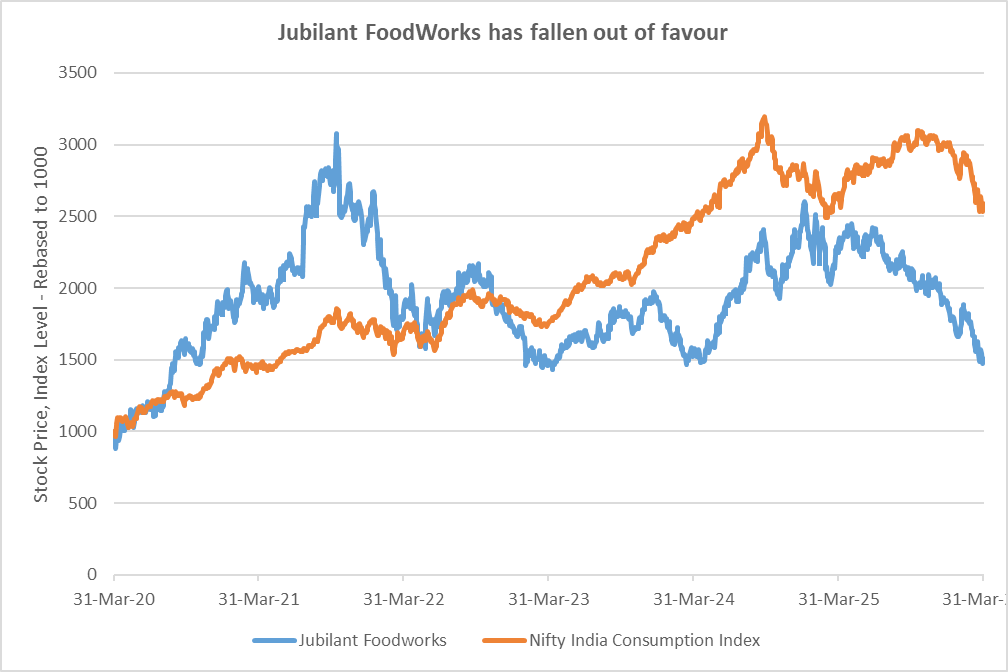

Jubilant FoodWorks, one of India’s larger Quick Service Restaurant (QSR) companies, recently made headlines for its decision to exit its 15-year long Dunkin’ Donuts franchise in India. Markets appear to be treating the move as incremental at best – the stock has gained 1.8% since 30 March, against Nifty 50 index’s 1.7% appreciation. After all, Dunkin’ contributed only a small share to revenues and remained loss-making for years.

But timing matters. The decision comes at a point when Jubilant’s stock has corrected nearly 40% off its early-2025 peak, and sentiment around discretionary consumption has clearly softened. More importantly, profitability pressures from aggressive store expansion, rising input costs, and intensifying competition have started to show up consistently in quarterly numbers.

The question, therefore, is not whether Dunkin’s exit moves the earnings needle immediately. It clearly doesn’t. The real question is whether this marks the beginning of a broader strategic tightening at Jubilant FoodWorks – exactly what the doctor ordered after a difficult year for the stock.

