If you have followed Sunil Singhania, you know the man rarely buys what is already in fashion. The Abakkus Asset Management founder built his name at Reliance Mutual Fund hunting for businesses the rest of the market had not yet bothered to read about. So, when his March 2026 quarter filings showed six brand new entries, it was hard to ignore.

The fresh additions add up to roughly Rs 322 cr and sit across the Abakkus Flexi Cap Fund, the Growth Funds II, and the Four2Eight Opportunities Fund. The list includes a 30-year-old dairy company, a glass maker that came out of NCLT, a fashion retailer that has been called a show-me story for years, two electronic manufacturing services (EMS) firms that have been hammered in the recent sell-off, and a freshly listed MSME lender that the IPO market possibly rejected.

There is no AI theme here. No defence stock. No semiconductor name. Singhania appears to be doing what value investors are paid to do in expensive markets, which is to buy disappointment.

According to data filed for the March 2026 quarter, the Abakkus portfolio’s overall net worth was a little over Rs 2,740 cr. Let us dig in to see if these new entries are the noise of a gainful run or deliberate redeployment in a tougher tape.

#1 Heritage Foods: Scaling Value-Added Products Amidst Margin Pressure

Singhania’s Abakkus Flexi Cap Fund picked up 12,98,704 shares, or a 1.4% stake, in Heritage Foods Ltd. The stake is valued at around Rs 47 cr.

Incorporated in 1992, Heritage Foods is a Hyderabad-based dairy and FMCG company that runs three core businesses: dairy, renewable energy, and animal feed. Dairy is the engine. The company sells milk, curd, ghee, butter, paneer, flavoured milk, and ice creams.

It is owned by the family of Andhra Pradesh Chief Minister N. Chandrababu Naidu, with his son Nara Lokesh on the board. The current market cap is around Rs 3,384 cr. Promoter holding stands at 41.3%.

The stock has cracked nearly 26% on a year-to-date basis in 2026. That sets up the opportunity. The recent operating numbers, on the other hand, tell a more complicated story.

| Fiscal Year | FY20 | FY21 | FY22 | FY23 | FY24 | FY25 |

| Sales (Rs Cr) | 2,726 | 2,473 | 2,681 | 3,241 | 3,794 | 4,135 |

| EBITDA (Rs Cr) | -382 | 261 | 186 | 132 | 203 | 326 |

| Net Profit (Rs Cr) | -169 | 148 | 96 | 58 | 107 | 188 |

FY25 was a record year as revenue of Rs 4,135 cr was the highest ever, up 9% over FY24. EBITDA jumped 58% year on year. Net profit jumped 77% to Rs 188 cr. The big driver was Value Added Products (VAP), which include ghee, butter, paneer, and curd. VAP now contributes around 40% of total revenue.

Q3 FY26, however, took some of the shine off. Revenue grew 9% to Rs 1,119 cr but EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) margin contracted by about 122 basis points because milk procurement costs rose 6.3% while realisations rose only 4.5%. Net profit grew a modest 4%. The company is also ramping up an ice cream facility and acquiring a majority stake in its joint venture with France’s Novandie.

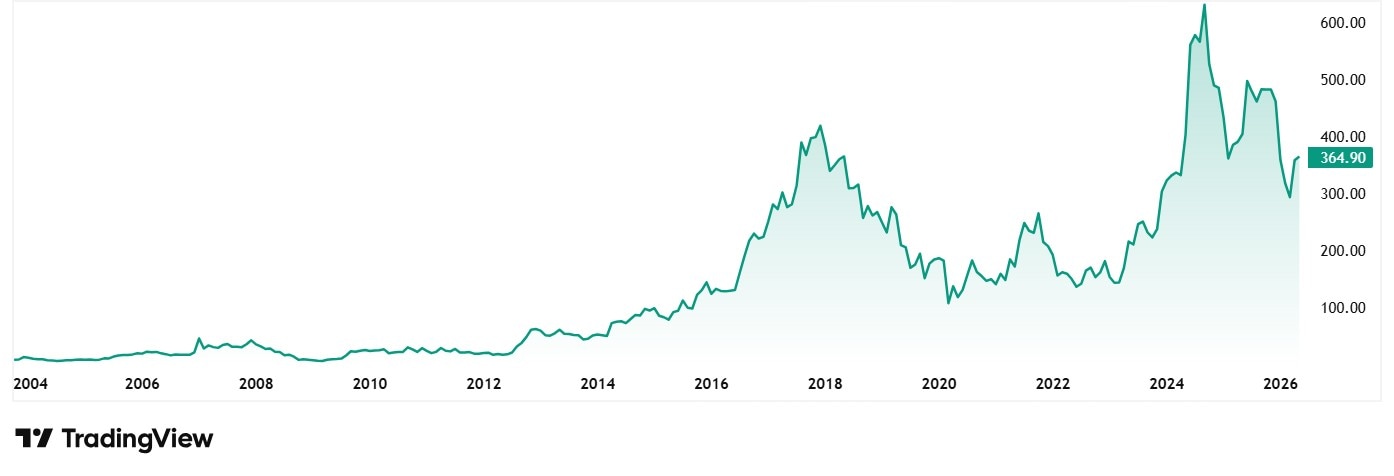

The share price of Heritage Foods was around Rs 177 in May 2021 and as on closing of 7th May 2026 it was Rs 365, which is a jump of 106% in 5 years.

