the company’s EBITDA margins are expected to contract moderately (from 29.8% in FY26 to 28.6% in FY28). The reason is simple: manufacturing of large platforms involves a high share of imported components, which typically offers lower gross margins than other segments.

JM Financial on HAL: Valuation metric

The brokerage house valued the stock at a historical average of 29x, on the back of a strong prospect pipeline. However, it was partly offset by potential risks to prospects’ translation to order inflows and execution dependence on other vendors for critical supplies.

Nonetheless, the stock has corrected 22% in the last six months versus 8% fall in the Nifty and, thus, seems to price in most of the headwinds. “Hence, the risk-reward seems favourable at this stage,” said JM Financial.

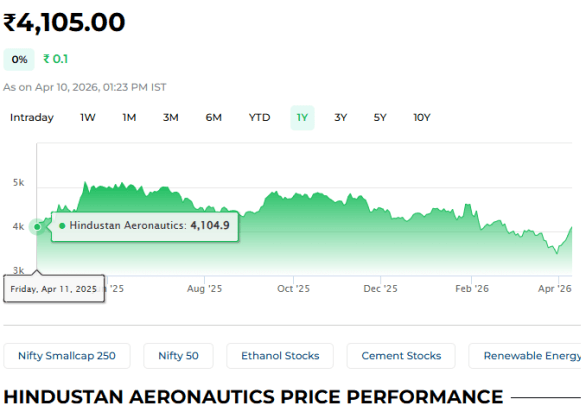

HAL share price performance

The share price of Hindustan Aeronautics has risen 12% in the last five trading days. The stock has increased 1.8% in the past one month and has declined 15% in the last six months. HAL’s share price has changed a little over the previous 12 months.

HAL Q3FY26 results

The firm reported a consolidated profit after tax (PAT) of Rs 1,866.68 crore in Q3FY26, rising 29.64% year-over-year, compared with Rs 1,439.83 crore posted in the same quarter a year back.

Its revenue from operations grew 10.65% YoY to Rs 7,698.8 crore in the third quarter of the current financial year, compared to Rs 6,957.31 crore in the year-ago period.