Welcome to the latest edition of Dividend Hunter. Over the past few weeks, we have analyzed companies where strong cash flows could translate into consistent dividends going forward. In our previous edition, we covered a global IT firm with a presence in artificial intelligence offering 6.1% yield. In this edition of Dividend Hunter, we analyse a Navratna public-sector giant that forms the bedrock of India’s economy. A company that has consistently generated massive cash flows and just rewarded its shareholders with yet another generous dividend payout.

With initiatives like PM Gati Shakti and the National Infrastructure Pipeline in full swing, securing high-quality raw materials remains a critical ongoing theme for the nation.

As infrastructure development scales up, steel demand is also expected to rise steadily. Notably, the construction and infrastructure sectors alone account for more than 60% of India’s overall steel consumption.

Higher steel demand, in turn, increases the need for a reliable supply of high-grade iron ore. India’s per capita steel consumption of 103 kg (2024) is also low against the global average of 215 kg.

This necessitates long-term resource security important for India’s industrial growth. To fill this gap, India aims to aggressively scale its crude steel capacity to 300 million tonne (MT) by 2030, and a staggering 500 MT by 2047.

This exact need creates an opportunity for a specific set of mining companies. While many players focus on downstream steel manufacturing, a select few specialize in ensuring the fundamental raw materials are pulled from the earth efficiently and flawlessly.

One dominant market player in this niche is NMDC Limited.

NMDC is a Navratna Public Sector Enterprise (PSE) operating under the Ministry of Steel and stands tall as India’s single largest iron ore producer.

The Strategic Fe Grade: How NMDC Controls the Upstream Value Chain

NMDC sits right at the critical juncture of resource security and industrial growth. It helps domestic steelmakers and global markets safely scale their operations by supplying premium 64% Fe grade iron ore.

It doesn’t just dig up rocks.

NMDC specializes in highly mechanized, cost-efficient mining from its 5-star rated complexes in Chhattisgarh and Karnataka. This ensures that its supply chain fulfills high demand, helping the country avoid supply bottlenecks.

NMDC’s business model translates into strong financial strength, thanks to surging demand for core commodities. It generates strong cash flows and maintains a pristine balance sheet.

Even better, they are actively sharing this wealth with investors. The company boasts an impressive track record, maintaining an average dividend payment of around 793% on its face value over the last five years.

Most recently, in FY25, it declared an interim dividend of ₹2.30 per share and recommended a final dividend of ₹1.00 per share. But will this dividend payment be sustainable? We will try to find out in this story.

The Bedrock of India’s Infrastructure: Understanding the NMDC Footprint

NMDC is India’s largest producer of iron ore.

The extraction and sale of iron ore is the company’s primary business, accounting for approximately 96% of its total turnover.

Geographic Dominance: From Chhattisgarh to Karnataka

The company operates four fully mechanized iron ore mining complexes located in Chhattisgarh and Karnataka.

The Bailadila sector in Chhattisgarh houses the Kirandul andu Bacheli mining complexes. The Donimalai sector (Karnataka) is in the Bellary-Hospet region, which includes the Donimalai and Kumaraswamy iron ore mines.

NMDC supplies high-grade iron ore products, including lumps and fines, with an iron (Fe) content ranging from 60% to 65%. The company also operates a 1.2 million tonne per annum (MTPA) pellet plant in Donimalai, which converts iron ore fines into pellets for use in the steel industry.

In addition, NMDC’s diversified mining operations also include diamond and coal. NMDC operates the Diamond Mining Project in Panna, Madhya Pradesh, which is currently the only mechanized diamond mine in Asia.

Energy Security Pivot: Transitioning into Domestic Coal Mining

It is expanding into domestic coal mining to support energy security. It has been allocated the Tokisud North (non-coking coal) and Rohne (coking coal) mine blocks in Jharkhand. Mining operations commenced in FY26.

Global Footprint: Gold Mining and Australian Strategic Tenements

NMDC has expanded its footprint globally through subsidiaries and joint ventures.

NMDC holds a 92.8% stake in Legacy Iron Ore Limited, an Australian company. Legacy recently commenced gold mining operations at the Mt. Celia project and holds tenements for exploring iron ore, base metals, and tungsten.

Financial Momentum: Analyzing the 41.6% Operating Margin

The company’s market cap is ₹79,284 crore, as of 07 May 2026.

