India’s textile sector is entering a new growth phase, driven by a combination of trade agreements, shifting global sourcing patterns, and capacity expansion by leading manufacturers.

The market size of India’s textile sector has increased from Rs 4.9 tn in 2010 to Rs 16 tn currently, and the government aims to double it to Rs 33 tn by 2031.

Exports, particularly, are expected to play a major role. The Ministry of Textiles has set an ambitious goal of achieving Rs 9 tn in exports by 2030 from Rs 3.2 tn in FY26.

The proposed India-UK FTA and India-EU FTA are expected to be key growth drivers for the sector. Both these FTAs could open a US$ 30 bn addressable home textile market. This would provide the sector access to one of the world’s largest apparel markets.

We discuss five textile companies that are expanding capacity, diversifying product portfolios, and strengthening their export footprint.

#1 Pearl Global Industries

First on the list is Pearl Global Industries (PGIL).

PGIL operates as a leading manufacturer and strategic supplier to prestigious global retailers across the US, Japan, Australia, and the EU.

To mitigate risks and remain competitive, they leverage a multi-country manufacturing presence across

India, Bangladesh, Vietnam, Indonesia, and Guatemala.

PGIL is on a growth trajectory, targeting revenue of Rs 60 bn by FY28, up from Rs 50 bn in FY26. To support its FY28 vision, PGIL aims to scale its existing capacity of 100 million (m) to between 125-130 m pieces, shipping roughly 100 m pieces annually.

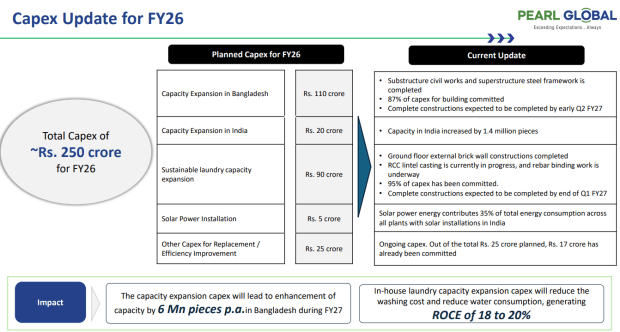

It committed around Rs 2.5 bn in capex during FY26 and is outlining a further capital commitment of Rs 2-2.5 bn for FY27 to build capabilities.

Source: Q4FY26 Investor Presentation

The company is investing Rs 1.1 bn to expand its capacity in Bangladesh. Ongoing construction of two new units (washing and stitching) is slated for completion in H1FY27. This will add approximately 6-7 m of pieces to the annual capacity.

PGIL is seeing strong customer traction and an 80% capacity utilisation at the Vietnam plant. As a result, it’s in the advanced stages of acquiring a land parcel for a greenfield project. This expansion aims to transition more production from partner factories to in-house facilities.

Following a ramp-up phase, capacity utilization at the Indonesian hub grew from 39% to 47%. Further ramp-up could aid top-line and bottom-line growth.

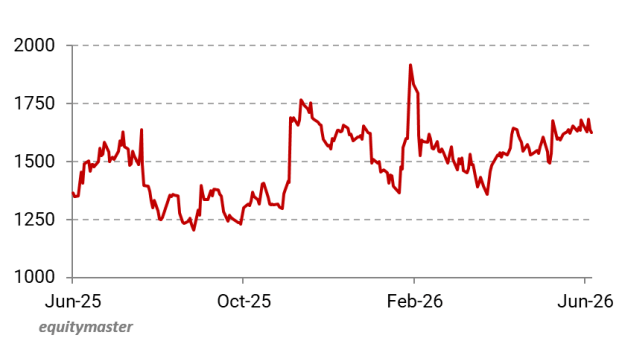

Pearl Global Share Price – 1 Year

Source: Equitymaster

PGIL has increased capacity in India by 1.4 m pieces. It’s currently ramping up its new factory in Bihar.

Additionally, it aims to increase its ‘wallet share’ with existing global brands and onboard marquee clients, particularly in Japan.

An earnings trigger for PGIL is the transition to an EBITDA margin of 10-12%, beginning in FY27. In-house laundry operations and the turnaround of its Guatemala facility, which is expected to reach breakeven in FY27, should support margin expansion.

From a financial perspective, revenue grew 11.5% to Rs 50.3 bn in FY26. Adjusted EBITDA grew 14% to around Rs 4.7 bn with margins at 9.3%. Net profit surged 17% to Rs 2.7 bn.