As for the valuations, the share is trading at a PE of 21x and the industry median currently is 26x. The 10-year median PE for Heritage foods is 25x, which is same as the industry median for the same period.

The strong VAP shift is a pull factor, a recognised consumer brand, low debt, and a stock that is down 26% in 2026. The drag however is the lumpy milk pricing, working capital tied up in the dairy supply chain, and inconsistent return on equity. ICICI Securities and ICICI Direct currently have a ‘hold’ rating.

For Singhania, this looks like a classic buy the bad quarter entry on a brand-led FMCG name with operating leverage just starting to show.

#2 Sejal Glass: A Post-NCLT Turnaround with Middle-East Tailwinds

Singhania’s Abakkus Growth Funds II picked up 5,00,000 shares of Sejal Glass, a 4.4% stake worth around Rs 38 cr. This is the highest stake percentage among all six new entries.

Sejal Glass, incorporated in 1998, is the flagship of the Sejal Group. The company processes architectural glass in five forms: tempered, laminated, insulated, fire-rated, and bullet-proof. It came out of the NCLT process a few years back.

Since then, the management has focused on operational discipline, capacity utilisation, and exports to the Middle East. The current market cap is around Rs 924 cr. Promoter holding stands at 70%.

The financials show an aggressive growth phase.

| Fiscal Year | FY21 | FY22 | FY23 | FY24 | FY25 | FY26 |

| Sales (Rs Cr) | 10 | 24 | 46 | 164 | 244 | 396 |

| EBITDA (Rs Cr) | -3 | -1 | 3 | 20 | 34 | 61 |

| Net Profit (Rs Cr) | -18 | 147 | 8 | 3 | 11 | 29 |

In FY26, net sales jumped 62.8% year on year to Rs 396.5 cr. Profit before tax grew 171.7% to Rs 31.62 cr. Profit after tax jumped 162.2% to Rs 28.74 cr. Net cash from operating activities turned positive at Rs 51 cr in FY26 versus a Rs 5.7 cr outflow in FY25. International revenue contributed 74% of the FY25 mix, with the Middle East driving most of it.

Q4 FY26 was the standout quarter. Net profit rose 198.9% year on year to Rs 11.33 cr. Revenue grew 69.5% to Rs 114.55 cr. The stock hit the 5% upper circuit on the day of the result. Management has guided for a minimum 25% revenue growth for FY27, with margin expansion expected from fire-rated and bullet-proof glass by Q3 FY27. Railway-grade glass approvals have come through and supply has started.

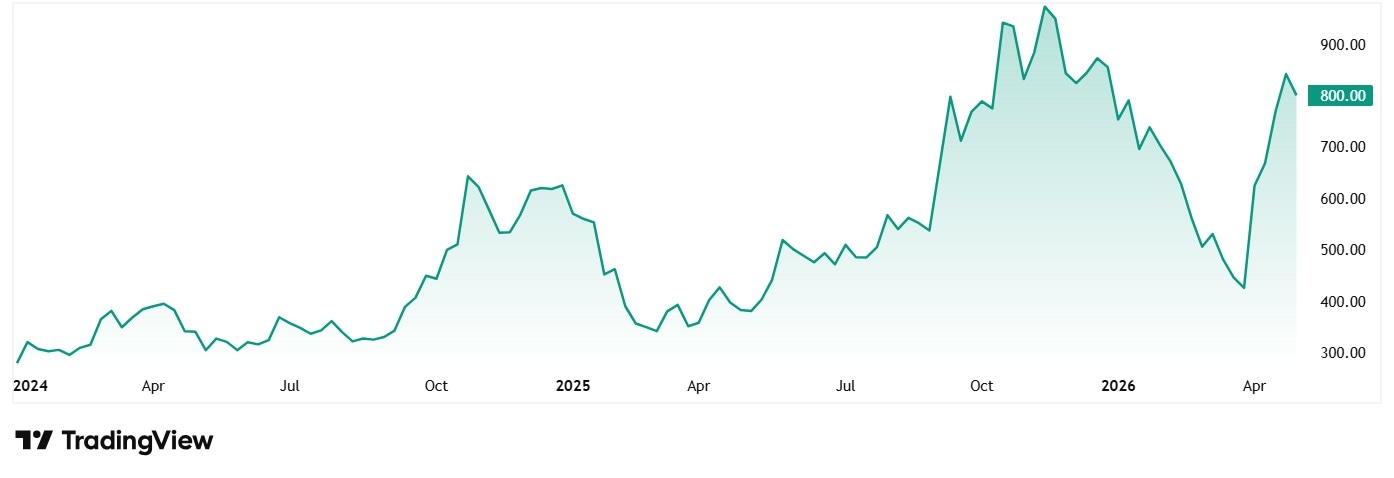

The share price of Sejal Glass Ltd was around Rs 16 when listed in December 2021 and as of closing on 7th May 2026 it was Rs 802, which is a jump of 4,912% in a little over 4 years.

