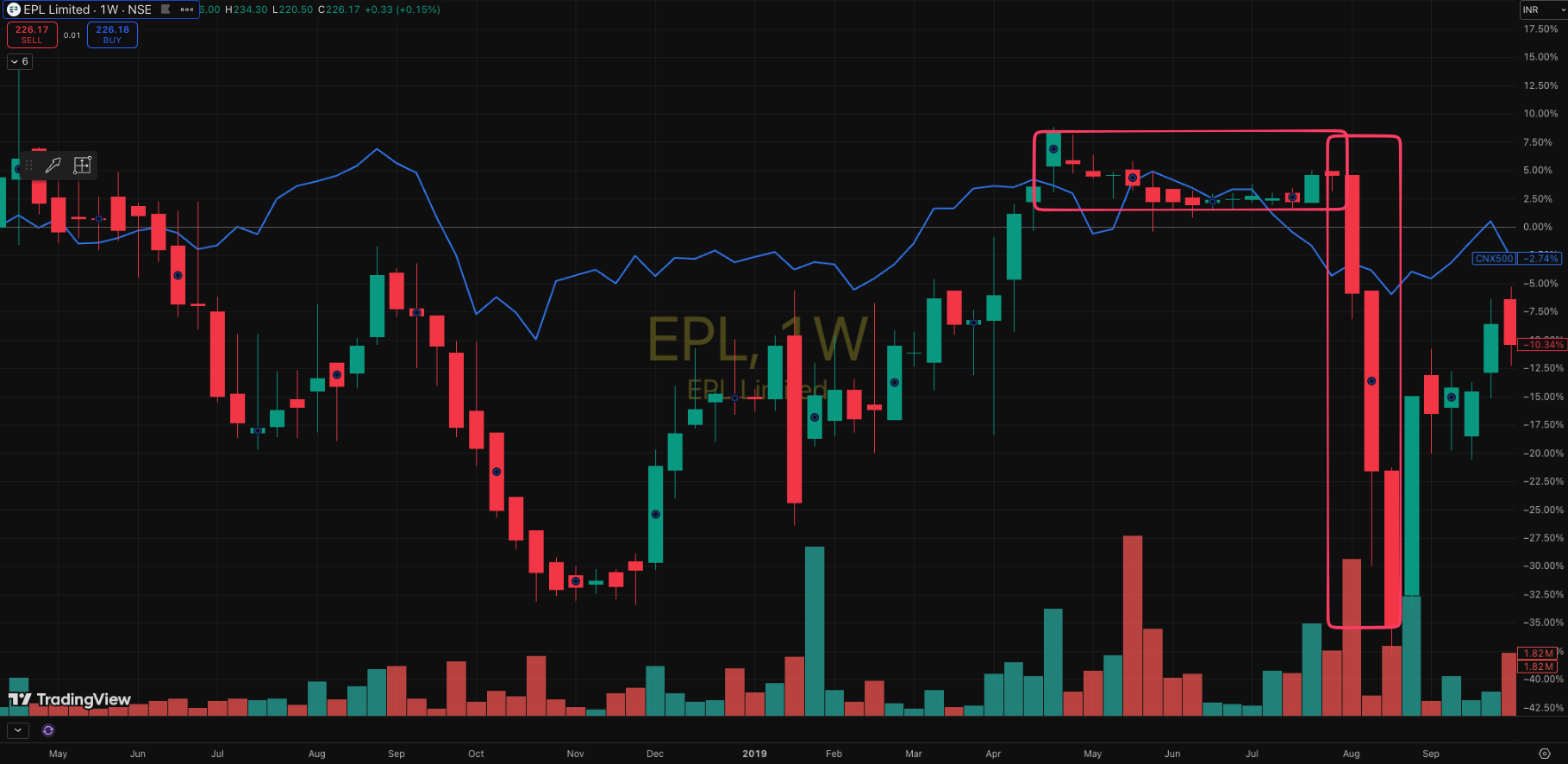

The year is 2019. Blackstone acquires Essel Propack Ltd from its promoter – Ashok Goel at Rs 139 per share, trading at 21x trailing Price to earnings multiple and 12-13x EV/EBITDA.

This transaction triggers an open offer mandating Blackstone to buy up to 26% from public shareholders at the same price. By 9th August 2019, the open offer ends.

Shareholders who had jumped in for the open offer arbitrage profits (difference between market price and offer price) and whose shares couldn’t get tendered dumped stock in the open market and the share price dropped to just Rs 82 per share.

Post open offer stock price beatdowns are normal.

With much fanfare Blackstone steps in – revamps the board – puts out a glossy presentation – churns out a new strategy & KPI targets and the stock skyrockets from Rs 82 per share to Rs 292 per share in August 2020.

If covid-19 happened, EPL ltd – the name Blackstone gave it, didn’t get the memo.

Blackstone books profits

Encouraged by the quick stock price returns following its August 2019 investment in Essel propack ltd, Blackrock pared down its holding by about 25% (retaining over 50%) by August 2020.

The stock hasn’t hit those levels ever since.

But why does that concern us? Because in 2025, Blackstone sold a majority of its stake in EPL Ltd to Indorama Ventures ltd (IVL) – a Thailand listed entity run by an M&A hungry management.

The deal was done at Rs 240 per share with only 25% of its 56% odd holding exchanging hands i.e. Blackstone continued to hold a 26% stake in EPL. By May 2026. one year post the initial tranche, IVL chose to increase its shareholding without dishing out more cash.

It did this by merging one of its ‘rigid packing’ businesses into EPL ltd.

In effect, this is an extended special situation at EPL.

Is this an opportunity? Or is this just another M&A ‘hall of shame’ deal? Let’s dig in.

The Deal

So far, the deal has taken place in two steps.

Leg 1: Blackstone (Epsilon Bidco Pte.Ltd) sold 24.8% of its 51.3% holding in EPL ltd to IVL on May 27th 2025, at Rs 240/share. The number is intentionally kept below 26% to avoid triggering an open offer.

It was obvious there was going to be a follow up deal but very few anticipated how it would happen.

Leg 2: Agreement to merge Indovida India private ltd (IVL subsidiary) – IVL’s “rigid packaging business” with EPL ltd such that IVL shareholding goes from ~25% to ~51%, while both the public and Blackstone get diluted by 36% each.

That sounds bad. But whether it really is or not, depends on what you’re getting or the dilution. But something about this structure makes me super curious.

That Blackstone decided to retain 16% and the right to nominate 1 board member, essentially creates an opportunity to coattail them? More on this later too.

How the deal was valued

When promoters merge their privately held entity into a listed company, the biggest concern is whether they will short-change existing shareholders in the listed entity.

Typically, such a scenario plays out with promoter entity on one side of the table and non-promoters on the other. This time it’s different.

Blackstone is a pseudo promoter whose interests are aligned, even if temporarily, with the public shareholders because it’s on the way out. So, diluting its shareholding at a less than fair valuation would be a no go.

So, what’s this deal actually worth?

Firstly, no cash is changing hands here. This is a share swap.

Both Blackstone and IVL agreed to value EPL ltd at Rs 339 per share (vs Rs 240/share in May 2025). That’s a 70% premium to closing price before the announcement (about Rs 199 per share).

From 30th April 2026 closing price of Rs 226 per share, EPL ltd still trades at a 33.3% discount, assuming that is indeed the true value. However, the real discount implied by the merger valuation is higher. More on that later.

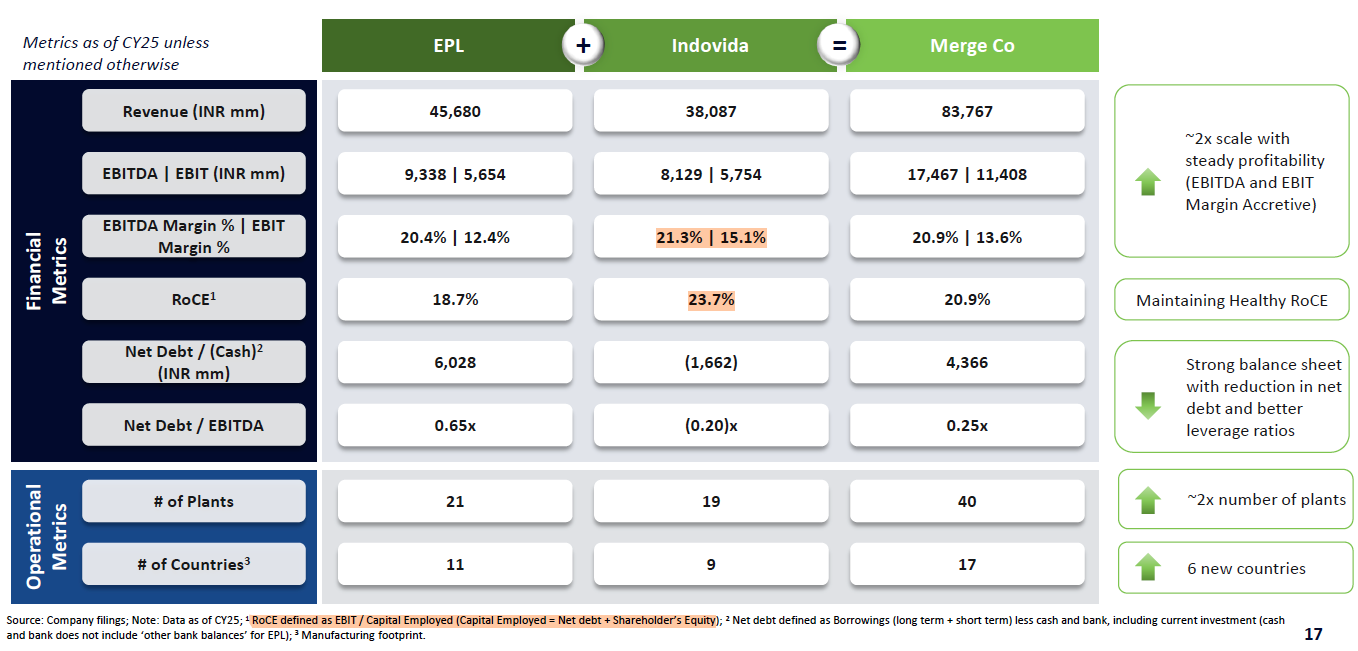

Merger valuation pegs EPL’s equity value of about INR 11,000 crore (~$1.2 bn).

Indovida India, the unlisted Indian holding company that Indorama Ventures has stuffed all its emerging-market packaging subsidiaries into, is being valued at INR 6,250 crore (~$0.75 bn).

Add the two together and the combined company that will emerge from this merger is worth, on paper, around $2 bn or Rs 17,250 crores.

For every 10,000 shares of Indovida that Indorama owns, it gets 286 fresh EPL shares, a number arrived at jointly by BDO and Duff & Phelps as valuers, with EY as the fairness-opinion provider.

