Welcome to the latest edition of Dividend Hunter Weekly. Previously, we examined a debt-free IT Player with a 32% ROE offering 7% dividend yield, and a Public Sector Undertaking with 6% yield and zero debt. This week, we examine a business built on India’s vast regional news readership and the reach of print media.

Despite the growing influence of digital media, print media continues to play a pivotal role in India’s regional markets, particularly in the hinterlands. As a leading media company, the brand attracts a vast readership and sustains consistent advertising demand. These two factors, with its ‘asset-light’ business model, enable DB Corp to consistently distribute dividends.

DB Corp Stock: Why it Passed the 7-Point ‘Dividend Hunter’ Screen

In this context, we select stocks that can pay dividends in the upcoming quarters. We select these stocks (excluding InVITs and REITs) using a screen that meets the following broad criteria.

- Dividend yield above 2%.

- Payout ratio below 100%.

- At least one of 3, 5, or 7-year profit growth above 5%.

- Five-year average dividend greater than zero.

- The latest dividend is higher than the five-year average.

- The latest profit is at least 80% of the previous year’s profit.

- Market capitalization above ₹1,000 crore.

After Alldigi Tech and Coal India, DB Corp is the third company to meet these criteria. At current prices, the company offers an attractive 6% dividend yield (based on historical payouts). Interestingly, renowned fund manager Pulak Prasad of the famed “Nalanda Capital” holds a 9.3% stake in the company (as per the latest available information).

Let’s dig into the company to see how it is performing and whether that can give us any clues about future payouts.

Dominance in the Indian Language Media Landscape

DB Corp (DBCL) is India’s largest and most diversified media conglomerate. It is the country’s largest newspaper group and a dominant player in the Indian language media landscape.

DBCL’s operations are central to India’s information and media network, as the company connects approximately 14 crore people, translating to nearly 10% of India’s total population. Its extensive reach covers about 49% of India’s urban population and 58% of the nation’s land area.

DBCL publishes newspapers, broadcasts on radio, and operates digital platforms, offering flagship products such as Dainik Bhaskar, Divya Bhaskar, Divya Marathi, and MY FM.

The company operates a geographically diverse network with a strong presence across 14 Indian states. This extensive portfolio includes 61 newspaper editions, 211 sub-editions across 3 languages, 30 radio stations, and state-of-the-art infrastructure with 51 printing facilities.

Infrastructure Edge: The Power of 32 Lakh Copies Per Hour

Additionally, DBCL operates a printing infrastructure featuring 51 printing facilities across 12 states, equipped with 84 advanced high-speed presses and computer-to-plate (CTP) technology.

This ensures rapid, efficient, and high-quality newspaper production with an installed capacity of approximately 32.93 lakh copies per hour.

The company has set an ambitious long-term roadmap focused on digital innovation, AI-driven personalization, and leadership in Indian-language content to build for the “next billion” consumers.

Navigating a High Base: Analyzing the Q3 FY26 Financial Consolidation

The company’s market cap is ₹3,618 crore, as of 13 March 2026.

Over the last 3 years, net profit has grown at a 37% CAGR. Total revenue dipped to ₹2,421 crore in FY25, due to the high base (₹2,482 crore) of FY24. EBITDA (Earnings Before Interest, Tax, Depreciation and Amortisation) decreased by 11% to ₹627 crore, with a 26% margin. Net profit declined to ₹371 crore, compared to last year’s profit of ₹426 crore. Still, the profit is above 80% of last year’s number.

Past Financial Track Record

Further, the financials faced some pressure in Q3 FY26.

Total revenue fell by 4% year-on-year to ₹629 crore, due to a high base and state elections in the same quarter last year. EBITDA for the quarter stood at ₹159 crore, with a 25% margin. This was supported by tight cost controls and stable newsprint prices, resulting in a net profit of ₹96 crore, down by 18.6%.

Return ratios remain strong for the business. Return on Capital Employed (ROCE) stands at 21% (down from 24% in FY24), and Return on Net Worth (RONW) stands at 16.7% (down from 20.3% in FY24).

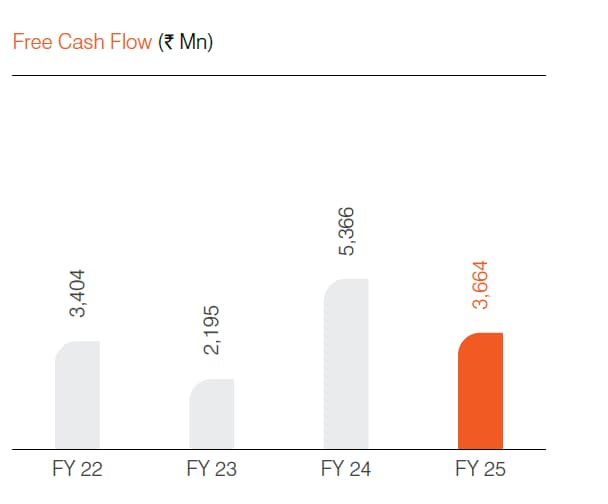

Debt-Free & Cash-Rich: Inside DB Corp’s ₹1,000 Crore Balance Sheet

The company is debt-free, with cash reserves exceeding ₹1,000 crore as of 31 March 2025. The company consistently generates strong free cash flow, which supports its ability to pay dividends. Free Cash Flow stood at ₹366 crore in FY25, down from ₹537 crore in FY24.

Free Cash Flow Trend

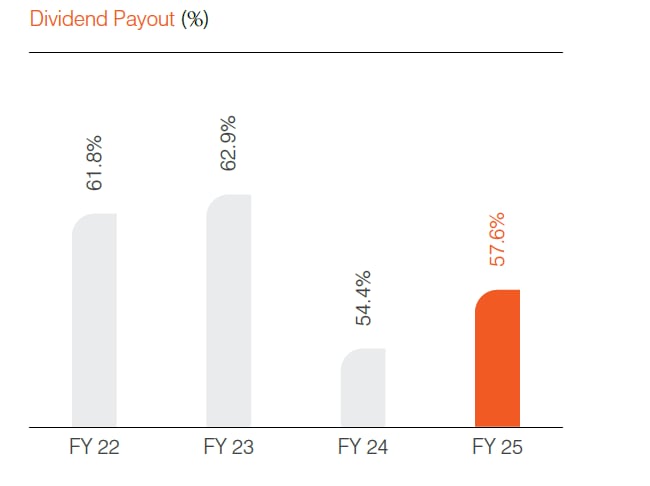

DB Corp’s Dividend Policy: Why Payouts Remain Sustainable

On the back of such cash flow, the company has already paid an interim dividend of ₹7.0 in FY26 Year-To-Date (YTD). This comprises an interim dividend of ₹5.0 per share (ex-date 24 July 2025) and ₹2.0 per share (ex-date 22 January 2026). This translates to a dividend yield of 3.5% YTD in FY26.

Dividend Payout Trend

Historically, DB Corp has consistently paid dividends each year over the last five financial years. It paid a dividend of ₹12.0 in FY25, translating into a dividend yield of 6% as per the current price of ₹203 per share. In FY24, the dividend was ₹13 per share, ₹3 in FY23, ₹6 in FY22, and ₹5 in FY21.

Collectively, in FY26 YTD, DB Corp has already paid 90% of the last 5-year average dividend. The dividend payout has consistently been less than 80%, well below the 100% threshold required by our filter.

The Dividend Payout Policy: 5% of paid-up capital

Additionally, this dividend payout policy is consistent as the company aims to distribute no more than 5% of the paid-up capital as dividends. This suggests that dividend continuity remains highly possible. Furthermore, as profitability scales, payouts could even trend higher, consistent with the company’s historical track record.

Management is optimistic regarding the underlying business momentum and profitability. It noted a gradual improvement in advertising demand as Q3 progressed, indicating growing advertiser confidence.

Going forward, DB Corp anticipates strong growth from core industries including automobiles, real estate, healthcare, banking/finance, and education. Early indicators are positive, with the automobile sector showing strong advertising spending in January 2026.

Ad-Revenue Catalysts: 26% Rate Hikes & Sectoral Tailwinds

The company’s strategy to drive ad revenue remains heavily focused on volume (expected to drive 70% of the growth), combined with slight yield improvements (30%). Furthermore, the actual revenue impact of the government’s recently approved 26% ad rate hike is expected to become visible starting in Q4 FY26.

Management’s primary focus is on growing copy numbers rather than increasing cover prices, i.e., volume-driven as compared to value-driven. To achieve this, the company is launching new readership schemes and circulation growth programs.

Additionally, government initiatives that make newspaper reading compulsory in schools in states such as Uttar Pradesh and Rajasthan can act as a regulatory tailwind for DB Corp.

Management expects newsprint prices to remain largely stable and range-bound in the near term. This pricing stability, combined with stringent cost controls and operational discipline, is expected to continue supporting the company’s healthy EBITDA margins.

The Digital Pivot: Can AI & Radio Offset Print Headwinds?

Digital remains a central growth pillar, with news apps maintaining around 210 lakh monthly active users as of November 2025. It plans to focus on reader acquisition, technology, and user experience rather than immediate revenue generation. The segment is cash-burning right now and is expected to be EBITDA positive over the next couple of years.

The company is aggressively expanding its radio footprint and expects to fully operationalize 14 newly acquired radio stations by June 2026. Initially, the margin will be lower than the business’s historical range (30-40%), but is expected to ramp up to those levels over a two- to three-year timeframe.

Valuation: Is DB Corp Trading at a Discount to Peers?

Valuation-wise, DB Corp trades at a price-to-earnings multiple of 11.2X, almost in line with the 10-year historical median of 13.1X. Relative to Jagran Prakashan (8.1X) and Sandesh (6.3X), the valuation is a premium, reflecting the company’s leading position in the print media.

Is DB Corp a stock that Dividend Hunters should track?

Undoubtedly, DB Corp meets the key Dividend Hunter filters. It has a steady profit growth, strong cash flows, and a payout ratio within thresholds. With a 6% yield, higher profitability, a dividend payment mandate, and dividend continuity, dividend continuity appears possible.

However, sustainability will depend on future profitability, momentum, and net worth. Dividend hunters should add this stock to their watchlist and see if it continues to deliver a lucrative dividend yield.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data were unavailable have we used an alternative, widely accepted, and widely used source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.