Note that almost every textile company’s financials were muted in FY26 due to the US tariffs.

#2 Welspun Living

Second on the list is Welspun Living.

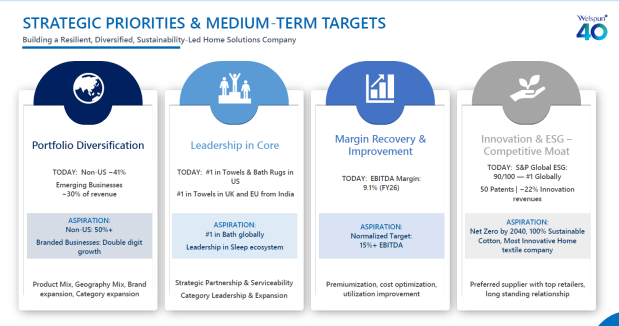

Welspun Living (WLL) is a global leader in the home textiles industry. WLL maintains partnerships with top global retailers and exports its products to over 60 countries.

Home Textiles is the company’s largest division, accounting for roughly 92% of its revenue in FY26. WLL is a leading global supplier of towels, bath rugs, and sheets. WLL’s presence also spans advanced textiles and flooring solutions.

To capture demand, WLL is making targeted capital investments while maximizing existing capacities. The company’s Ohio facility (US) is currently operating at 60% utilization. WLL invested US $13 m in a new Greenfield pillow plant in Nevada with a capacity of 4.5 m pieces on 31 March 2026.

It plans to double its pillow business revenue from US$ 27.5 m in FY26 to approximately US$ 60 m in FY27.

WLL is also aiming to achieve Rs 10 bn in flooring revenue, up from Rs 7.4 bn in FY26. Increasing demand for high-margin (20%+) soft flooring products across the commercial and hospitality segments will drive this growth.

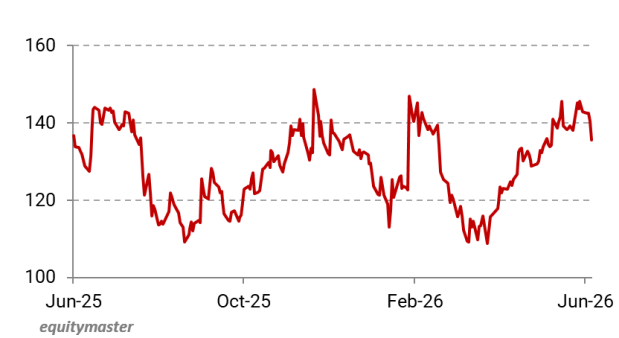

Welspun Living Share Price – 1 Year

Source: Equitymaster

The company is also expanding its flooring business in Australia and New Zealand, which could provide an additional growth lever for the segment.

While FY26 faced utilization pressures, WLL expects capacity utilization across its core towel, sheet, and bath rug segments to rebound to above 86% in FY27.

With its currently optimized capacities, WLL estimates a peak revenue potential of around Rs 120 bn.

It aims to push its non-US revenue contribution from the current 41% to over 50% in the medium term.

In India, management anticipates consistent growth of 26-30%. The company aims to scale its domestic consumer brand portfolio (Welspun and Spaces) toward the Rs 10 bn mark, up from Rs 6.6 bn in FY26. The portfolio now accounts for 19.3% of total revenue.

From an earnings perspective, it expects margin expansion and strong cash flow generation following the reduction in US tariffs.

The company expects FY27 EBITDA margins (current 9.1%) to advance into the “teens”. Their normalized medium-term aspiration is to restore EBITDA margins to 15% or higher.

Source: Q4FY26 Investor Presentation

ROCE also dipped to 5.6% in FY26. Management has guided ROCE to exceed 15% over the next three years, driven primarily by an asset-light growth strategy.

Another key development could be achieving net debt zero by FY27. WLL’s free cash flow stood at Rs 9.6 bn in FY26. This allowed WLL to reduce its net debt by 52% to Rs 7.7 bn.

From a financial perspective, total income declined 11.5% to Rs 94.7 bn in FY26. EBITDA declined 40.6% to Rs 8.6 bn with margins at 9.1%. Net profit dropped 68% to Rs 2 bn.

Looking ahead, management is targeting double-digit revenue growth in FY27. The planned capex is Rs 4.5 bn for modernisation, automation, and debottlenecking.

