Welcome to the latest edition of Dividend Hunter. Over the past few weeks, we have analyzed companies where strong cash flows could translate into consistent dividends going forward. In our previous edition, we covered a Bluechip PSU offering a 5.4% yield.

In this edition of Dividend Hunter, we analyze a private-sector technology company that is a major enabler of the modernization of the global airline economy. This company has consistently generated strong operating cash flows and has just paid a dividend yielding 8%.

As airline operations scale, the complexity of managing global ticket sales and settlements is rising. Evolving industry standards, such as the International Air Transport Association’s (IATA) One Order initiatives, are driving a fundamental upgrade in how airlines manage their commercial networks.

Accelya: A Key Enabler of Airline Tech

One established market player in this specific niche is Accelya Solutions India Limited. It ensures that this digital infrastructure is seamlessly deployed.

Why the Airline Transition Drives Technology Deployment

To meet this demand and fulfill modern retailing goals, airlines are moving away from legacy ticketing systems. While airlines focus on core operations such as expanding routes and managing fleets, they cannot operate effectively without mission-critical financial software.

Operational Profile: The Machinery for Airline Finance

Accelya provides specialized software and a service platform exclusively for the airline and travel industry. It provides cost-effective, pay-as-you-use platforms to global airlines to support their day-to-day operations.

It doesn’t just sell software. It serves as an accountable partner for complex processes, including revenue accounting, cost management, and audit services.

This ensures that global carriers avoid financial bottlenecks across their revenue streams. This operational strength translates into stable financial growth. Of course, this is driven by the airline industry’s ongoing need for digital modernization.

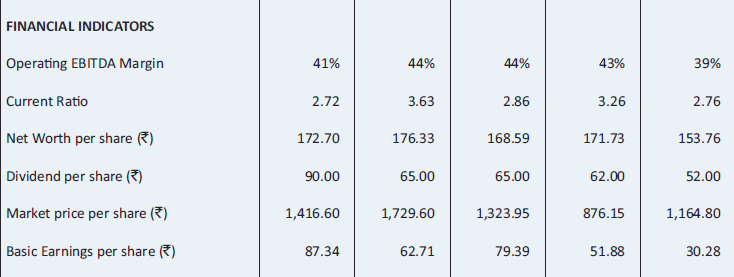

It generates steady profitability. It boasts a 41% operating EBITDA margin while maintaining a clean balance sheet with zero borrowings. On top of that, Accelya prioritizes returning capital to shareholders.

It has a historical track record of consistent dividend payments and recently increased its payout. For instance, for the financial year ended 30 June 2025, Accelya paid a total dividend of ₹90.00 per equity share, up from ₹65.00 in the previous year.

But Accelya is now investing heavily to scale its platforms into new domains, like the cloud-native (FLX ONE) architecture and modern AI-driven retailing standards.

So, the moot question is, will these cash flows and dividend payments remain sustainable in the long run? We will find out in this story.

Inside Accelya’s Airline Financial Ecosystem

Accelya provides several specific solutions designed to manage the financial lifecycle of airline ticketing and operations. This includes revenue accounting, revenue assurance, cost management, order accounting, and Accelya Managed Services.

In revenue accounting, Accelya provides platforms to ensure accurate and timely revenue declarations. Revenue assurance provides audit services that span the entire airline ticket lifecycle, from the original passenger booking to the completion of the journey.

Under cost management, it automates the payables process for airlines. Beyond providing software, Accelya delivers processing services that adhere to stringent Service Level Agreements and consistently meet both internal and external airline audit requirements.

Accelya Bets on IATA’s ‘One Order’ Shift

Now, adapting to new industry standards, it is actively transitioning airlines to the IATA “One Order” initiatives. This platform handles essential financial functions for modern retailing, including Order-to-Cash, Procure-to-Pay, Settlement, Accounting, and Reconciliation.

Accelya operates on a structured commercial model, maintaining long-term client relationships and predictable cash flows. The model is built on three main pillars: Pay-as-you-use Model, Single Vendor Accountability, and Neutral Service Provider.

Why Accelya’s Pay-Per-Use Model Stands Out

Under the Pay-as-you-use Model, Accelya offers its software and solutions on a variable, pay-per-use basis. This approach allows airlines to keep capex low by shifting to variable costs. For Accelya, this model creates recurring revenue streams and stable cash generation.

Dissecting the Predictable Revenue Mix

In the revenue mix, Business Process Outsourcing accounts for 58% of the revenue. This reflects the Single Vendor Accountability pillar. Software Hosting and Support contributes another 26%. This segment strongly aligns with their Pay-as-you-use. The balance (16%) comes from the software license.

Strong Margins and Cash Flows Support Accelya’s Business Model

The company’s market cap is ₹1,675 crore, as of 21st May 2026.

Accelya Share Price

Over the last three years, Accelya’s net profit grew at a 19% CAGR, reaching ₹130 crore in FY25. Operating revenue in FY25 rose by 11% year-on-year to ₹501 crore. Its asset-light model and operating leverage helped maintain strong profitability. As we said, Accelya’s financial year ends on 30 June.

Unpacking the 39% Profit Surge (And the Low-Base Reality)

The company’s operating EBITDA (Earnings Before Interest, Tax, Depreciation and Amortisation) increased by 2% to ₹205 crore, maintaining a comfortable operating margin of 41%.

This steady operational performance translated well into the bottom line, with net profit growing by 39% to ₹130 crore. However, most of the profit growth came from a low base due to a one-time exceptional loss in FY24. Otherwise, the net profit was flat.

Further, in 9MFY26, revenue rose by 2% to ₹405 crore. However, operating profit grew by 11% to ₹127 crore, while margins fell 460 bps to 31.4%. Net profit fell by 31% to 65 crore.

Capital Efficiency at Scale

The company generates a robust return on equity (ROE), underscoring its efficient capital allocation. Accelya reported an ROE of 50% for the financial year ended 30 June 2025 (FY25), up from the 36% recorded in the previous year. The ROCE stood at 55% for FY25, compared to 46% in the previous year.

The sustainability of Accelya’s dividend depends on cash generation. Accelya’s business serves as a reliable cash engine.

The Cash Conversion Engine Sustaining the 8% Yield

For FY25 ending 30 June, it generated net cash from operating activities of ₹145 crore. This results in strong cash conversion and predictable liquidity. The pay-as-you-use model, which provides annuity-style revenue streams, supports this visibility.

Accelya’s balance sheet has zero bank borrowings. As a result, the company’s financing activities are entirely free of interest payments to banks, allowing management to direct capital toward shareholder returns. In FY25, the net cash used in financial activities was ₹146 crore.

This outflow was used only for repayment of lease liabilities (₹12 crore). The majority of the cash flow (₹134 crore) was paid directly to equity shareholders as dividends. This was a notable increase from ₹82 crore paid in FY24.

Assessing the Long-Term Sustainability of the 8% Dividend

Over the last 5 financial years, it has not only maintained its payouts but has consistently increased its dividend per share year-on-year.

The company has consistently scaled its shareholder returns over the last five years. The payout began at ₹52.0 per share in FY21, climbing to ₹62.0 in FY22 and ₹65.0 in FY23. This momentum was sustained at ₹65.0 in FY24, before reaching a high of ₹90.0 in FY25.

At the current share price of ₹1,116, FY25 payout translates into a dividend yield of 8.0%. Also, for FY26, the company has already declared an interim dividend of ₹45 per share. If past track record is to be believed, it may also declare a final dividend at the end of its financial year on 30 June.

This is consistent with its dividend policy of paying one interim dividend and one final dividend every year. This supports the possibility of continued dividend payouts, subject to business conditions.

Key Financial Metrics

The company’s general approach is to declare an interim dividend at least once a year and to recommend a final dividend. But this is contingent on several internal and external financial parameters.

This includes working capital needs, investing to support future growth, and also maintaining free cash to manage unforeseen situations. Thus, if the company incurs losses or profits are deemed inadequate, it prefers to manage its reserves judiciously.

In such cases, it may either choose not to declare a dividend or declare one that is lower than its normal rate. Even if the Board proposes not to distribute profits for a given period, it must disclose the reasons.

Will Ongoing Investments Derail the Dividend?

For a dividend investor, the primary concern is whether management will cut the dividend to fund these new technological developments. However, based on the current financial structure, these investments are unlikely to derail the dividend.

Because Accelya is a software provider, its capital requirements are relatively low. In FY25, the company spent just ₹3.7 crore on product development, which is small compared with its cash flow and net profit.

The company generates more than enough organic cash to fund its Artificial Intelligence and platform upgrades while still maintaining its high dividend yield. But, there are several external and operational risks that could impact the company’s future cash flows and, by extension, its dividend sustainability.

The Hidden Risks in Accelya’s Business Model

Accelya’s core risks include macroeconomic downturns triggering airline bankruptcies, which directly reduce revenue. The company has several pending income tax disputes and a service tax demand.

Other risks include high customer concentration. Just one single customer accounted for over 10% of the company’s revenue in FY25. This poses a big risk to the company’s revenue if the customer ends its relationship.

Another risk is the company’s dependence on related-party transactions within the broader Accelya Group.

For the year ended 30 June 2025, Accelya generated nearly half of its total operating revenue from services rendered to related parties, primarily fellow subsidiaries like Accelya World S.L.U. and Accelya Middle East FZE.

Valuation Arbitrage: Is Accelya Trading at a Steep Discount?

Valuation-wise, Accelya trades at a price-to-equity (P/E) multiple of 16x, which is at a discount to its 5-year historical median (20x). The valuation is also at a discount to the industry P/E (20x) but is almost in line with peers, such as Saksoft (14x) and Ceinsys (14x).

The “Dividend Hunter” Verdict: Is This a Long-Term Income Fortress?

Accelya meets the key Dividend Hunter filters. It has shown profit growth, strong cash flows, and a payout ratio within thresholds.

Given a yield of 8%, consistent increases in cash flow, a dividend distribution policy, and a historical dividend payout track record, it appears likely that the dividend payout trend could continue and increase.

Nonetheless, dividend hunters should add this stock to their watchlist and see if it sustains its dividend yield.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data were unavailable have we used an alternative, widely accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.