For three decades, Vijay Kedia has sold the market the same idea. Find a company that is Small in size, Medium in experience, Large in aspiration and Extra-large in market potential. He calls it the SMILE test. Most of his big wins came from buying these names early, sitting tight, and letting time do the heavy lifting.

The March 2026 shareholding filings show a busier Kedia than usual. In one quarter, he took fresh stakes in 2 companies. Both sit in different corners of the market: solar manufacturing and crop protection. Neither is a household name. One of them is listed on the BSE SME platform, where the rules and the risks are not the same as the main board.

That is the story worth telling. Not just what Kedia bought, but how far down the size ladder he is now willing to reach, and what an ordinary investor should weigh before following him there. Let us dive in to find out more.

#1 Websol Energy: Balancing a 1.35 GW Capacity Turnaround Against Low Promoter Holdings

Founded in 1990 and based in Falta, West Bengal, Websol Energy makes photovoltaic solar cells and modules under the Webel Solar brand. After years of false starts, the company has had a remarkable turn.

With a market cap of Rs 4,767 cr, Kedia bought 1% stake in the company, which is over 44 lakh shares worth Rs 49 cr currently.

The financials explain the excitement. Let us look at the standalone numbers for Websol to get a better long-term perspective.

| Financial Year | FY21 | FY22 | FY23 | FY24 | FY25 | FY26 | 5Yr CAGR |

| Sales (Rs Cr) | 154 | 213 | 17 | 26 | 575 | 1,049 | 47% |

| EBITDA (Rs Cr) | 34 | 26 | -13 | -1 | 253 | 429 | 66% |

| Net profit (Rs Cr) | 49 | 10 | -24 | -121 | 155 | 303 | 44% |

| OPM % | 22% | 12% | -74% | -5% | 44% | 41% | – |

In FY26, sales crossed Rs 1,000 cr for the first time and net profit hit Rs 303 cr. Return on capital employed sits at a striking 63%, and return on equity at nearly 67%. The five-year sales growth works out to 47% a year, and profit growth to 44% in the last 5 years, per Screener.

The table tells you why this is both a turnaround and a risk. As recently as FY24, the company was deep in the red. The leap since is real, but it is built on a fresh capacity ramp to 1.35 GW, and a single year of clean profit.

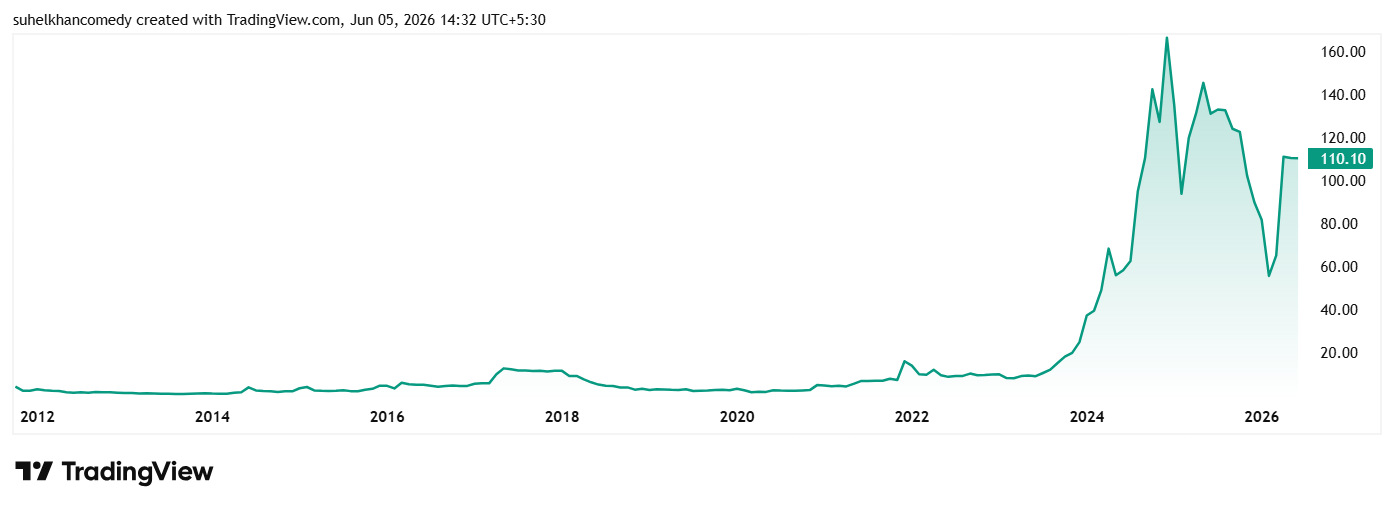

The share price of Websol was around Rs 6 in June 2021 and as on 5th June 2026 it was Rs 110, which is a jump of over 1,700% in 5 years.

Websol Energy Long Term Price Chart

Current PE for the stock is 16x and the industry median is 28x. The 10-year median PE for the company is 18x, while the industry median for the same period is again 28x.

As per the latest investor presentation from May 2026, the company had a strong order book of Rs 1,161 cr at the end of March 2026.

The big red flag is that the promoter holding is low at just under 30%, and promoters have pledged 89% of that holding. The stock also trades at nearly eight times book value. Kedia’s new 1% stake shows he is paying up for momentum, not buying a forgotten name.

#2 Mahamaya Lifesciences: Scale Expansion vs Negative Cash-Flow Traps

The next pick is Mahamaya Lifesciences, incorporated in 2002, engaged in manufacturing, registration and export of finest crop protection products and bioproducts for crop & soil health management.

With a market cap of Rs 381 cr, the company manufactures pesticide formulations and supplies bulk products to Indian agrochemical companies and multinational corporations (MNCs). It imports scientifically researched molecules, secures registrations with the Central Insecticides Board, and develops these molecules into technical-grade and value-added formulations, which are marketed to domestic manufacturers and global MNCs.

Kedia bought a 4.5% stake in the company through Kedia Securities Private Limited, as per the filings for the quarter ending March 2026, which is currently worth over Rs 17 cr.

The Liquidity Catch: Navigating Light Disclosures on BSE’s SME Platform

Mahamaya trades on the BSE SME platform, and that changes the game in ways retail buyers often miss. SME stocks trade in large minimum lots, so the entry ticket is high. Volumes are thin, which means getting out at a fair price is not guaranteed on a bad day. Disclosure is lighter too. Mahamaya, for instance, reports results every six months rather than every quarter, so investors see less of the engine room. Smaller floats also make these counters easier to move, up or down, on modest buying.

None of this makes them bad businesses. But it does mean Kedia stake carries a different weight than the same number on a large, liquid stock. When a big name owns a chunk of a thinly traded SME counter, the price can run far ahead of the fundamentals on sentiment alone. That is a feature of the platform, not a verdict on the company.

Let us look at the financials to see if we can find out what caught Kedia’s attention.

| Financial Year | FY22 | FY23 | FY24 | FY25 | FY26 | 4Yr CAGR |

| Sales (Rs Cr) | 90 | 137 | 161 | 264 | 329 | 38% |

| EBITDA (Rs Cr) | 6 | 9 | 13 | 23 | 34 | 54% |

| Net profit (Rs Cr) | 3 | 4 | 5 | 13 | 17 | 54% |

| OPM% | 7% | 6% | 8% | 9% | 10% | – |

On the face of it, the business looks tidy. Consolidated sales grew from Rs 90 cr in FY22 to Rs 329 cr in FY26, with net profit rising from Rs 3 cr to Rs 17 cr over the same span. The operating profit also logged a strong 54% CAGR in the last 4 years, while operating profit margins climbed to 10%.

The share price of Mahamaya was around Rs 115 when listed in November 2025 and as on 5th of June 2026 it was Rs 160.

Mahamaya Lifesciences Long Term Price Chart

The share is trading at a PE of 23x and the industry median currently is 22x. Since the stock was recently listed, a 10-year median figure would not be of any use right now.

However, the caveat sits in the cash flow. Despite reporting steady profits, the company’s cash from operations was negative Rs 30 cr in FY26, as money got locked up in inventory and receivables. Profit on paper is not the same as cash in the bank. For a small chemicals maker that needs working capital to grow, that gap is the thing to watch.

As for the future plans, the company plans to expand its formulation capacity at Dahej and add technical (technical-grade active) manufacturing capability at the same site to reduce import dependence and improve margins.

Watchlist or wait? Reading Kedia’s Fresh Picks

Step back, and the March 2026 filings show a clear posture rather than a single sector call. Kedia is betting on things India must build, from solar cells to farm inputs, and he is happy to go very small to do it.

Websol is a proven winner he is joining late, after gains of over 1,700%. While Mahamaya is the newly listed fresh pick listed in the SME board, which is now backed by the market master of India. The bet there is that the runway is still long enough to justify the price.

For an ordinary investor, the lesson is not to copy the trade. It is to copy the homework. Kedia is not someone who will pick new holdings without doing the homework. A good idea would be to add these two stocks to a watchlist and keep a close eye on them.

Disclaimer:

Note: We have relied on data from http://www.Screener.in and http://www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.