However, this jump originates from a deep-value recovery following its Corporate Insolvency Resolution Process (CIRP). This performance includes the one-time structural re-rating that occurs when a company successfully exits NCLT and resumes operations under new management. Such returns are a function of a near-zero distressed base and are considered non-replicable organic growth.

Regarding the valuation, the company’s share is trading at a PE of 31x, while the current industry median is 39x.

The stock trades at around 28 times book value. Promoter holding has fallen 20.5% over the last three years, which is worth watching. The 5-year revenue CAGR on screener reads as a striking 128.7%, but most of that is base-effect recovery from the NCLT period.

Still, a 4.4% stake from Singhania in a sub-Rs 1,000 cr market cap company is a strong signal. The play is a fire-rated and bullet-proof glass story riding on real estate, infrastructure, and railway tailwinds, but only if the operating discipline holds.

Apart from these two big buys, Singhania also added 4 more stocks to his portfolio as per the exchange disclosures.

#3 Arvind Fashions: Premium Retail Bet Ready for a Re-rating?

Through the Abakkus Flexi Cap Fund, Singhania picked up 13,70,717 shares of Arvind Fashions. That is a 1.03% stake worth around Rs 62 cr.

Arvind Fashions houses a portfolio of well-known brands. These include US Polo Assn., Tommy Hilfiger, Calvin Klein, Arrow and Flying Machine. It is the apparel retail and licensing arm that was demerged from Arvind Ltd. The market cap is around Rs 6,070 cr. Promoter holding stands at 35.1%.

#4 Avalon Technologies: The High-Conviction EMS Play

Abakkus picked up 7,74,840 shares of Avalon Technologies. That is a 1.16% stake worth around Rs 81 cr. This is the largest of the six new positions in absolute rupee terms.

Avalon Technologies is one of India’s leading fully integrated EMS companies, with end-to-end operations spanning PCB design, assembly, box-build, and component design. The company has 12 manufacturing units across the US and India. The customer mix runs across industrials (35%), mobility (27%), clean energy (19%), communication (9%), and medical and others (10%). Market cap stands at around Rs 7,614 cr. Promoter holding is 44.4%.

#5 Client DLM: A bet on Aerospace and Defence visibility

Singhania’s Abakkus Flexi Cap Fund picked up 15,50,841 shares of Cyient DLM. That is a 1.95% stake worth around Rs 58 cr.

Cyient DLM is the EMS subsidiary of the Cyient group, with a focus on aerospace and defence (A&D), medical, industrial and rail segments. The market cap is around Rs 3,153 cr. Promoter holding stands at 52.1%.

The stock has seen a correction of 11% in 12 months and is well below its highs. For Singhania, this is the classic post-correction entry into a small-cap EMS name with a clear FY27 recovery thesis.

#6 Aye Finance: The IPO Reject Play

Singhania’s Abakkus Four2Eight Opportunities Fund bought 27,13,240 shares, or a 1.10% stake, in Aye Finance in February 2026. The stake is valued at around Rs 37 cr.

Aye Finance is a Gurugram-based NBFC focused on lending to micro-scale MSMEs, the borrowers that traditional banks largely ignore. Average ticket size is around Rs 1.8 lakh. The company serves over 5.86 lakh customers across 18 states and three union territories. Backed by global investors including Google’s CapitalG, LGT Capital, A91 Partners and British International Investment, it ran the most distinctive of the recent NBFC IPOs.

The IPO is the story. Aye Finance opened on Feb 9, 2026 with a price band of Rs 122-129. The Rs 1,010 cr issue closed at just 1.04x subscribed, the weakest of the entire 2023-26 NBFC listing wave. QIBs put in 1.62x, but retail (0.81x) and HNI (0.05x) stayed away. The stock listed on Feb 16, 2026 around the issue price and has traded sideways since.

Will These 6 ‘Unloved’ Small-Caps Deliver Alpha by 2027?

Step back from the individual names and a pattern emerges. Five of the six are trading well below their recent highs. Four of the six have just completed or are recovering from a difficult quarter. Three of the six (Sejal Glass, Cyient DLM, Aye Finance) had specific events such as a turnaround, a weak quarter, or a weak listing, that pushed sentiment lower. None of them is in a hot theme.

Singhania’s fresh buys are consistent with the Abakkus value-investing playbook. Buy disappointment, size positions modestly and let the catalyst play out over a few quarters rather than days.

Whether all six work is a different question. The setup, however, is what value investors are paid to recognise. These are high-quality businesses, with visible recovery levers, available at prices the rest of the market is not interested in paying.

Adding these stocks to a watchlist sounds like a good idea, as the next few months are when the thesis will get tested.

Disclaimer: Note: We have relied on data from www.screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information. The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article. The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary