In 2010, TEIL demerged its steam turbine division into Triveni Turbine Limited (TTL).

TTL was listed in late October 2011 and shortly thereafter dropped to Rs 40 per share. Today it trades at Rs 1,590 per share, a price return of nearly 30% CAGR over 15 years.

Today TTL’s market cap is ₹18,000 crore, nearly double TEIL’s own ~₹9,200 crore. The spun-off child outgrew the parent. This is the kind of enviable outcome every special situation investor hopes for when investing in a ‘demerger’ play.

Of course, few are as successful as TTL but when the same entity that birthed TTL is also de-merging another entity one must pay attention.

Why Demergers create value

When a company houses multiple businesses under one roof: a cyclical sugar operation alongside a high-margin engineering business, for examples, the market struggles to value it properly.

Fund managers who want exposure to engineering business don’t want a sugar stock. Sugar analysts don’t know how to value gearboxes. The result is a blended, middling valuation that undervalues the better business. This is the conglomerate discount.

A demerger forces the market to price each business independently. Separated entities attract sector-specific investors and analysts, management gets dedicated focus and capital allocation, and each business pursues its own strategy unshackled from the other’s cycle.

The discount evaporates, usually. The mechanism works best when the businesses being separated have contrasting profiles such as different growth rates, margins, capital needs, and investor bases.

India’s recent demerger wave illustrates this well.

ITC demerged its hotel business in January 2025, a division consuming ~20% of capital while contributing just 3-4% of operating profits. ITC Hotels debuted at ~₹42,000 crore as an independent company, while ITC itself saw improved return ratios as a purer FMCG play.

Reliance demerged Jio Financial Services in 2023; it has appreciated ~36% since listing.

Raymond’s stock nearly doubled in 2024 backed by an impending demerger and improving performance in underlying businesses.

In the special situations space, the Greenply-Greenpanel demerger (2019) is a textbook case.

Greenply demerged its MDF business into Greenpanel in 2018 at a 1:1 ratio. Greenpanel rallied over 5x from its listing price within two years, validating the demerger thesis. Although, like any cyclical business, it has since given back some of those gains

The pattern is consistent. Give a focused, high-quality business its own identity, its own management attention, and its own investor base, and value tends to surface sooner or later.

Why Triveni power transmission business demerger Makes Sense

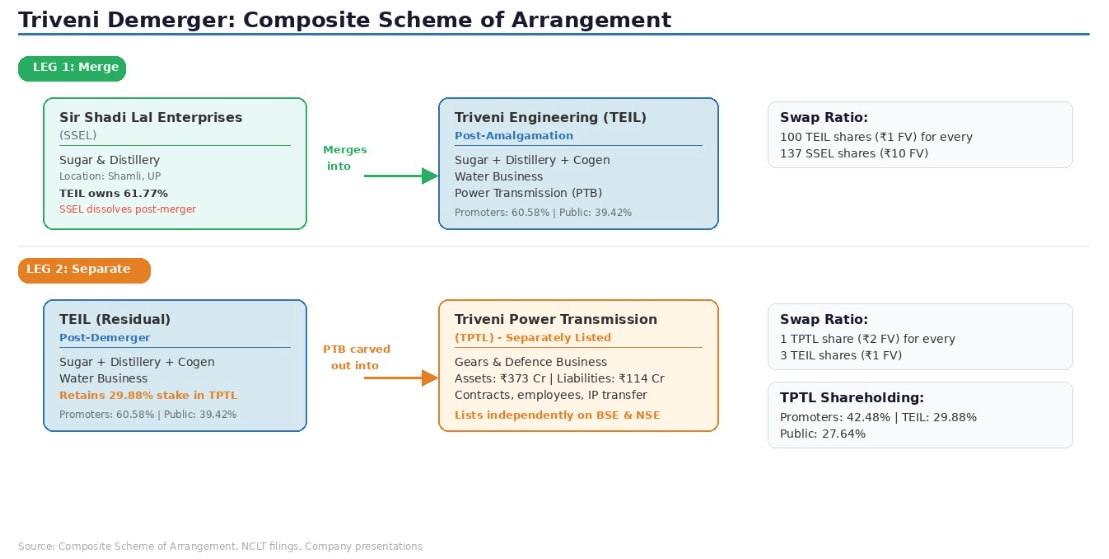

TEIL is currently in the process of merging its sugar subsidiary SSEL into itself, then carving out its Power Transmission Business (gears + defence) into a new company called Triveni Power Transmission Limited (TPTL).

If you hold 300 TEIL shares on the record date (not finalised yet), you keep all 300 TEIL shares (now a purer sugar + distillery + water company) and receive 100 TPTL shares (the gearbox and defence business) directly in your demat account.

No cash changes hands. You simply end up owning two separately listed companies instead of one. Before we get into the mechanics and valuations, let’s understand WHY it makes sense to demerge the PTB – power transmission business.

The three reasons why separating the Power Transmission business makes sense now.

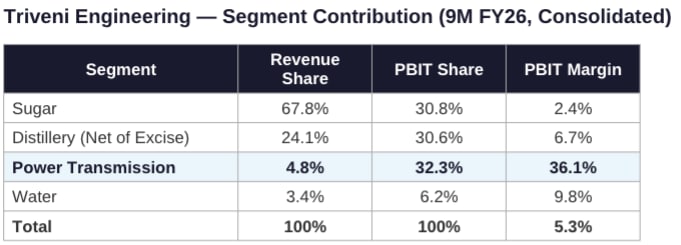

#1 The power transmission business (PTB)

In 9MFYF26, PTB contributed just 5% of Triveni’s revenue but punched at 31% of consolidated pre-tax profits.

Sugar and distillery together made up 92% of revenue but only 62% of profits. When one business runs at 34% PBIT margins and the other swings between negative and single digits depending on the monsoon, the market doesn’t know what multiple to assign.

#2 PTB has reached escape velocity

Five years ago, PTB was a ₹154 crore revenue division. Today it’s at ₹370 crore with a ₹700 crore capacity buildout completing by September 2026, a defence facility commissioned, a Swiss subsidiary for European expansion, and AVL approvals from every major global OEM. It’s no longer a small division that needs the parent’s balance sheet, it’s a business that needs its own identity, its own capital allocation, and its own investor base to attract the kind of valuation its growth profile deserves.

#3 The sugar and distillery businesses are cyclical and they’ll drag PTB’s valuation down if they stay together

Ethanol overcapacity is real (industry capacity of 2,300+ crore litres against around 1,050 crore litres of demand). Sugar remains hostage to government pricing and the MSP (Minimum support price) hasn’t been revised since 2019 despite cane costs rising every year. If PTB stays inside this structure, every bad sugar quarter pulls down the stock, and every policy uncertainty around ethanol clouds the market’s view of what is fundamentally a globally competitive precision engineering business. Separation protects PTB’s valuation from noise it has nothing to do with.

Zooming in on PTB – the hidden gem

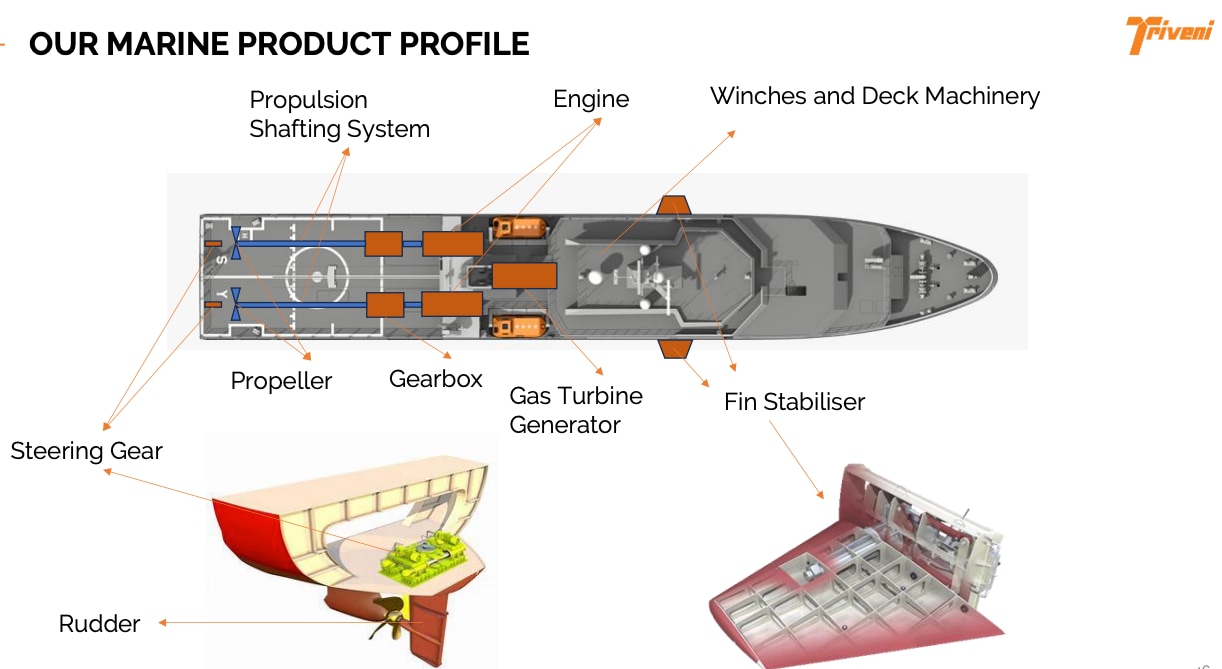

Triveni’s Power Transmission Business, based in Mysuru, has been manufacturing high-speed gears and gearboxes since 1976.

These are precision-engineered, made-to-order products that go into steam turbines, gas turbines, compressors and pumps, powering everything from oil refineries to steel plants to naval vessels. With over 12,500 installations across 80+ countries, Triveni is the largest player in this space in India, South Asia and Southeast Asia.

What makes PTB hard to replicate is a combination of cost, speed and credibility.

On the Q3 FY26 concall, Vice Chairman Tarun Sawhney noted that Triveni’s manufacturing costs are 25 to 30% cheaper than European competitors, while delivery timelines run at 6 to 8 months versus 12 months or more for EU peers.

Over the past two years, the business has been qualified as an approved supplier by virtually every major global OEM in its space, including Siemens, MAN Energy Solutions, Mitsubishi, Atlas Copco and Doosan.

In just the first nine months of FY26, Triveni added 11 new OEM customers globally. Once you’re on these approved lists, you get access to recurring global order flow. That’s a moat that takes years to build and is very difficult to dislodge.

The defence piece adds a layer of long-term optionality. Triveni is an indigenous supplier of marine propulsion gearboxes for the Indian Navy and Coast Guard. A new multi-modal defence manufacturing facility in Mysuru (the first of four planned bays, with Board-approved capex of over ₹100 crore) was commissioned in December 2025.

The product scope is broad: fin stabilisers, propulsion shafting for surface ships and submarines, deck machinery, gas turbine enclosures under a 10-year agreement with GE Aerospace, and a recently signed MOU with Rolls Royce for marine gas turbine generators for next-generation Navy vessels.

The long-duration order book stands at roughly ₹185 crore, of which approximately 80% is defence. Management has indicated they are now looking beyond the Navy to other branches of the armed forces.

Internationally, the groundwork for expansion has already been laid inside TPTL. Before the demerger, TPTL acquired a Swiss subsidiary (Triveni Power Transmission GmbH) and opened a European sales office.

It’s export growth is being driven by compressors and gas turbine gearboxes, with the Middle East emerging as a key market. The gears manufacturing capacity is being scaled from ₹400 crore of potential revenue currently to ₹700 crore by September 2026, and that doesn’t include the defence facility.

This is the business that’s about to go on its own.

The Mechanics of How the Demerger will work

Triveni’s restructuring has two legs.

First, it absorbs its sugar subsidiary Sir Shaadi Lal Enterprises (SSEL) – 61.77% owned, into itself. SSEL shareholders receive 100 Triveni shares for every 137 SSEL shares held.

Second, it carves out the Power Transmission Business into a new company called Triveni Power Transmission Limited (TPTL), transferring all PTB assets (₹373 crore), liabilities (₹114 crore), contracts, employees and IP.

Triveni shareholders receive 1 TPTL share (₹2 face value) for every 3 Triveni shares (₹1 face value). TPTL then lists on BSE and NSE.

One important detail is that Triveni will retain a 29.88% stake in TPTL after the demerger. The parent will maintain skin in the game, much like it held 22% in Triveni Turbine after the 2010-11 demerger before selling it a decade later for ₹1,593 crore.

Where we are today

The scheme has cleared every major gate on schedule.

Board approval (December 2024), SEBI and exchange clearances (August 2025), NCLT-ordered shareholder and creditor meetings (approved December 7, 2025), and NCLT sanction (December 16, 2025).

On the Q3 FY26 concall in February 2026, Tarun Sawhney confirmed the scheme was on track for “this calendar quarter” and closed with: “The next time we speak, in all probability, this will be two separate companies.”

The remaining steps are procedural: filing the order with the Registrar, allotting shares, and applying for TPTL’s listing.

