In the vast and often noisy world of equity markets, some investors act like quiet north stars. They do not shout. They do not chase every passing trend. Yet, their portfolios offer direction. They help others navigate uncertainty with a sense of calm and clarity. Over time, patterns emerge from their choices. And those patterns often reveal where the next opportunities may lie.

The Ashish Kacholia Strategy: Scouting Industrial Quiet Stars

One such investor is Ashish Kacholia. Known for his sharp eye in the mid- and small-cap space, he has built a reputation for identifying businesses early in their growth journey. His portfolio is not driven by headlines or crowded themes. Instead, it reflects a preference for companies that are quietly building scale. Many of his bets have gone on to deliver strong returns over time, reinforcing his image as a disciplined and forward-looking investor.

In this article, instead of focusing on the most well-known or widely discussed stocks from his portfolio, the focus shifts to a different pattern. The idea is not to identify the biggest holdings, but to understand what connects some of the lesser-known ones.

A closer look suggests a clear tilt towards manufacturing-linked niches. These are not broad sector plays. They are specialised segments within the larger industrial ecosystem where businesses operate in a focused and often underpenetrated space.

The selection of stocks in this article is therefore built around this idea of micro-niche dominance. The focus is on companies that operate in narrow but scalable segments within the broader industrial ecosystem. These businesses are not chosen at random. Each one has a clearly defined role in its respective value chain.

#1 Aeroflex Industries: Cooling the Global AI Infrastructure

Incorporated in 1993, Aeroflex Industries, manufactures and supplies environment-friendly metallic flexible flow solution products.

As of 31st March 2026 Ashish Kacholia held 2.3% stake of Aeroflex Industries which is worth Rs 93.6 crore.

Aeroflex Industries reported a steady performance in the December quarter, supported by strong export demand and a continued shift towards value-added products. The company posted a revenue of Rs 121 crore in Q3FY26, marking a 21% year-on-year (YoY) growth. Net profit stood at Rs 16.5 crore, up 8% YoY. Margins remained healthy, with earnings before interest, tax, depreciation, and amortisation (EBITDA) margin at around 23.5%, reflecting improved product mix and operating leverage.

The growth was led by higher contribution from specialised products such as assemblies, fittings and bellows, which now account for more than half of total sales. The company continues to move away from commoditised offerings and deepen its presence in niche segments within industrial flow control. This shift is critical, as these products offer better margins, stronger customer stickiness and repeat demand across cycles.

Data Center Pivot: The 15,000-Unit Annual Scaling Goal

A key development during the quarter was the company’s entry into liquid cooling solutions for data centres. It completed its first commercial dispatch of advanced flow control components and skid assemblies for this segment. The company is scaling up capacity to 15,000 units annually, with completion expected by June 2026. This expansion is backed by rising global demand for data centres and AI infrastructure, where efficient cooling systems are becoming essential.

Capacity expansion remains a central focus. Aeroflex has increased its hose capacity to 17.5 million metres annually, with further additions planned over the next few quarters. At the same time, it is investing in automation and process improvements, including robotic welding and annealing facilities, to improve consistency and handle more complex applications. A new plant in Pune is also being set up to support the growing skid assembly business.

The 75% Export Advantage

Exports continue to be a key driver, contributing nearly three-fourths of total revenue. Growth in exports was supported by strong demand from the US and Europe, along with improving traction in the EU market. The company also expects trade agreements to enhance its competitiveness in overseas markets over the medium term.

The broader trend highlights a clear positioning. Aeroflex is not competing as a volume manufacturer. It is building capabilities in specialised industrial applications where precision, reliability and engineering expertise matter more than scale. This aligns with the broader investment approach seen in portfolios that favour niche manufacturing plays with long-term growth visibility.

Looking ahead, the company’s performance will depend on execution of its expansion plans and the pace of adoption in newer segments such as liquid cooling. While global demand remains supportive, near-term uncertainties around tariffs and customer onboarding could influence growth. Even so, the company’s focus on high-value segments and strong export linkages provides a stable foundation for gradual scale-up.