NMDC Share Price

Over the last 5 years, net profit grew at a 13% CAGR, reaching ₹6,693 crore in FY25.

Gross operating revenue in FY25 rose by 11% year-on-year to ₹23,668 crore. The company even efficiently managed to convert this revenue to profitability.

The Efficiency Frontier: Why 41.6% Margins Matter

The company’s EBITDA (Earnings Before Interest, Tax, Depreciation and Amortisation) surged nearly 17% to ₹9,846 crore, while its operating margin expanded by over 200 basis points to reach a comfortable 41.6%.

This solid operational growth translated perfectly into the bottom line, with net profit jumping 17% to ₹6,693 crore.

Volume over Pricing: A Deep Dive into 9MFY26 Performance

NMDC has delivered a robust operational and financial performance in the 9MFY26, driven primarily by strong volume growth.

The company saw significant improvements in its core mining activities.

Iron ore production grew by 20% year-on-year to reach 36.9 MT, compared to 30.8 MT in the same period last year.

Similarly, iron ore sales volumes rose by 10% to hit 34.9 MT.

This strong physical output translated into solid top-line and bottom-line growth. NMDC’s revenue for 9MFY26 surged by 22% year-on-year, reaching ₹20,381 crore.

While overall revenues grew, the average domestic sales realization dipped slightly by 4%, settling at ₹4,992 per tonne. But the high volume of iron ore extracted and sold allowed NMDC to maintain its upward financial trajectory for the year.

The company’s EBITDA rose 5% to ₹7,666 crore. This operational growth was primarily supported by the increased volumes and healthy realizations. As a result, PAT surged by 4% to ₹5,401 crore.

Capital Efficiency at Scale

The company’s return ratios are better than the industry median. Return on Capital Employed stood at 32% (against the industry median of 16.4%) in FY25, while Return on Net Worth stood at 22.6% (14.7%).

The company generates exceptionally high returns on invested capital in its operations. In FY25, the RoIC was recorded at 46.3%.

A company’s ability to consistently pay high dividends isn’t just about its accounting profits. It ultimately comes down to the actual cash it generates and holds. For NMDC, the cash position is a pillar supporting its payouts.

The Liquidity Cushion: Evaluating the ₹10,000 Crore Cash Reserve

NMDC maintains a highly liquid and pristine balance sheet. As of 31 March, 2025, NMDC held cash and bank balances of over ₹10,088 crore. The company generated a net operating cash flow of ₹1,894 crore in FY25, a steep decline from ₹7,394 crore in FY24.

A look at where this cash goes shows a company carefully balancing its future growth with immediate shareholder returns. In FY25, NMDC spent ₹3,230 crore on CAPEX to support its capacity expansion.

Despite this reinvestment, the company still comfortably distributed ₹2,460 crore (final dividend of FY24 and FY25 interim dividend) in cash dividends to its investors during the same year.

The Capex vs. Payout Balancing Act

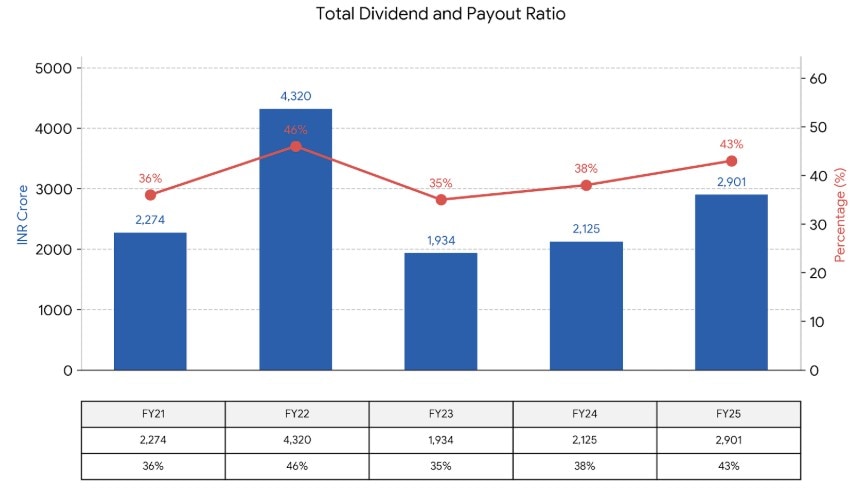

Over the past 3 years, the company’s dividend payout has been consistently increasing. In FY23, the company distributed a dividend of ₹1,934 crore (35% of PAT), which rose to ₹2,125 crore (38%) in FY24, and further increased to reach ₹2,901 crore (43%) in FY25.

This suggests the company has been increasing its dividend payout alongside the rise in PAT. This indicates that dividend payouts could sustain and even increase further as long as profitability growth stays healthy.

The Payout Paradox: Balancing Dividends with 100 MTPA Ambitions

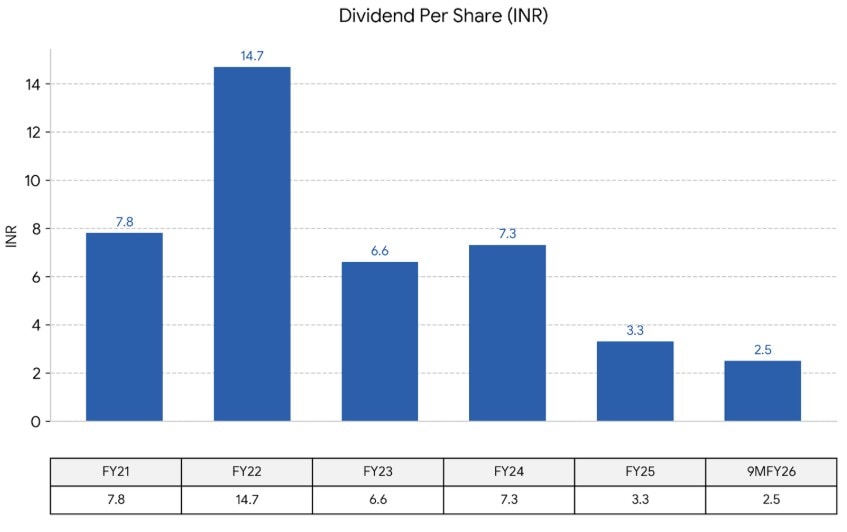

However, the dividend per share has been quite volatile. NMDC paid a dividend of ₹3.3 per share in FY25, translating into a dividend yield of 3.7% at the current share price of ₹90 as of 07 May, 2026.

In FY26 year-to-date, the company has already paid ₹2.5 per share in dividends. Prior to FY25, NMDC had paid ₹7.3 per share in FY24, ₹6.6 in FY23, ₹14.7 in FY22 and ₹7.8 in FY21.

Navratna Discipline: Why the 60% Govt. Stake Matters for Dividends

That said, because NMDC is a Navratna PSE, its dividend policy is inherently tied to its largest shareholder, the Government of India, which holds a 60.8% promoter stake.

This ownership structure ensures that the company remains disciplined in returning cash, as the government relies on these consistent dividend streams.

Project 100 MTPA: The 2030 Growth Roadmap

The management is not just sitting on its cash; it is aggressively expanding. Backed by a planned capital expenditure of over ₹70,000 crore, NMDC has set a target to more than double its iron ore production capacity to 100 MTPA by 2030. This expansion will be funded internally.

Efficiency Through Infrastructure: The 135-km Slurry Pipeline

To transport this volume of ore efficiently, NMDC is investing in cutting-edge logistics. This includes the construction of a 135-kilometer underground slurry pipeline to transport iron ore from Bacheli to Nagarnar.

Additionally, the company is supporting the doubling of the 150-kilometer Kothavalasa-Kirandul railway line. This will boost the evacuation capacity of its Bailadila sector from 28 MTPA to 40 MTPA.

Valuation Arbitrage: Is NMDC Trading at a PSU Discount?

Valuation-wise, NMDC trades at an EV/EBITDA multiple of 7.1x, at a discount to the 10-year historical median of 9x. The valuation is not just a discount to the industry EV/EBITDA (9.2) but also to local domestic peers such as Lloyds Metals (21.8), GMDC (23.5), and MOIL (11.3).

The “Dividend Hunter” Verdict: Is This a Long-Term Income Fortress?

NMDC meets the key Dividend Hunter filters. It has shown profit growth, strong cash flows, and a payout ratio within thresholds.

Given a yield of 3.7%, consistent increases in cash flow, a government-owned PSE, and a historical dividend payout track record, it appears likely that the dividend payout trend will continue.

Dividend hunters should add this stock to their watchlist and see if it sustains its lucrative dividend yield.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data were unavailable have we used an alternative, widely accepted, and widely used source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.