A structural detail worth understanding

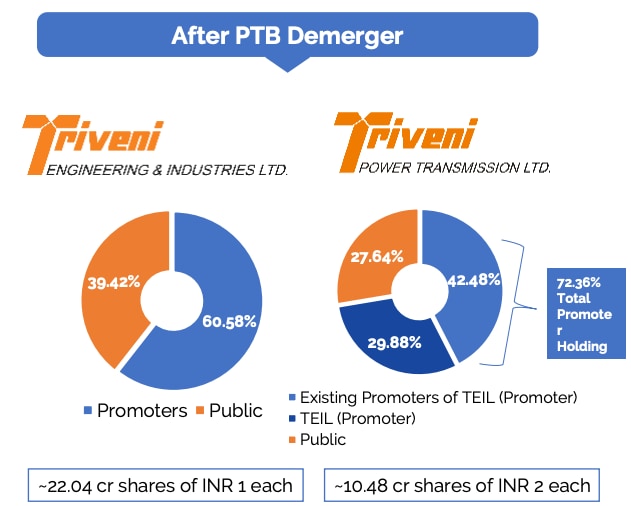

In a standard demerger, the new company’s shareholding mirrors the parent’s. Triveni’s public holds 39.42%. You’d expect them to hold roughly the same in TPTL also. They won’t.

Public shareholders will hold just 27.64% of TPTL directly, a compression of nearly 12 percentage points. So, TPTL’s post-scheme capital has two layers: existing shares (held entirely by Triveni the corporate entity, which includes public shareholders) and new shares (issued proportionately to all Triveni shareholders). Only the new shares mirror Triveni’s ownership pattern.

The net effect is that direct public shareholding in TPTL is reduced from 39.42% in TEIL to 27.64% in TPTL.

Triveni Engineering pre & post demerger public shareholding

But holding companies in India routinely trade at steep discounts to net asset value. Triveni’s 30% TPTL stake may never reflect fully in Triveni’s market price. This detail has appeared in four consecutive quarterly investor presentations. No analyst has questioned it, yet. It is a structural choice investors should understand before the record date.

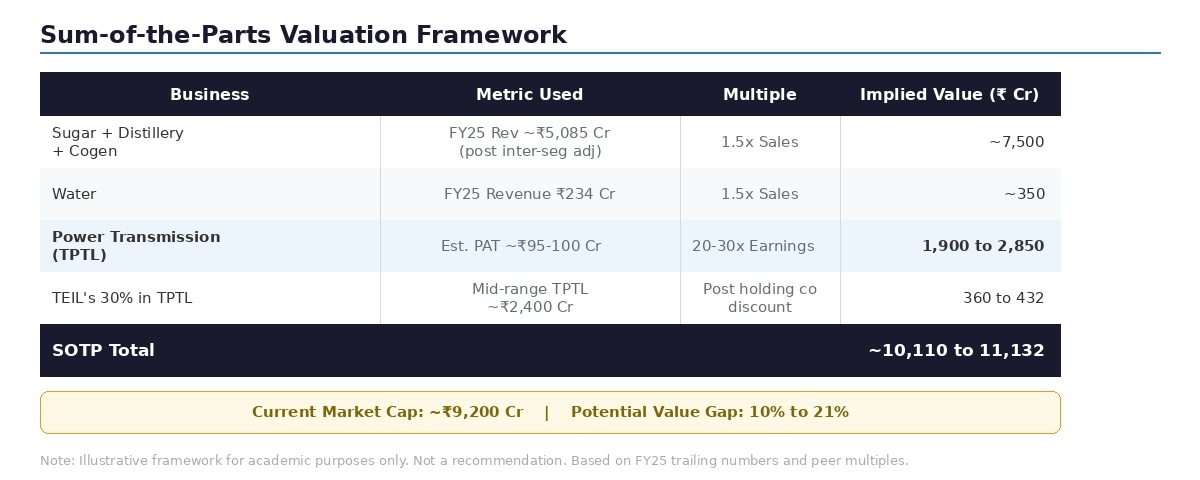

The Valuation Math. Is There Value?

A standard disclaimer before we proceed: what follows is a simple, illustrative framework using publicly available peer multiples and trailing financials. It is not a target price, not a recommendation, and not a prediction.

It is an if-then exercise to help readers think about how the market might value these businesses once they trade independently.

The logic of a sum-of-the-parts (SOTP) valuation is straightforward.

Today, the market assigns one blended multiple to Triveni’s combined ₹9,200 crore market cap. After the demerger, each business will attract its own set of investors, its own analyst coverage, and its own valuation multiple. The question is whether the sum of the parts, valued independently, exceeds the current whole.

Sugar, Distillery and Cogeneration (residual TEIL post-demerger)

FY25 revenue net of excise duty and after inter-segment adjustments for the sugar segment was ₹5,085 crore.

Indian sugar companies typically trade between 0.5x and 2.5x sales depending on where they are in the cycle. Balrampur Chini, a close peer, currently trades at 1.7x sales. However, Industry level ethanol overcapacity (not at TEIL through) hampering its pricing power and keeping margins low, the still loss-making SSEL subsidiary, and the policy dependence of both sugar and distillery justify a slightly more conservative multiple.