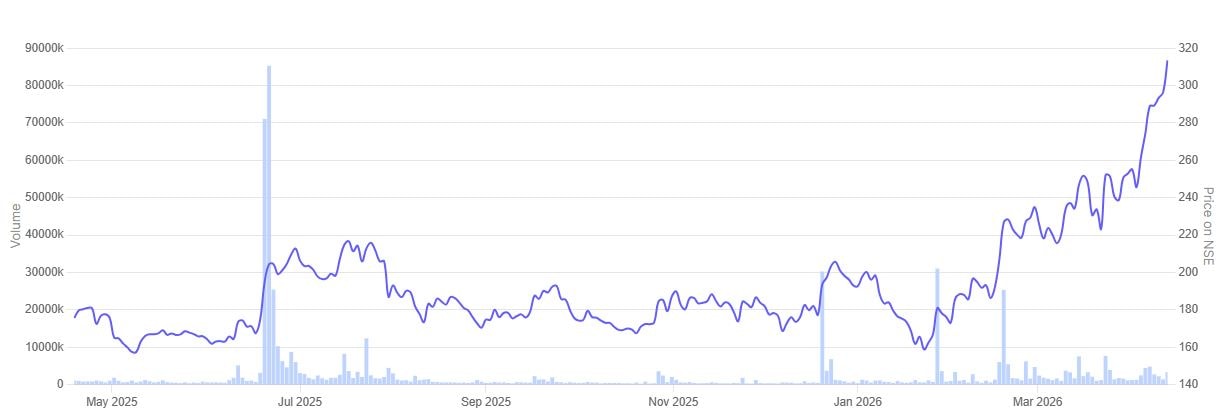

In the past year, the share price of Aeroflex Industries rallied 80.1%.

Aeroflex Industries 1 Year Share Price Chart

#2 Shaily Engineering Plastics: Precision Manufacturing for Global Pharma

Shaily Engineering Plastics is engaged in the manufacture and sale of injection moulded precision plastic components, sub-assemblies for various requirements of Original Equipment Manufacturers (OEM). It also offers secondary operations in plastics like vacuum metalizing, hot stamping, and ultrasonic welding.

As of 31st March 2026 Ashish Kacholia held 5.2% stake of Shaily Engineering Plastics which is worth Rs 451.2 crore.

Shaily Engineering Plastics reported a strong performance in the December quarter. The growth was driven by its healthcare segment. Revenue stood at Rs 251 crore in Q3FY26. This was a 27% YoY increase. Net profit came in at Rs 37 crore. It grew 48% YoY. Margins also improved. EBITDA margin stood at 26.5%. This reflected operating leverage and a better product mix.

Medical Device Boom: Why GLP-1 is Shaily’s Growth Catalyst

The growth was led by a sharp scale-up in healthcare. This segment now contributes over 40% of total revenue. It focuses on drug delivery devices such as pen and auto-injectors. Demand has been strong, especially for GLP-1 therapies (weight loss related). In contrast, the consumer segment remained weak. Demand in Europe and the US has slowed. This shows a gradual shift away from commoditised products.

This shift is important. The company is moving beyond general plastics manufacturing. It is focusing on niche, high-precision applications. These are largely in regulated industries. Products include complex medical devices. Entry barriers are high. Contracts are long-term. Capacity expansion is also linked to customer commitments. Many of these are backed by take-or-pay agreements. This gives better demand visibility.

Abu Dhabi Expansion: Scaling to 75 Million Units

A key development was the Abu Dhabi facility. It will manufacture pen and auto-injectors. Planned capacity is about 75 million units annually. The investment is around Rs 300–350 crore. The plant is expected to be operational by Q4FY28. This will expand the company’s global footprint. It will also bring it closer to international clients.

In India, capacity additions are ongoing. New high-speed assembly lines are being set up. Some delays in qualification have been reported. Full ramp-up is expected next year. Most domestic expansion is backed by contracts. The Abu Dhabi facility also has partial capacity commitments.

The company is also exploring new areas. These include semiconductor components and precision parts for electronics. These segments are still early stage. They are expected to scale over the next 12 to 24 months.

Exports remain a key driver. They account for over 70% of revenue. This shows strong integration with global supply chains. At the same time, it exposes the company to global demand cycles. This was visible in the slowdown in the consumer segment.

The overall strategy is becoming clearer. The company is positioning itself as a specialised manufacturer. It is focusing on niche, high-value segments. It is not competing on volume alone. This approach aligns with investors who prefer scalable niche businesses.

Going ahead, execution will be important. Capacity ramp-up will be a key monitorable. Demand in healthcare will remain critical. Near-term pressure in legacy segments may continue. However, the focus on niche manufacturing provides long-term visibility.