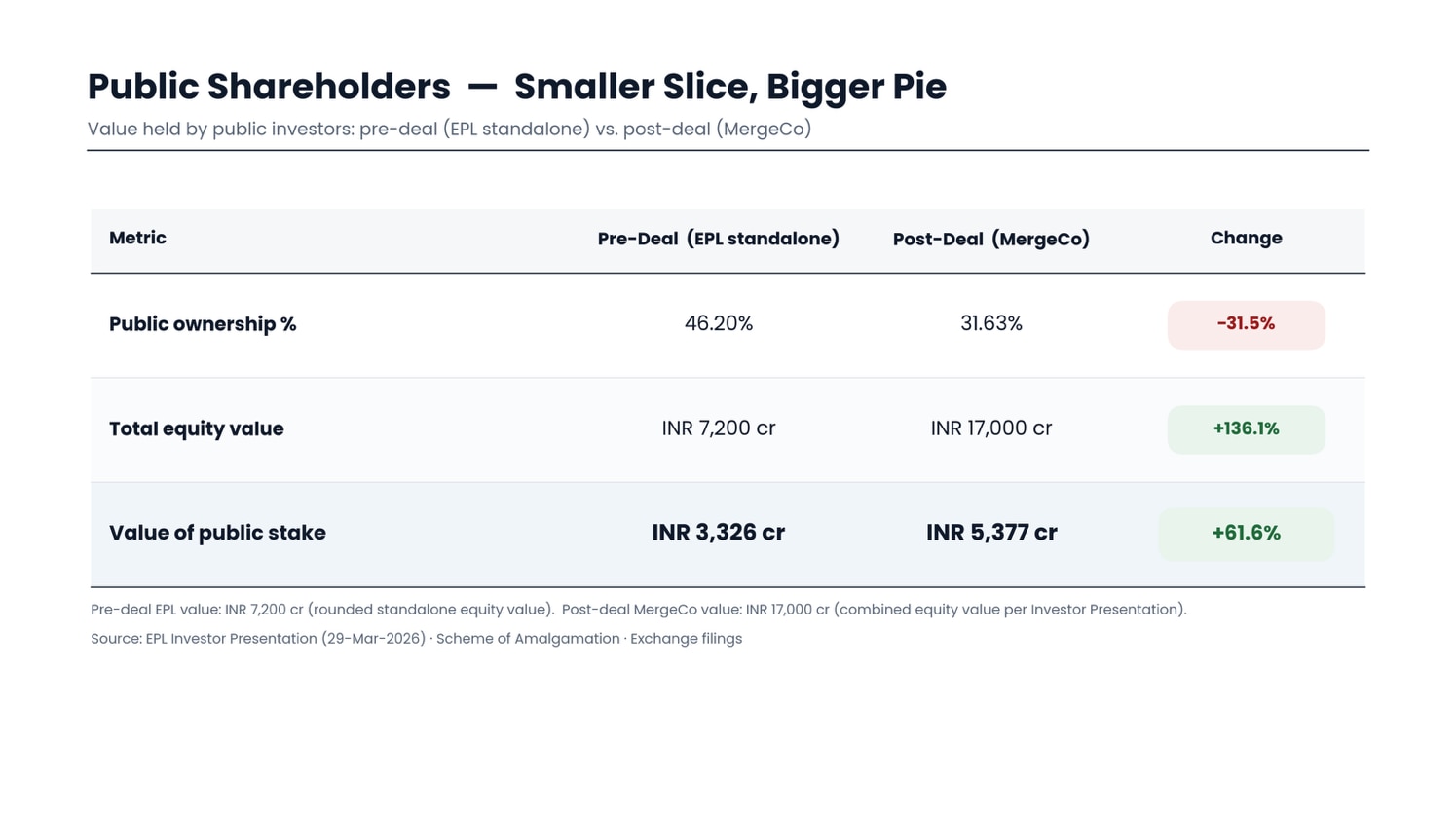

That mechanical swap is what produces the new cap table you saw above: Indorama goes from 24% to just under 52%, Blackstone gets diluted from 26% to just under 17%, and the public falls from 46% to a little over 31%.

The bit that matters: who’s getting the better deal?

EPL is being valued at roughly 12.5x its trailing EBITDA. Indovida is being valued at roughly 7.5x.

Management’s own framing is that “EPL gets a 55% premium to Indovida”, or equivalently, “Indovida is being brought in at a 35% discount”.

