For decades, India’s auto component industry followed a simple playbook: Win orders. Add capacity. Ship parts. Repeat.

When global demand for vehicles increased, suppliers prospered. When the cycle turned, earnings came under pressure. The business remained tied to the growth of a single industry. But a subtle shift is underway.

Some auto component manufacturers are quietly moving beyond their legacy business. Instead of relying solely on cars and commercial vehicles, they are using the same engineering capabilities to enter industries such as aerospace, defence, industrial automation, and energy. The result is that businesses are now less dependent on auto cycles, enjoy higher margins, and command better valuations.

Among the listed players, three companies stand out for how they are approaching this transition. NRB Bearings, Sansera Engineering, and Craftsman Automation. Each has a strong automotive business that continues to generate cash, but each is deploying that capital differently to build its next growth engine. The market has started taking notice of this shift.

Why These Three Companies?

Not every auto component company making diversification deserves attention. NRB Bearings, Sansera Engineering and Craftsman Automation are different as their diversification strategies are already visible on the ground. All three are building businesses outside their legacy automotive operations, through acquisitions or growing order books or expanding business segments.

Another common factor is institutional confidence. Despite operating in a cyclical sector, all three companies have attracted significant ownership from domestic and foreign institutional investors, suggesting the diversification story is finding support well beyond retail investors.

NRB Bearings: Buying Its Way Into Aerospace

NRB Bearings is India’s largest independent bearing manufacturer with over six decades of engineering legacy. More than 90% of the vehicles running on Indian roads have bearings made by NRB.

In January 2026, NRB took the first step to diversify beyond serving the auto industry. It acquired Bengaluru-based Mahant Tool Room for ₹27.5 crores. Although the acquisition didn’t make any headlines, it silently positioned NRB in the aerospace component manufacturing industry.

Mahant Tool Room produces high-precision, mission-critical components for aircraft engines and fuel systems for Hindustan Aeronautics Limited. It came with an existing order book of over ₹25 crores, which doubled to ₹50 crores within months of acquisition.

The Aerospace Qualification Shortcut

Building an aerospace business from scratch is a long process. Components used in aerospace engines require stringent product approvals and certifications. At times, the timelines for getting these approvals can stretch years. By acquiring Mahant, NRB effectively bypassed the lengthy three-to-four-year qualification cycle and entered the industry with an established manufacturing capability, customer relationships, and approved products.

Alongside, NRB also entered into a joint venture with Italy’s Unitec Group to manufacture industrial bearings, creating another non-automotive revenue vertical.

Financials: Where NRB Stands

NRB Bearings: Financial Performance

| Metrics | FY24 | FY25 | FY26 |

| Sales (₹ crores) | 1,094 | 1,199 | 1,335 |

| Operating Profit (₹ crores) | 176 | 199 | 232 |

| Operating Margin (%) | 16.1% | 16.6% | 17.4% |

| Net Profit (₹ crores) | 242* | 82 | 146 |

In FY26, NRB reported an 11.4% year-on-year increase in revenue, and operating margin expanded by 80 basis points from 16.6% in FY25 to 17.4% in FY26.

The management has set a target of reaching ₹2,500 crores in revenue by FY31, while maintaining a target range of operating margin between 18 to 20%. The aerospace business could command margins as high as 30%.

Regarding expansion in the aerospace segment, Mahant is in the process of obtaining AS9100 certification. NRB’s own engineered products will be included under this certification to expedite their market entry. NRB aims to use this platform to respond to roughly ₹100 crores of RFQs (Request for Quotation) from top global aircraft producers who require suppliers with credible certification plans.

Sansera Engineering: The Proof That Diversification Can Scale

If NRB represents the beginning of the journey, Sansera Engineering demonstrates what the next stage looks like.

Sansera Engineering is a precision engineering company that manufactures complex, high-precision components for the automotive and non-automotive sectors, supplying customers across passenger vehicles, commercial vehicles, aerospace and industrial applications.