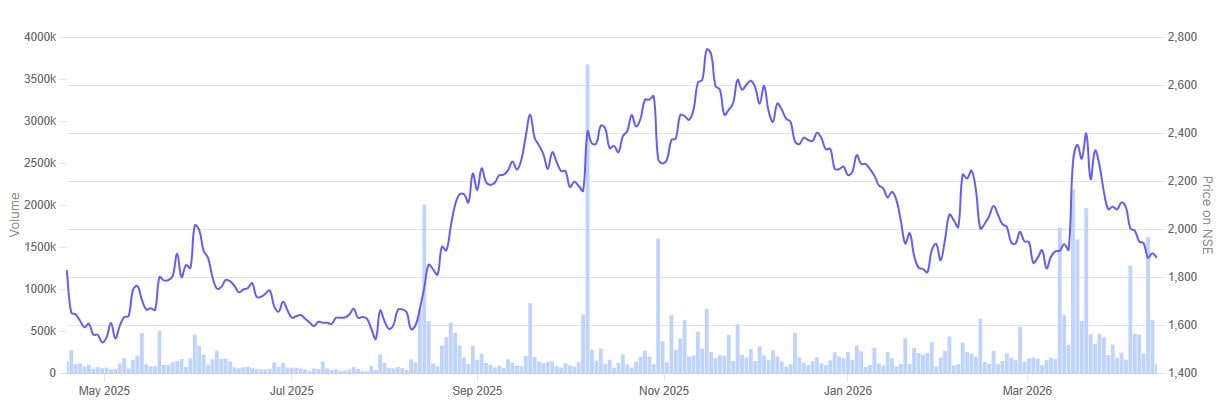

In the past year, the share price of Shaily Engineering Plastics is up 1.9%.

Shaily Engineering Plastics 1 Year Share Price Chart

#3 Fineotex Chemical: Specialising in High-Margin Solutions

Incorporated in 1979, Fineotex Chemicals is engaged in the business of manufacturing auxiliaries and specialty chemicals for textiles, construction, water treatment, fertiliser, leather, and paint industries.

As of 31st March 2026 Ashish Kacholia held 2.6% stake of Fineotex Chemical which is worth Rs 69.6 crore.

Fineotex Chemical reported a strong performance in the December quarter. Revenue stood at Rs 184 crore in Q3FY26. This was a 46% YoY increase. The growth was supported by both domestic demand and expansion in international business. Net profit for the quarter stood at Rs 30 crore, up 7.1% YoY.

Strategic Expansion: How Oilfield Specialities Diversify Revenue

A key driver during the quarter was the acquisition of a controlling stake in a US-based specialty chemicals company. The acquisition was completed in December. It added nearly 80,000 metric tonnes of capacity. It also expanded the company’s presence in oilfield chemicals. The business includes advanced fluid additives and end-to-end solutions for drilling and energy applications. This marks a shift towards more technology-driven segments.

Trade Tailwinds: Navigating the UK-EU Export Corridor

The company is also seeing structural tailwinds in its core textile chemicals business. Trade agreements with the US, UK and EU are expected to improve export competitiveness. Removal of tariffs in key markets is likely to support demand. Textile exports are projected to grow meaningfully over the next few years. This directly benefits specialty chemical suppliers involved in processing and finishing stages. These stages consume higher volumes of value-added chemicals.

There is also a visible shift in product mix. Demand is moving from commodity chemicals to premium, performance-based formulations. This is driven by stricter environmental norms and evolving global standards. Fineotex operates in this segment. It focuses on customised solutions and application-specific chemistries. This positions the company within a niche part of the industrial value chain rather than a bulk chemical producer.

Exports have gained traction. Export contribution rose to 48% in Q3FY26 from 25% in the previous quarter. This reflects stronger integration with global markets. The company is also expanding its presence in North America. Growth in energy and refining activity is expected to support demand for specialty additives and oilfield chemicals.

Capacity utilisation stood at around 64%. The company has already commissioned a new plant at Ambernath. This provides room for further growth without immediate large-scale capex. Additional investments are expected to remain moderate in the near term. Focus remains on improving utilisation and expanding high-value segments.

The broader strategy highlights a clear positioning. Fineotex is not competing as a volume-driven chemical manufacturer. It is building capabilities in specialised applications across textiles, oil and gas, and water treatment. This aligns with the broader investment approach seen in portfolios that favour niche manufacturing and specialty segments with scalable demand.

Going ahead, growth will depend on successful integration of the US acquisition and recovery in textile demand. Early signs of improvement in order books are visible. However, global demand cycles and pricing pressures remain key monitorables. The company’s focus on high-value, niche segments provides a clearer path to long-term growth.