In plain English: if you owned an EPL share before this deal, you are about to own a slice of a company that’s getting Indovida’s earnings and cash flows folded in at a much cheaper multiple than your own stock.

Every rupee of new shares being issued to Indorama is buying more underlying business than that same rupee of your existing EPL stake represents. That is the textbook definition of an EPS-accretive merger, and the company has guided that this will indeed be EBIT margin (+120 bps), ROCE (+220 bps) and EPS accretive from the very first full year.

This sounds great. But there are some questions an investor should ask.

This raises the question: Why is Indovida being valued so cheaply, then?

Three reasons.

The first is that Indorama already owns 24% of EPL and 100% of Indovida. The merger is what tips them past 50% and into formal promoter control.

Under SEBI’s takeover code, a court-sanctioned merger that gets majority public-shareholder approval is exempt from the open-offer requirement.

So Indorama isn’t buying control with cash at a marked-up price, it is negotiating control through a swap that needs the public to vote yes. The simplest way to ensure that yes-vote is to value your own asset modestly and the listed asset (EPL Ltd) richly.

Which is exactly what appears to have been done.

The second is purely about how markets price these businesses.

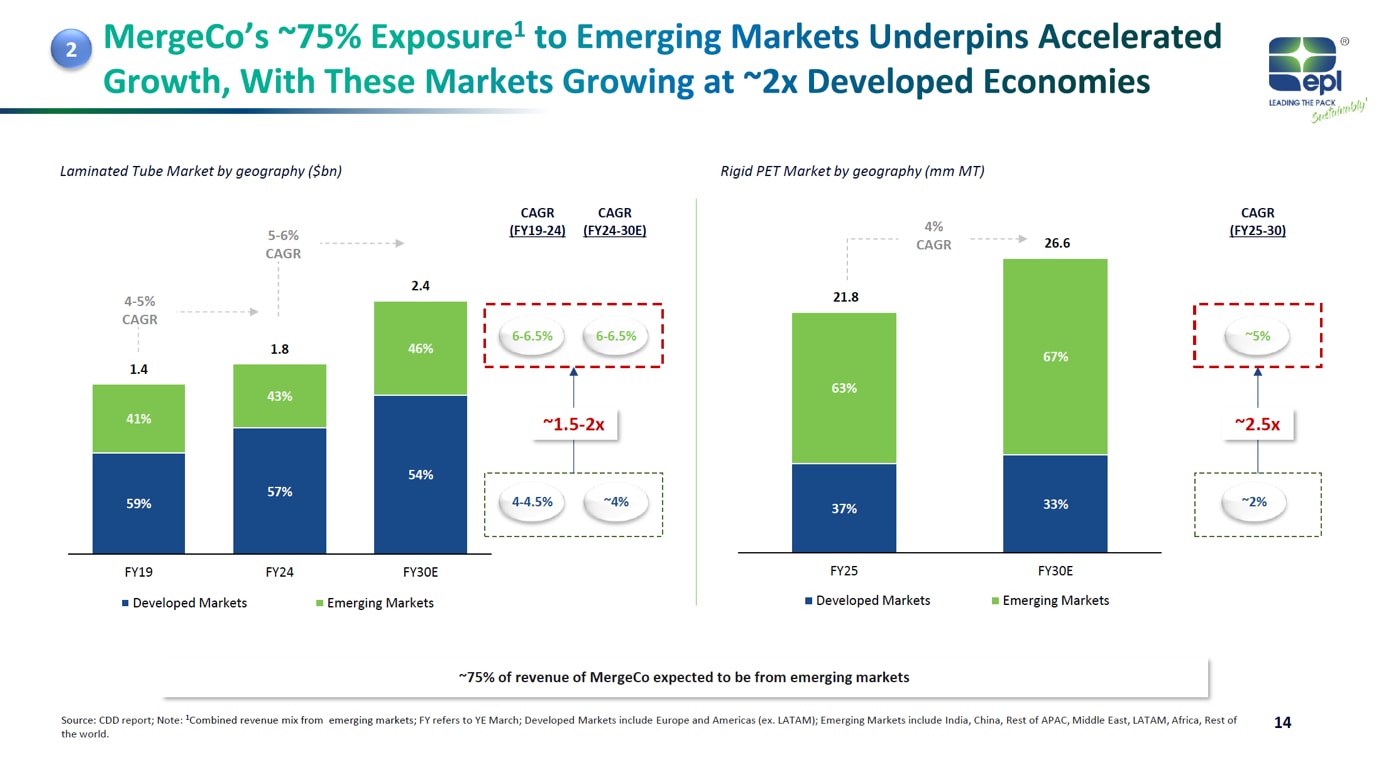

EPL is the global #1 in laminated tubes, a specialty, sticky, FMCG-customer-locked business.

Indovida is mostly a PET preform and bottle player. A respectable, profitable business, but one that globally trades at lower multiples because preforms are closer to a commodity than tubes are. A 3-5x EV/EBITDA multiple gap between specialty and commodity packaging is normal in private M&A. The 35% discount sits squarely inside that range.

The third is liquidity. EPL is publicly traded with real free float. Indovida is an unlisted holding company sitting on top of nine emerging-market subsidiaries in places like Nigeria, Egypt and Vietnam. Everything aside, an unlisted EM-heavy operating asset should not get the same multiple as an Indian-listed leader.