The company has spent years building relationships with customers around the world. Today it is a tier-1 supplier to Boeing and a tier-2 supplier to Airbus.

Financials: How Sansera is Doing

Sansera Engineering: Financial Performance

| Metrics | FY24 | FY25 | FY26 |

| Sales (₹ crores) | 2,548 | 2,719 | 3,098 |

| Operating Profit (₹ crores) | 450 | 473 | 566 |

| Operating Margin (%) | 17.7% | 17.4% | 18.3% |

| Net Profit (₹ crores) | 190 | 206 | 298 |

Sansera’s financial results already reflect its transformation. The company reported a 14% increase in revenue to ₹3,098 crore and its operating margin expanded by 90 basis points to 18.3% in FY26.

But the biggest change was in its non-auto business. The Aerospace, Defence and Semiconductor (ADS) segment was the fastest-growing segment of the business, posting a year-on-year growth of 155% to ₹315 crore in FY26.

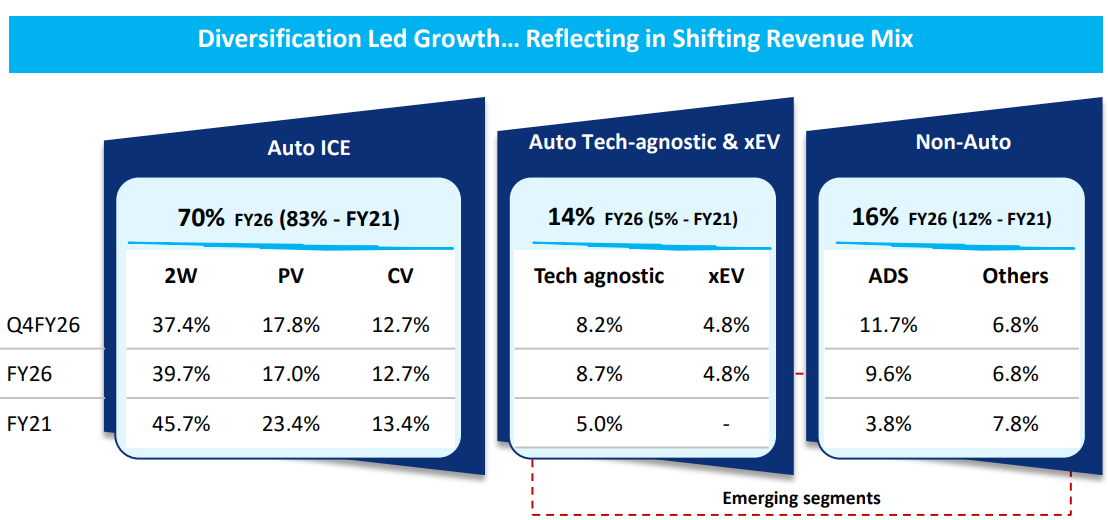

Decoupling from the ICE Engine Ecosystem

Sansera is gradually moving away from the traditional internal combustion engine (ICE) auto market. Auto ICE contributed 70% of revenue in FY26, and management intends to reduce this to ~60% over time by increasing its presence in auto tech-agnostic, EV, and non-auto businesses. Management expects the ADS business to generate revenue of ₹550-600 crores in FY27.

Sansera Engineering: Diversifying Revenue Pool

Management believes that it can execute orders worth ₹8,000-8,200 crores by the end of the decade, with an eventual goal to reach ₹10,000 crore.

Supporting this growth is Sansera’s long-term “20-20-20” strategy: achieving 20% EBITDA margin, 20% annual revenue growth, and 20% return on capital employed (ROCE).

Craftsman Automation: Betting on India’s Industrial Capex Boom

Rather than aerospace, Craftsman is betting on India’s manufacturing and industrial capex cycle.

Craftsman Automation was founded in 1986 in Coimbatore, Tamil Nadu, and produces precision components and provides contract manufacturing services to the automotive and industrial engineering industries.

Craftsman Automation: Financial Performance

| Metrics | FY24 | FY25 | FY26 |

| Sales (₹ crores) | 4,452 | 5,690 | 8,069 |

| Operating Profit (₹ crores) | 879 | 833 | 1238 |

| Operating Margin (%) | 19.7% | 14.6% | 15.3% |

| Net Profit (₹ crores) | 337 | 201 | 384 |

Consolidated revenues grew 42% YoY to ₹8,069 crores in FY26 and profit after tax almost doubled to ₹384 crores against the previous year. Operating margins have declined in the past 3 years, but there is a slight improvement in FY26.

Management sees the next phase of growth from industrial engineering, stationary engines and aluminium products even though the automotive business is still the biggest contributor.

The biggest opportunity lies in the stationary engines business, driven by the fast expansion of AI-led data centres. “There is a growing demand for large backup power systems, and we expect to generate almost $100 million in revenue by FY29-30.”

The aluminium business is expected to be an even bigger growth driver. Management aims to build it into a $1 billion business within the next two to three years, with revenue growing at 20-25% annually, much faster than its traditional powertrain business.

Alongside growth, the company is also strengthening its balance sheet. It aims to reduce its net debt-to-EBITDA ratio to below 2x during FY27 from 2.4x in FY26, while ensuring all new projects generate a minimum 20% pre-tax ROCE.

Smart Money is Following the Transition

All three companies have meaningful ownership from domestic and foreign institutional investors.

Institutional Shareholding (in %)

| Company | FII | DII |

| NRB Bearings | 14.7 | 10.0 |

| Sansera Engineering | 18.8 | 35.4 |

| Craftsman Automation | 17.1 | 31.0 |

Institutional ownership alone is never an investment thesis. But when companies begin investing beyond their legacy businesses, the presence of long-term institutional investors often provides an additional layer of confidence that the strategy is backed by rigorous due diligence.

Valuation: Is the Market Already Pricing in the Pivot?

The market has already started assigning higher valuations to companies that have demonstrated meaningful progress beyond their legacy automotive businesses.

Valuation Signals Investor Confidence

| Company | P/E | 5-yr Median PE | Industry PE |

| NRB Bearings | 28.8 | 20.1 | 30.0 |

| Sansera Engineering | 66.1 | 33.1 | 30.0 |

| Craftsman Automation | 63.1 | 37.1 | 30.0 |

Sansera Engineering commands the highest valuation at 66 times earnings, almost double both its five-year median and the industry’s average. Investors appear to be rewarding the company for building a sizeable Aerospace, Defence and Semiconductor (ADS) business

Craftsman Automation is trading at 63 times earnings, well above its historical 5-year median PE of 37 times. The premium reflects the optimism around its emerging businesses.

NRB Bearings, in contrast, shows quite a different picture. It trades at 29 times earnings, close to the industry’s average, but above its own five-year median of 20. Unlike the other two companies, its aerospace business is still at an early stage, and the market appears to be waiting for stronger execution before assigning a higher valuation.

The Road Ahead

For all three companies, the real test isn’t revenue growth. It’s whether these new businesses can meaningfully improve profitability margins.

NRB Bearings, Sansera Engineering and Craftsman Automation are all using their legacy automotive businesses to enter sectors with better profitability and longer growth runways. The market has already started rewarding this transition through higher valuations.

However, the biggest risk remains execution. Aerospace and defence businesses involve long qualification cycles, and any delay in approvals or new orders could slow growth.

Another challenge is scale. These newer businesses still contribute a small share of revenue, so it will take time before they can meaningfully improve overall margins.

Lastly, the core automotive business continues to fund these investments. A slowdown in vehicle demand could affect both cash flows and the pace of expansion. As the companies reinvent themselves, add these stocks to your watchlist and monitor how they execute on their long-term growth plans.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Deepan Datta has spent over a decade studying stocks and mutual funds. His passion is to uncover interesting stories in the financial markets and share them through his writings with investors at large. He is focused on delivering clear, easy to understand and research-backed insights. Deepan began his career as a Research Associate at S&P Global, where he developed a strong foundation in financial research and data analysis.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.