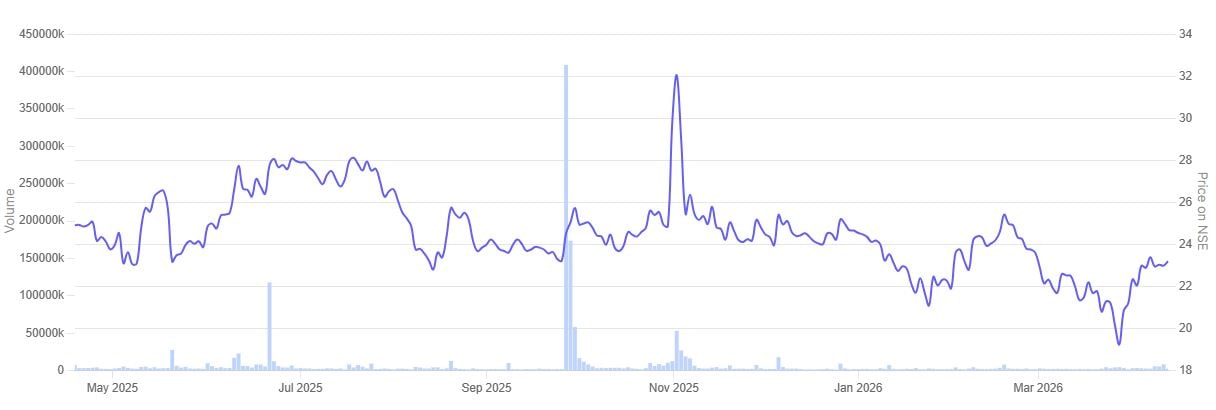

In the past year, the share price of Fineotex Chemical tumbled 53.4%.

Fineotex Chemical 1 Year Share Price Chart

#4 Knowledge Marine & Engineering Works: Dominating India’s Specialized Dredging Niche

Incorporated in 2015, Knowledge Marine & Engineering Works provides dredging services, owning and operating marine craft, and repairing, maintaining and refitting marine crafts and marine infrastructure.

As of 31st March 2026 Ashish Kacholia held 2.9% stake of Knowledge Marine & Engineering Works which is worth Rs 124.9 crore.

Knowledge Marine & Engineering Works reported a strong performance in the December quarter. Revenue stood at Rs 90 crore in Q3FY26. This reflects a 55% YoY growth. Net profit came in at Rs 33 crore, up 106%. Profitability remained strong, supported by improved execution and operating leverage. EBITDA margin stood at around 43%, indicating high efficiency in operations.

The growth was driven by expansion across core marine segments. The company operates in dredging, marine services and shipbuilding. These are specialised areas within the broader infrastructure value chain. Demand has been supported by government focus on ports and inland waterways. This creates a steady pipeline of long-term contracts.

Order Book Analysis: Breaking Down the Rs 1,500 Crore Pipeline

Order inflows remained strong during the quarter. The company secured shipbuilding orders worth over Rs 230 crore from Inland Waterways Authority of India. These include work boats, survey vessels and dredgers. It also won long-term contracts worth around Rs 700 crore for green tug construction and chartering. These projects are to be executed over a 15-year period. In addition, a capital dredging contract at JNPT worth Rs 50 crore was secured.

The order book stands at around Rs 1,500 crore. This provides strong revenue visibility over the next few years. The pipeline remains robust, with bids worth over Rs 3,000 crore under evaluation. The company currently operates a fleet of 45 vessels. Fleet utilisation remains high, with most assets deployed across contracts.

Asset Independence: The Shipbuilding Infrastructure Shift

Capacity expansion is ongoing. The company plans to invest close to Rs 100 crore in developing a shipyard. This facility will focus on building smaller vessels such as tugs and support crafts. The investment is expected to be spread over the next few years. This will help reduce dependence on external vendors and improve execution timelines.

The company is also exploring international opportunities. The Bahrain project remains active, though operations are yet to resume. Deployment is contingent on identifying a suitable vessel at viable cost. Management indicated that capital allocation will remain disciplined, with a focus on asset utilisation and returns.

The broader positioning remains clear. The company is not a generic infrastructure contractor. It operates in specialised marine engineering segments such as dredging and vessel operations. These are niche areas with limited organised players. As demand for waterways and port infrastructure increases, such businesses are likely to see steady growth.

Going ahead, execution of the large order book and timely deployment of assets will be key. Demand visibility remains strong. However, asset acquisition and project timelines will need close monitoring. The company’s focus on niche marine segments provides a defined growth path, but scalability will depend on consistent execution.

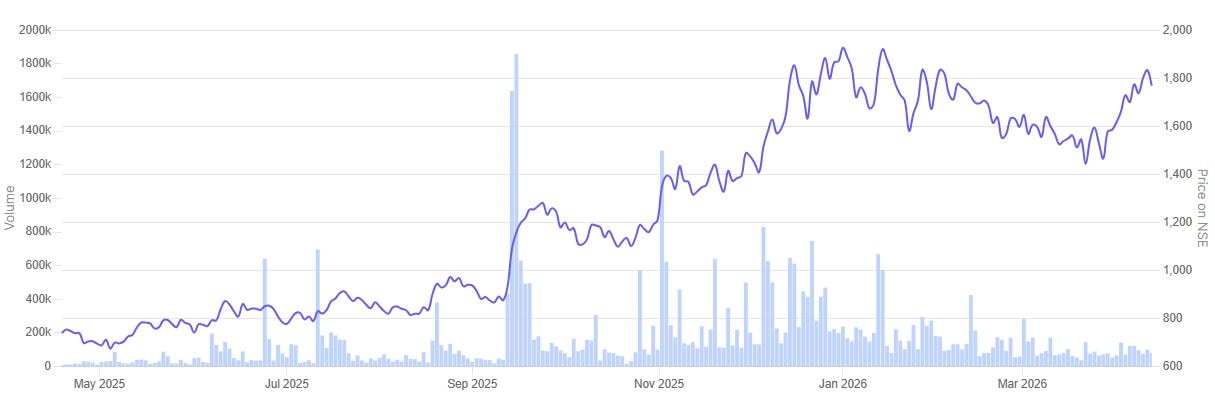

In the past year, the share price of Knowledge Marine & Engineering Works rallied 140.8%.

Knowledge Marine & Engineering Works 1 Year Share Price Chart

#5 Jain Resource Recycling: Scaling the Circular Economy

Incorporated in 2022, Jain Resource Recycling and its subsidiaries specialize in recycling non-ferrous metal scrap and producing lead, copper, and aluminium alloys. Its lead ingots are London Metal Exchange-registered, ensuring international quality standards. The company also trades non-ferrous metals and commodities.

As of 31st December 2025 Ashish Kacholia held 1.1% stake of Jain Resource Recycling which is worth Rs 163.8 crore.

Jain Resource Recycling reported a steady operational performance in the December quarter. Revenue for the quarter stood at Rs 2,676 crore up 55% YoY. Net profit for the quarter stood at Rs 127 core up 102.4%. EBITDA margin stood at around 7.2% in Q3FY26. Net profit margin improved to about 4.5%, compared to 3.3% in the same period last year. The improvement reflects better operating leverage and a favourable product mix.

The company operates in non-ferrous metal recycling. This includes copper, lead and aluminium. It is not a commodity producer in the traditional sense. Instead, it sits in a specialised segment of the value chain. It processes scrap into usable metal. This makes it part of the circular manufacturing ecosystem. Demand here is driven by global metal shortages and sustainability push.

Scaling Margins: The Anode and Cathode Roadmap

Growth is being led by a shift towards value-added products. The company is expanding its copper segment through forward integration. This includes products such as anodes, cathodes, wire rods and busbars. Construction of the value-added copper facility is around 80% complete. Key machinery has already been delivered. The anode plant is expected to start in February 2026. The cathode plant is likely to follow in March 2026.

Capacity expansion will continue beyond commissioning. Anode capacity is expected to double to 1,600 tonnes per month in Q1FY27. Cathode capacity is also planned to double by Q3FY27. Additional segments such as wire rods and busbars are expected to come online in phases. This transition is important. It reduces dependence on raw scrap margins and improves profitability through product mix.

Parallel expansion is underway in recycling infrastructure. A new copper recycling plant in Ahmedabad is being set up through a joint venture. The plant will process around 72,000 tonnes of scrap annually. It is expected to be operational from June 2026 in phases. This will strengthen sourcing and processing capabilities.

The company is also expanding globally. It has approved a 25% investment in a Kuwait-based recycling venture. This project will focus on battery scrap processing. It is expected to be operational by Q3FY27. The move is aimed at securing raw material and expanding presence in the Middle East market.

Strategic Extraction: Tapping the Antimony Niche

In addition, the company is entering niche extraction segments. It is scaling tin recovery capacity and moving into antimony extraction from lead scrap. This is a specialised process with limited domestic competition. The antimony plant is expected to be commissioned in Q3FY27. This segment offers higher value realisation compared to standard recycling operations.

The broader strategy remains focused on two levers. Volume expansion through new plants. And margin expansion through value-added products. This positions the company within a niche manufacturing space rather than a pure commodity cycle.

Going ahead, execution of multiple projects will be key. The company is entering a phase where several capacities will come online together. If timelines are maintained, this could support both volume growth and margin improvement. However, working capital cycles and metal price volatility remain factors to watch in the near term.

In the past year, the share price of Jain Resource Recycling rallied 32.5%.

Jain Resource Recycling 1 Year Share Price Chart

Valuation Audit: Are These Micro-Niches Priced for Perfection?

Let’s now turn to the valuations of the companies in focus, using the Enterprise Value to EBITDA multiple as a yardstick.

Valuations of Companies in focus

| Sr No | Company | EV/EBITDA Ratio | Industry Median | ROCE | ROE |

| 1 | Aeroflex Industries | 44.9 | 11.4 | 22.3% | 16.6% |

| 2 | Shaily Engineering Plastics | 35.6 | 13.8 | 17.0% | 15.3% |

| 3 | Fineotex Chemical | 18.5 | 15.0 | 23.8% | 18.4% |

| 4 | Knowledge Marine & Engineering Works | 43.1 | 31.5 | 24.7% | 25.8% |

| 5 | Jain Resource Recycling | 25.7 | 19.4% | 27.2% | 39.0% |

Jain Resource Recycling has the highest return ratios here. Return on capital employed (ROCE) is 27.2% and return on equity (ROE) is 39%. Knowledge Marine also looks strong with ROCE at 24.7% and ROE at 25.8%. Fineotex Chemical is steady with ROCE of 23.8% and ROE of 18.4%. Aeroflex Industries and Shaily Engineering Plastics are lower than these three but still decent.

Valuations are where the gap shows up. Aeroflex Industries is at 44.9 EV/EBITDA versus an industry median of 11.4. Shaily Engineering Plastics is at 35.6 compared to 13.8. Knowledge Marine is at 43.1 against 31.5. Fineotex Chemical is closer to its industry at 18.5 versus 15. Jain Resource Recycling is at 25.7, which is above the median but not as stretched as Aeroflex or Shaily.

Even though these companies are from different segments, there is a link. Each one operates in a small, specific part of a larger industrial chain. Aeroflex is into flow components. Shaily makes precision plastic parts. Fineotex supplies chemicals used in processing. Knowledge Marine works in dredging and marine services. Jain Resource Recycling is into metal recycling and moving towards copper products.

Some of these stocks are clearly priced for growth. Aeroflex and Shaily stand out here. Knowledge Marine also trades above its industry level. Fineotex looks more balanced. Jain Resource Recycling has strong return ratios, and the valuation shows the market is factoring in its expansion.

These names are better followed over time. The key thing to watch is execution. Growth in revenue, margins and capacity will decide how these valuations play out.

Conclusion

Niche manufacturing often sounds like a strong investment idea. Limited competition, focused operations, and the ability to build expertise can make these businesses stand out. But in practice, it is not always that simple. Many of these segments are still evolving. Scale can take time. Demand visibility is not always clear. Execution becomes critical.

That is where the difference lies. Identifying a niche is one part. Building a business in that niche is another. Some companies are able to expand steadily and improve margins. Others struggle with capacity utilisation or pricing pressure. The gap between potential and actual performance can be wide.

Seen in this context, this set of stocks reflects a certain pattern. The focus is on companies operating in smaller, specialised parts of a larger industrial chain. These are not obvious sector leaders. They are businesses trying to build scale within narrow segments.

For retail investors, the takeaway is simple. Such portfolios can offer direction, but they are not a blueprint to copy. Many of these stocks are already trading at a premium. Entry price, holding period, and risk appetite will make a big difference.

In the end, returns will depend on execution. If these companies are able to scale their niche into a larger opportunity, the story holds. If not, the same niche can become a constraint.

You can track how these are progressing by adding stocks to your watchlist.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Ekta Sonecha Desai has a passion for writing and a deep interest in the equity markets. Combined with an analytical approach, she likes to deep dive into the world of companies, studying their performance, and uncovering insights that bring value to her readers.

Disclosure: The writer and her dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.