At current Market cap/sales multiple of 1.4x sales, which is TEIL’s 5 year median, upward bias will depend on how the prospects for sugar industry change going forward.

Water

Peers like VA Tech Wabag and Ion Exchange trade at 2.1x to 2.5x market cap to sales. Given Triveni’s smaller scale but mostly recurring (70% orderbook – O&M contracts), a conservative 1.5x seems fair.

Power Transmission (TPTL)

This is where the arithmetic gets interesting. FY25 revenue was ₹370 crore with PBIT of ₹127 crore at a 34.3% margin. Assuming a 25% tax rate, that translates to an estimated PAT of roughly ₹95 to 100 crore.

Elecon Engineering, a listed peer in the industrial gears space, trades at approximately 24x earnings. Applying a range of 20x to 30x to PTB’s estimated earnings gives an implied market cap of ₹1,900 to ₹2,850 crore for TPTL as a standalone listed entity.

Even at the conservative end, that is a significant number relative to Triveni’s current total market cap of ₹9,200 crore. And this is on trailing numbers alone, before factoring in the capacity expansion to ₹700 crore, the defence ramp-up, or the export growth from new global OEM qualifications.

TEIL’s retained 30% stake in TPTL

At a mid-range TPTL valuation of roughly ₹2,400 crore, Triveni’s 30% stake would be worth approximately ₹720 crore on paper. But this is where the holding company discount bites.

Listed Indian holding companies and parent companies with minority stakes in subsidiaries routinely trade at 40% to 60% discounts to their net asset value. Apply that discount and the market value of the stake drops to ₹360 to 432 crore. This is the practical cost of the structural choice discussed earlier.

Against a current market cap of ₹9,200 crore, the SOTP range of ₹10,100 to ₹11,100 crore suggests the stock is slight undervaluation of 10%-20%. But, this is not a screaming mispricing.

Why these estimates could prove conservative

The SOTP uses trailing FY25 numbers. Several developments could push actual values higher on both sides of the split.

On the sugar and distillery side, realisations in 9M FY26 are already running 5 to 6% above the prior year, recovery trends have improved, and production is expected to be meaningfully higher this season.

The MSP, unchanged since February 2019 at ₹31/kg, appears set for revision. Tarun Sawhney indicated on the Q3 FY26 concall that it is expected in the “high ₹37/kg bracket.”

On ethanol, blending has hit 20% and NITI Aayog is working on a roadmap for beyond E-20, with a senior cabinet minister publicly confirming 27% blending has been approved. If blending targets rise and ethanol prices are revised upward, the distillery business could see a step-change in profitability that the 1.5x revenue multiple does not capture.

But the bigger upside skew sits with PTB.

The SOTP values it on trailing earnings of ₹95 to ₹100 crore PAT. It does not account for the fact that additional gears capacity which is coming online by September 2026 has the potential to double revenue from this segment from ₹400 crore to ₹700 crores.

The defence facility is also now operational, with inquiry levels up by 75%. Eleven new global OEM customers added in nine months. Accelerating exports in compressors and gas turbines. If PTB delivers ₹450 to 500 crore in revenue over the next two to three years at similar margins, PAT could reach ₹120 to 135 crore.

Apply the same 20 to 30x range and TPTL’s implied value moves to ₹2,400 to ₹4,050 crore. At the higher end, that alone would represent nearly half of Triveni’s current consolidated market cap for a business that today accounts for under 5% of revenue. Of course, this is all based on broad assumptions.

The asymmetry is what makes demergers potentially attractive. The downside is anchored by real assets and cash flows. The upside is driven by a capital-light, high-margin engineering business entering its next growth phase.

The point of the demerger is not that the math works on day one. It is that once PTB trades independently, attracts dedicated engineering and defence sector investors, and builds its own track record as a listed company, the multiple it commands can expand well beyond the 20x to 30x range used here.

Triveni Turbine’s journey from a division buried inside a sugar company to a ₹17,000 crore standalone entity took time, but the re-rating was substantial. The question is whether history will repeat or rhyme.

Note: We have relied on data from http://www.Screener.in and http://www.tijorifinance.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

Disclaimer:

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

Rahul Rao has been Investing since 2014. He has helped conduct financial literacy programs for over 1,50,000 investors. He helped start a family office for a 50-year-old conglomerate and worked at an AIF, focusing on small and mid-cap opportunities. He evaluates stocks using an evidence-based, first-principles approach as opposed to comforting narratives.

Disclosure: The writer or his dependents do NOT Hold shares in the securities/stocks/bonds discussed in the article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.