#3 Vardhman Textiles

Third on the list is Vardhman Textiles.

Vardhman operates as India’s largest vertically integrated textile manufacturer. Yarn is the backbone of Vardhman’s operations, accounting for 65% of the revenue. It’s the largest producer of yarn in India, with an installed capacity of over 1.25 m spindles.

The fabric division is the company’s second-largest segment, contributing 35% of revenue. The Indian market accounts for 56% of its revenue, while exports contribute the remaining 44%.

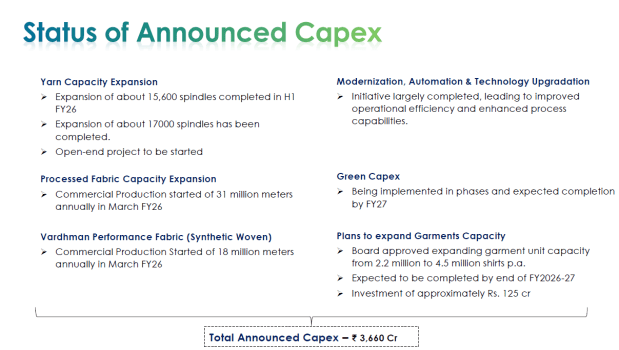

It’s expanding capacity to capture market demand. In the yarn segment, the company completed an expansion of about 15,600 spindles in H1FY26 and then an additional 17,000 spindles.

Management is also restarting an open-ended spinning project that was previously put on hold.

In its fabric division, Vardhman is diversifying and expanding. In March 2026, it commenced commercial production of an additional 31 m meters of processed fabric annually, along with an 18 m meter line dedicated to performance fabrics (synthetic woven).

This plant is expected to reach optimal capacity utilisation over the next 6-9 months. This expansion positions Vardhman to tap into the 100% synthetic fabric market, where domestic competition is limited.

To capitalize on strong relationships with existing brands and improve the cost structure of its smaller garmenting operations, it also approved an investment of around Rs 1.3 bn.

Source: Q4FY26 Investor Presentation

The garmenting segment is currently small. It plans to invest around Rs 1.3 bn to improve the business’s cost structure. The strategy is to utilise strong relationships with existing brands to scale this vertical. The investment will double the garment’s annual capacity from 2.2 m to 4.5 m shirts by the end of FY27.

To further expand its capacity, it has acquired new land in the PM MITRA Park in Madhya Pradesh.

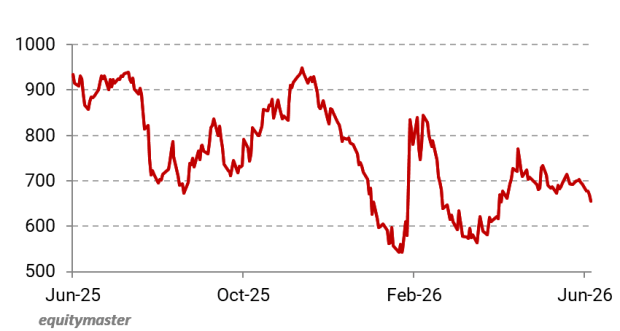

Vardhman Textiles Share Price – 1 Year

Source: Equitymaster

The land is expected to be handed over by December 2026 or January 2027. This would allow Vardhman to begin planning its next phase of capacity expansion to meet anticipated demand.

From a financial perspective, total income declined slightly by 0.3% to Rs 99.3 bn in FY26, mainly due to US import tariffs, volatile domestic cotton prices, and geopolitical tensions. EBITDA declined 8% to Rs 14.9 bn with margins at 15.1%. Net profit dropped 16% to Rs 7.4 bn.

Looking ahead, management expects better performance in FY27, driven by a 40-50% expansion in yarn spreads, the alignment of Indian cotton prices with international markets, and strong export demand.

#4 Arvind

Fourth on the list is Arvind.

Arvind is a diversified manufacturing enterprise whose core operations are divided into two primary segments: Textiles and Advanced Materials.

In the textiles and garments, the company is a major producer of denim and woven fabrics. The segment contributes 74.1% to revenue. The remaining comes from advanced materials.

Strategic international acquisitions, capacity expansions, and favorable sector-specific demand drive the company’s expansion strategy.

A key part of Arvind’s growth strategy is the acquisition of a 61% stake in US-based Dalco-GFT. The acquisition gives Arvind a presence in a US $2.5 bn market across multiple product segments. Achieving a similar scale, customer base, and market access on its own would have taken several years.

