The Valuation Air Pocket: Why Growth Outpaces Price

Even as retail investors trip over themselves to buy into the blue-chip narrative, paying eye-watering multiples for the privilege, many a times the real story is unfolding somewhere else. And in such a market, big-brand healthcare has created a risky blind spot.

In a sector where 20% growth is cheered, two outliers have quietly engineered a massive 130% profit CAGR over the last five years.

Despite delivering a growth trajectory that outpaces most of frontline peers, these two stocks are currently trading at a significant discount to their all-time highs. It is a classic valuation air pocket.

In the cold language of the market, this could be a rare asymmetric trade, where the downside is cushioned by a massive discount, but the upside is fuelled by triple-digit earnings momentum.

Are these stocks poised to make the most of the next Healthcare Bull Run? Also, do they have what it takes to sustain the enviable profit growth? Let us dive into the two stocks to find out?

Entero Healthcare Solutions Ltd: 152% Profit Compounder at a 27% Valuation Air Pocket

Incorporated in 2018, Entero Healthcare Solutions Ltd is in the business of distribution and marketing of pharmaceutical and surgical products and allied services.

With a market cap of Rs 4,910 cr as on 20th March 2026, the company is a leading Healthcare Supply Chain Solutions Specialist, ranks among India’s top three healthcare product distributors by revenue, offering demand fulfilment and generation solutions to manufacturers.

Entero Healthcare offers a one-stop procurement solution with a vast product range and quick delivery. It provides healthcare manufacturers with a nationwide, compliant distribution platform, connecting them to pharmacies, hospitals, and clinics across India. Advanced distribution systems and technology platforms ensure seamless delivery from manufacturers to end-consumers

The company has reduced its debt from over Rs 600 cr 5 years ago to the current Rs 44 cr, thus reducing the pain of hefty interest payments to some extent.

The company was listed 2 years ago in February 2024, where it raised over Rs 950 cr under its IPO.

Let us look at the financials of the company and try to find out if it is worthy of your FY27 watchlist

Growth at Any Cost v/s Cash is King

The company’s sales have seen a compounded growth of 30% from Rs 1,350 cr in FY20 to Rs 5,096 cr in FY25. And in the 3 quarters between April 2025 to December 2025, the company has recorded sales of Rs 4,682 cr.

The EBITDA (earnings before interest, taxes, depreciation, and amortization) was a Rs 23 cr in FY20 which grew to Rs 172 cr in FY25, logging a compound growth of an impressive 50%. And for the 3 quarters of FY26 ending in December 2025, EBITDA of Rs 180 cr has been logged already.

As for the net profits, the company recorded a compound jump of a huge 152% from Rs 1 cr in FY20 to Rs 107 cr in FY25. And for the 3 quarters of FY26 ending in December 2025, the company has recorded profits of Rs 101 cr.

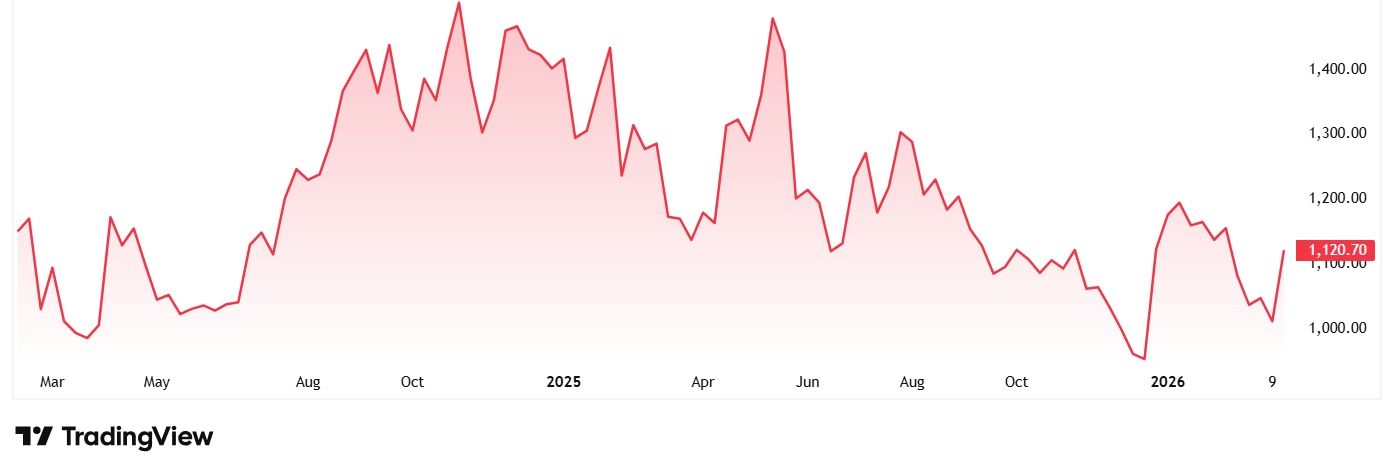

The share price of Entero Healthcare Solutions Ltd was around Rs 1,150 when listed in February 2024 and as on 20th March 2026 it was Rs 1,128.

At the current price, the share is trading at a discount of 28% from its all-time high of Rs 1,584.

One reason could be the markets shift for growth at any cost to cash is king. Investors are no longer willing to overlook persistent negative operating cash flow and a roll-up acquisition strategy that has begun to falter. Add to that the hit the company has taken due to the new unified labour laws.

The company’s share is trading at a current PE of 42x while the industry median when compared to peers is 44x. And for a company trading at a significant premium to many peers, the structural frictions listed above have turned a compelling growth story into a cautionary tale of valuation indigestion.

Entero is a high-speed engine currently trapped in a low-gear valuation. The debt reduction proves management’s focus on balance sheet repair. But until Entero can resolve its cash flow friction and labour law headwinds, this deep discount remains a high-stakes test of operational grit. The big question is that is the top-line momentum irrelevant if the business model continues to consume more capital than it generates?

Medplus Health Services Ltd: India’s Second-Largest Pharmacy at a 30% Valuation Steeple

Incorporated in 2021, MedPlus is the 2nd largest pharmacy retailer in India, with 4,930 stores across 13 states and 1 union territory, serving 750 cities.

With a market cap of Rs 9,892 cr as on 20th March 2026, the company’s offerings include medicines, vitamins, medical devices, and test kits, personal and home care items, toiletries, baby care, soaps, detergents, and sanitizers.

MedPlus also offers over 1,450+ private label products across pharma and FMCG categories, aiming to increase their contribution in high-margin segments. The company is also known for its targeted pricing strategy, offering high discounts (up to 80%) on chronic therapy products to cater to price-sensitive, high-value customers, while balancing discounts on acute therapy to maintain profitability.

Looking at the financials, the company’s sales have logged a compounded growth of 16% from Rs 2,871 cr in FY20 to Rs 6,136 cr in FY25. And in the 3 quarters between April 2025 to December 2025, the company has recorded sales of Rs 5,028 cr already.

The EBITDA grew from Rs 134 cr in FY20 to Rs 488 cr in FY25, logging a compound growth of 25%. And for the 3 quarters of FY26 ending in December 2025, EBITDA of Rs 439 cr has been logged.

Regarding net profits, the company has recorded an impressive compound growth of 131% from Rs 2 cr in FY20 to Rs 150 cr in FY26. And for the 3 quarters of FY26 ending in December 2026, the profits logged are 156 cr already, hinting at a stronger finish to FY26.

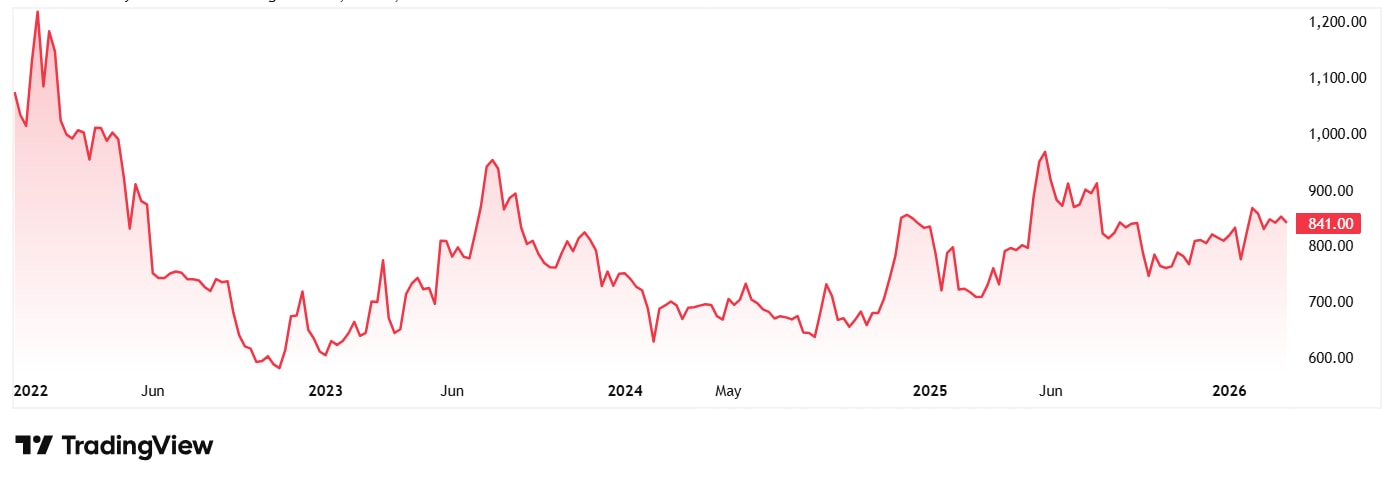

The share price of Medplus Health Services Ltd was around Rs 1,076 when it was listed in December 2021 and as on 20th March 2026 it was Rs 824.

The Price of Aggressive Expansion

At the current price, the stock is trading at a discount of 37% from its all-time high of Rs 1,343.

MedPlus Health is discovering that in a maturing market, store-count is a vanity metric while compliance is sanity. Thanks to a wave of regulatory suspensions the company’s aggressive expansion bleeding free cash flow, the market is no longer buying the growth story without a side of governance.

Having said that, MedPlus is a study in precarious scaling. While a 131% profit CAGR suggests a retail steamroller in the making, the 60% promoter pledge acts as a heavy anchor on investor sentiment. It is one thing to win the pharmacy wars on the high street, but quite another to survive the cold scrutiny of a sceptical market.

For now, the valuation steeple remains a slippery climb, and the market’s demand for governance could outweigh its hunger for growth.

Prescriptions for a Sceptical Market

Both Entero Healthcare and Medplus Health have posted solid profit growth of over 130% in the last 5 years, a feat most CEOs would give their right arm for. But in the market, the mood is far from celebratory. Investors have knocked nearly 30% off their peak prices, posing a tough question: is this a bargain or a warning sign? Also, while the profit figures are verified, triple-digit CAGR often originates from a low base in early years of operation.

The analysis for both firms is a mix of solid financials with worrying signs. Entero has slashed its debt and dominated the supply chain, but it is learning that growth doesn’t count for much if you can’t turn it into cold, hard cash. Meanwhile, Medplus has built a pharmacy empire, yet it is currently haunted by regulatory red tape and a massive 60% promoter pledge that makes big investors nervous.

So, should one trust the triple-digit profit growth and buy the dip, or listen to a market that seems to value safety over speed? If these companies can fix their internal leaks, specifically their cash flow and governance, today’s discount might look like the steal of the decade. But it is all speculation as of now.

Hence, it will be a wise decision to add these stocks to a watchlist and keep an eye on them if you don’t want to miss out on any big movements.

Disclaimer:

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.