Then there’s IVL’s side of the story. According to IVL 2.0 – a value unlocking strategy at the Thailand listed parent (IVL) involves restructuring of its debt laden, cyclical business whose stock has been declining over the last 4 years, taking over a listed entity in India and merging its private business is effectively a backdoor listing route.

IVL’s investor presentation filed with Thai stock exchange suggests it wants to leverage from the generous valuations being assigned to companies on NSE & BSE.

Valuation: A reality check on the 70% “premium”

The 70% premium to market is not a tender offer. Nobody is being asked to sell their EPL shares at INR 339. The premium is purely the price-tag the two boards have agreed on for the swap math.

I call it the ‘Signal price’.

The way public shareholder actually pocket that premium is through dilution avoidance. Meaning by valuing EPL high, fewer new shares need to be issued, so each existing shareholder ends up owning more of Merged Co’s earnings than they would have at a lower agreed price.

The second way they benefit is if/when market value matches up to the value of the combined co’ of $2 billion or Rs 17,500 cr. If actual market value of combined co’ catches up to this ‘implied value’, public shareholders get an upside of 61%.

What’s the catch?

First. Indovida India ltd is an engineered entity, created specifically for the purpose of merging and getting back-door listing on NSE/BSE.The official balance sheet has still not been filed with the stock exchanges so we don’t know what we don’t know.

Second.Are there growth opportunities available for the combined entity? In segments that are pegged to grow 5-6.5%, what kind of topline, EBITDA & bottom-line growth can the combined EPL-Indovida entity aim for?

Leading up to the merger, EPL ltd has grown Revenue at 7%, EBITDA at 13% and PAT at 19% aided by lower cost of goods sold and cost efficiencies leading to higher EBITDA margins. At a trailing EBITDA margin of 20%, our initial view is that further room for expansion seems limited.

Sure, management has highlighted $30-50 millions of synergy benefits but we would be conservative in factoring those in just yet.

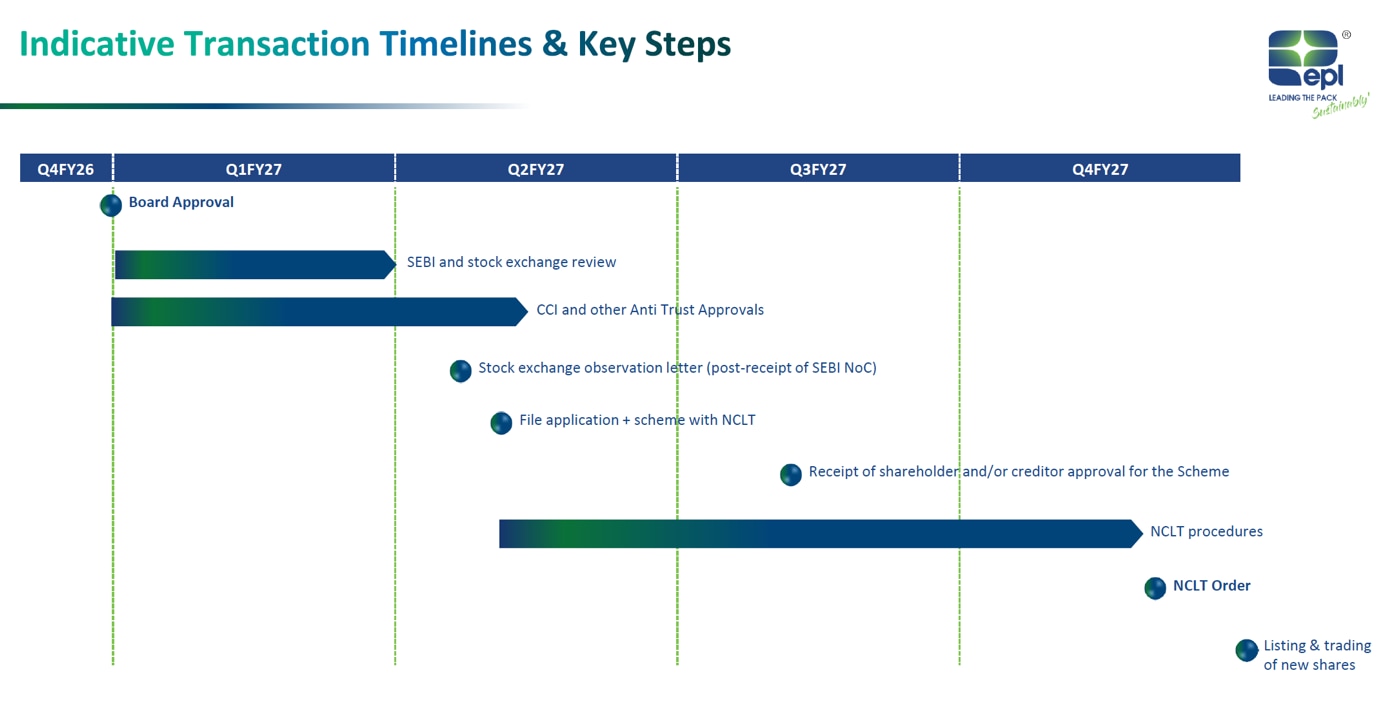

Third. Merger process completion is still 12 months away with pending regulatory and shareholder approvals remaining.

Fourth. Just one year ago, when actual cash exchanged hands between Blackrock and Indovida, the same EPL was pegged at Rs 240/share. In the recent, noncash based deal its being pegged at Rs 339/share. What’s changed so materially that the same set of buyer and seller are agreeing to value the same asset higher by 40%?

In conclusion, it seems like a great deal on paper with a decent upside. How it plays out depends on timeline, quality of earnings of Indovida India limited and timely approvals.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Disclaimer:

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

Rahul Rao has been Investing since 2014. He has helped conduct financial literacy programs for over 1,50,000 investors. He helped start a family office for a 50-year-old conglomerate and worked at an AIF, focusing on small and mid-cap opportunities. He evaluates stocks using an evidence-based, first-principles approach as opposed to comforting narratives.

Disclosure: The writer or his dependents do NOT Hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.

– 22K, 24K Gold, 1gm, 10gm Silver Price Today in Delhi, Mumbai, Chennai, Hyderabad, Bengaluru, Ahmedabad, Kerala | Sona, Chandi Rate Today in India – Gold Pulse News")