Details of the Dunkin’ exit

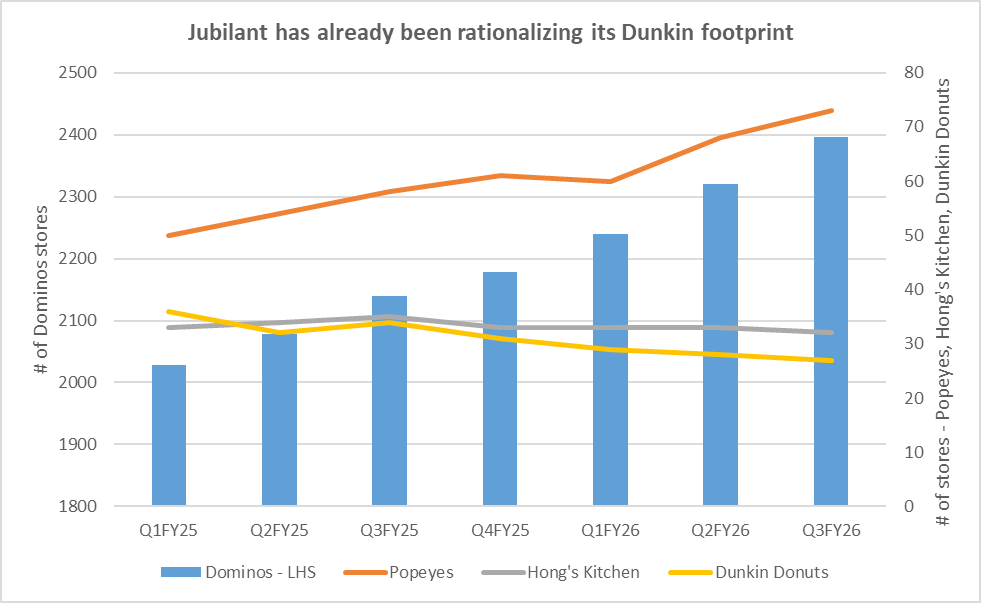

The Multiple Unit Development Franchise Agreement (MUDFA) between Jubilant FoodWorks and Dunkin’ Donuts is set to expire on 31 December 2026, and will not be renewed. To be sure, while the footprints for its pizza-franchise (Dominos) and fried-chicken chain (Popeyes) have expanded consistently, Jubilant has been rationalizing Dunkin’ stores since FY25. Down from a peak of 32 stores in June 2024, Dunkin’ sports only 27 stores in India as of December 2025.

The official decision to not renew the franchise could likely result in further store-closures, sale or transfer of assets, or reassignment of franchise rights, depending on discussions with the owners of the Dunkin’ brand.

The Dunkin’ drag

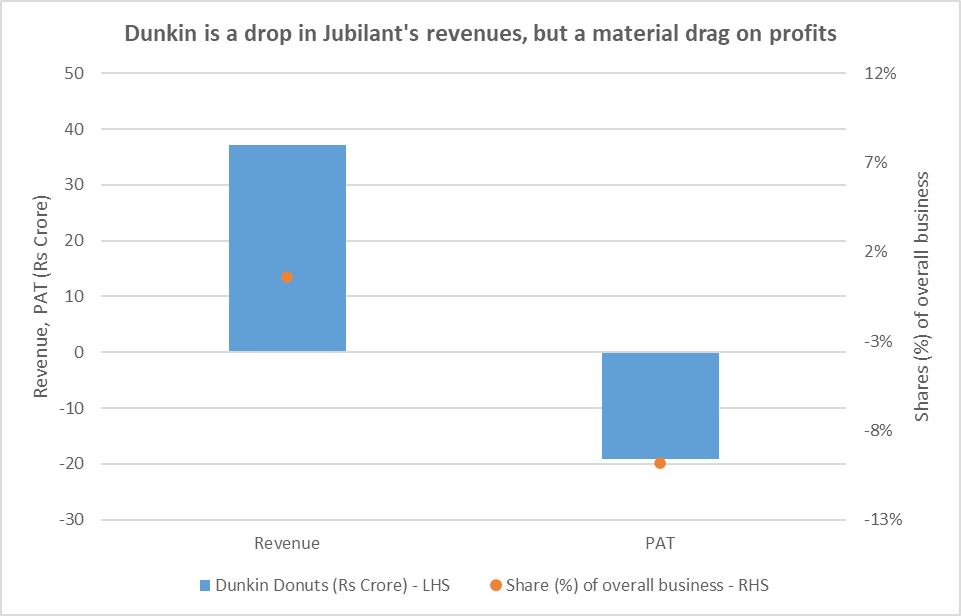

As for what it would mean for Jubilant, at just Rs 37 crore, Dunkin’s revenues make up a meagre 0.6% of its topline. But when it comes to profits, the drag has been material. Jubilant’s profit in FY25 would have been Rs 213 crore instead of Rs 194 crore, had it not been for Dunkin’s stubborn losses.

More importantly, there has been no clear path to profitability. Reports suggest that donuts have failed to carve a space for themselves despite India’s growing fast-food culture. That donuts and coffee do not belong in India’s preference for hot and savoury breakfasts, and the pricey dessert does not fit well into India’s price-conscious mass-consumption landscape either.

In contrast, Dominos has scaled up successfully on the back of mass appeal for its brand, as well as a well-established supply-chain. Jubilant runs almost 2,400 Dominos stores in India and has recently extended the franchise by 15 years with an option for further extension by 10 years. Once the Dunkin’ drag is shed, the consequently higher strategic focus on the more promising Dominos brand could be exactly what the business needs amid recent struggles.

What Mad Over Donuts did differently

Despite experimentation with smaller stores and savoury snacks, Dunkin’s 27-store footprint remains but a faint shadow of its initial lofty goal of 500 stores in India. On the other hand, Mad Over Donuts (MOD) has found better traction with reports claiming over 150 stores, and better profitability as well.

MOD’s relative success in India, compared to Dunkin’, has less to do with category demand and more to do with positioning discipline. Unlike Dunkin’, which entered India as a hybrid cafe competing simultaneously with burger chains, coffee chains, and dessert formats, MOD stayed tightly focused on the indulgence-led dessert occasion.

Meanwhile, Dunkin’ was forced into repeated menu pivots toward sandwiches and burgers that diluted brand identity without fixing profitability. That said, donuts remain a niche category even today, and the recent shift in consumer behaviour away from sugary snacks is likely to bear down on both brands.

Shareholding stress?

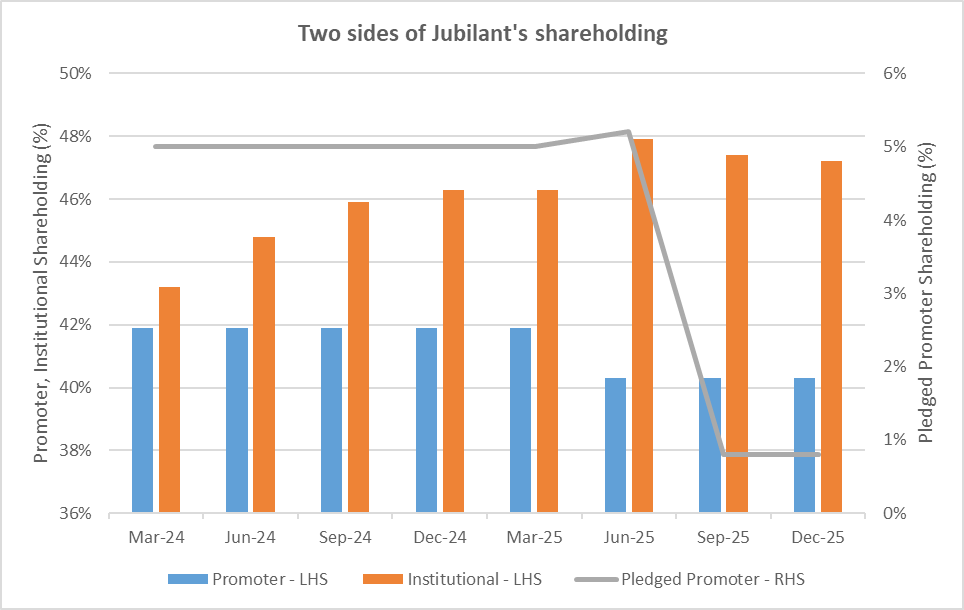

The Bhartia family, promoters of the Jubilant group, had sold 1.6% stake in Jubilant FoodWorks in June via block deals. This had created a liquidity overhang, which triggered a sharp selloff in the stock. But the point to note is that the stake-sale does not reflect the promoters’ confidence (or lack of it) on Jubilant FoodWorks. The stake-sale spanned the entire Jubilant group, and helped raise over Rs 1,800 crore for the acquisition of Coca Cola’s bottling arm.

Moreover, the pledged portion of promoters’ shares has fallen from over 5% to less than 1% last year. This reduces the risk of a vicious cycle causing further stress amid the stock’s correction. At the same time, rising institutional shareholding is a vote of confidence for the business. That said, a liquidity overhang would not have sparked an extended correction if things had been picture perfect on the ground.

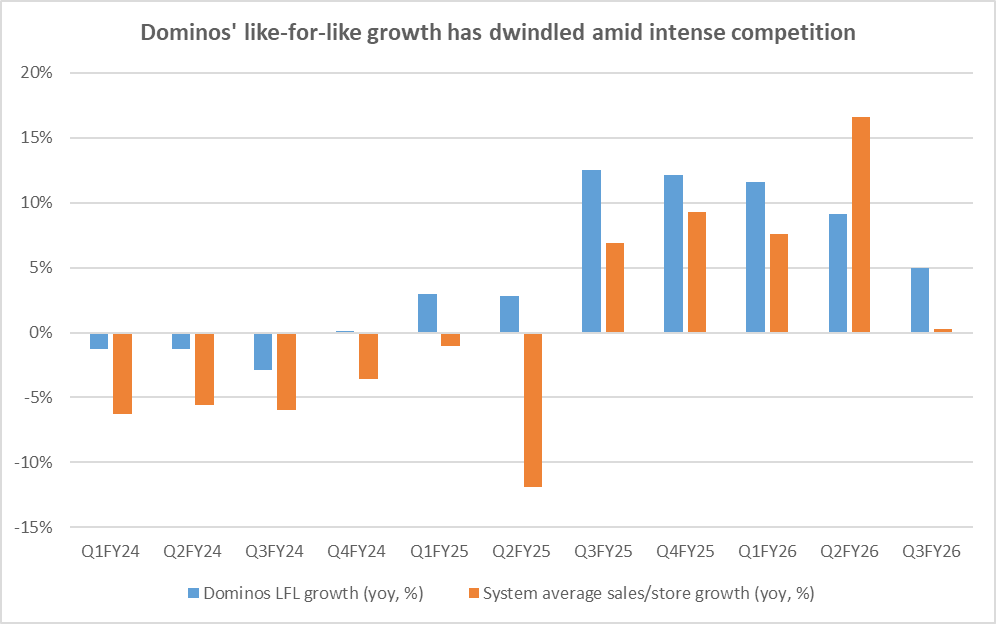

Overheated domestic market

Back home, expansion has been aggressive. Popeyes stores, particularly, have seen double-digit growth with a target of 250 stores and Rs 1,000 crore in revenue over the medium term. But despite menu innovation and calibrated pricing, like-for-like (LFL) growth has fallen to the mid-single-digits amid intense competition in India’s QSR space. The December 2025 quarter saw 11.8% year-on-year growth in revenue to Rs 1,800 crore with LFL growth at just 5%.

Meanwhile, store additions, elevated food inflation, and rising employee and rental costs have weighed on margins. Gross margin came in at 74.9% during Q3FY26, a 16-bps contraction over the year-ago period. Importantly, the company has been reluctant to fully pass on cost pressures to consumers amid a slowdown in discretionary demand – a prudent strategic move that has helped the business grow faster than the industry and gain ground over competitors, but one that has kept earnings growth subdued in the near term.

The new labour code is also expected to shave 10-15 bps off domestic margins over the near to medium-term. But over the longer term, the turnaround in India’s QSR space should help Jubilant. Moreover, as its stores mature, higher store productivity and operating leverage should get margins back on track – management’s guidance stands reaffirmed at 200 bps over FY24 margins.

International angle

Internationally, its DP Eurasia operations, spanning Turkey, Azerbaijan and Georgia, has been a source of concern due to currency volatility and acquisition-related leverage. But management commentary suggests that the business is on track to gradually service its debt through internal cash flows, even as inflationary pressures in Turkey have begun to stabilise. Consolidated financing costs have already seen a 59% year-on-year decline on refinancing of DP Eurasia debt from Turkish Lira to Euro.

Improving revenue and store-level economics raise hopes of a recovery – DP Eurasia clocked 15% year-on-year growth in revenue to Rs 580 crore in the December 2025 quarter, with PAT margin delivery at a healthy 6.2%. Still, LFL growth trends remain uneven, and macro risks in the region cannot be ignored.

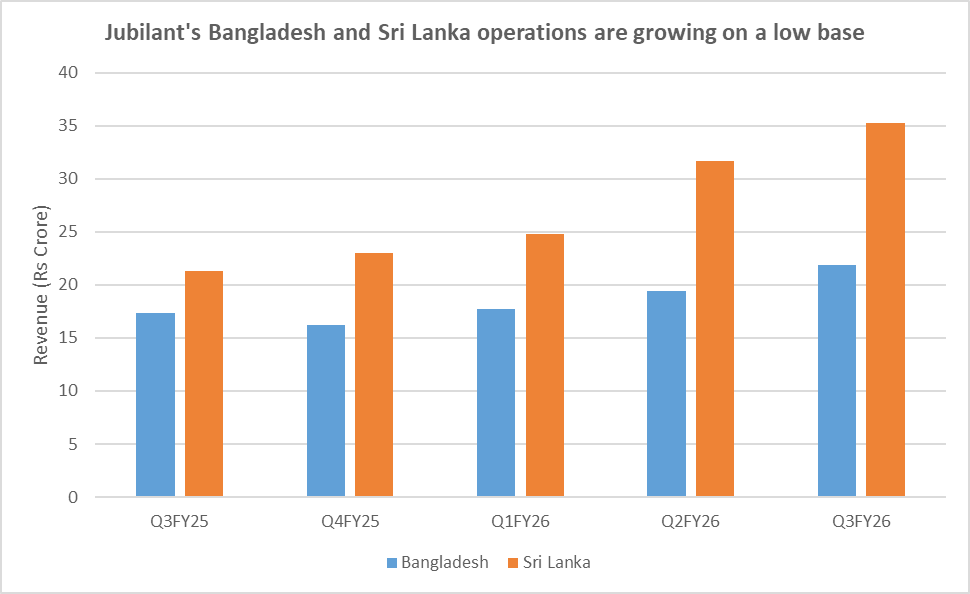

Smaller markets such as Sri Lanka and Bangladesh are showing strong growth on a low base, providing incremental diversification to the revenue mix. But international operations are still unlikely to be the primary driver of near-term earnings upgrades, even as they are slowly transitioning from being a drag on sentiment to a modest supporting pillar.

Summing it up

Jubilant’s management expects 15-16% sales CAGR growth on the back of 1,000 new stores and 5-7% LFL growth over the medium-term. Against this context, shutting the structurally weaker Dunkin’ business signals a sharper capital allocation discipline at a time when investors are looking for evidence that management is willing to prioritise returns over expansion optics.

At a valuation of 89x P/E, the stock is now trading at a significant discount to its median 132x P/E. But considering that the industry P/E is 63x, a rerating for Jubilant will be contingent on tangible improvement on the ground.

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Disclaimer:

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ananya Roy is the founder of Credibull Capital, a SEBI-registered investment adviser. An alumnus of NIT, IIM, and a CFA charter-holder, she pens her views on the economy and stock markets.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article. Clients of Credibull Capital may or may not own these securities.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.