It also provides Arvind with manufacturing facilities in North and South Carolina, bringing production closer to customers in the US.

The Dalco-GFT acquisition is both margin and EPS-accretive at the consolidated Arvind level. It generates a 17% EBITDA margin and previously achieved a 40% Return on Capital Employed. Arvind aims to accelerate the business growth rate at 15%+ from the historical growth of 10%.

To achieve this, Arvind plans to invest US$ 5 m annually in Dalco-GFT to add one new manufacturing line per year. This capacity expansion would resolve the capacity bottleneck.

Arvind Share Price – 1 Year

Source: Equitymaster

The US facilities are currently operating at around 85% capacity, leaving room for further expansion. The plants also have enough space to add three more production lines, ensuring that capacity is unlikely to be a bottleneck as the business grows.

On the domestic front, Arvind intends to invest Rs 4.5-5 bn in FY27 in its garmenting and advanced materials divisions. This will be funded entirely by its free cash flow.

The garmenting division continues to be a growth engine. It recently crossed the milestone of producing over 10 m pieces for the third consecutive quarter and surpassed Rs 20 bn in annual revenue.

From a financial perspective, total income grew by 12% to Rs 93 bn in FY26. EBITDA grew 15% to Rs 10.6 bn with margins at 11.4%. Net profit grew 21% to Rs 4.4 bn.

#5 Gokaldas Exports

Fifth on the list is Gokaldas Exports.

Gokaldas is a leading apparel manufacturer that designs, develops, and exports a range of clothing for all seasons. It has an annual production capacity of 87 m pieces.

In FY26, North America was the dominant end-market at 77.9%, followed by Asia at 12.2% and Europe at 9.3%. The company is strategically pivoting its product mix to capture higher-value segments.

It successfully onboarded four new premium brands (two for India operations and two for Africa), which will begin contributing to revenues in FY27.

To sustain an expected growth rate of minimum 15%, it’s continuously scaling its physical infrastructure and improving operational efficiency.

Following recent capacity additions, the company’s manufacturing capacity is poised to reach 104 m pieces, comprising about 52 m pieces in India and 40 m pieces in Africa, with additional expansions.

A manufacturing unit in Karnataka (Kolar Gold Fields) is currently ramping up and will hit full capacity in H1FY27. This will add about Rs 1.3 bn to revenues.

Gokaldas Exports Share Price – 1 Year

Source: Equitymaster

Concurrently, a new plant in Bhopal is expected to reach full capacity by Q3FY27, adding about Rs 1.8 bn to the top line.

Beyond its ongoing expansion, it may greenlight two new factories with a planned capital expenditure of Rs 0.8-1 bn over two years. These facilities are expected to add around Rs 3 bn to revenue by FY28.

In the overseas market, physical capacity expansion in Africa was largely completed last year. It now plans to drive output by introducing a second shift. The African business is also showing signs of revival.

A major growth driver could be Gokaldas merger with Bombay Rayon (BPTL). The merger is expected to conclude in Q3FY27 and will add significant scale.

BTPL has a current capacity of 7 m meters of fabric, which can be scaled up to 10 m of fabric. Its current capacity utilisation is approaching 5 m meters. BTPL revenue is expected to cross Rs 10 bn in FY27.

EBITDA break-even is likely in H1FY27, with margin projected to reach 12% by FY28 and 14% by FY29.

From a financial perspective, total income grew 4% to Rs 40.7 bn in FY26. EBITDA grew 2% to Rs 4.3 bn with margins at 10.7%. Net profit declined 37% to Rs 1 bn due to geopolitical headwinds.

Bottom line

The next phase of growth in India’s textile sector is unlikely to be driven by industry tailwinds alone.

It will depend on which companies can convert capacity additions, new customer wins, acquisitions, and margin initiatives into sustainable earnings growth.

The five companies on this list have laid out some of the most visible expansion plans in the sector. The key question now is not whether opportunities exist, but who can execute best.

On the risk side, the heavy reliance on the US market remains a key concern, as any increase in tariffs could affect export growth and profitability.

Thus, instead of relying solely on hype, investors need to carefully analyse the company’s fundamentals, including financial performance, corporate governance practices, and growth strategies.

Happy investing.

Disclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such. Learn more about our recommendation services here…

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary