The 2026 calendar has started on a defensive note. Indices have been choppy, the small-cap index has cooled off, and many fund managers are sitting on cash. So, when two of India’s most tracked investors put fresh money to work in the same narrow window, it is worth a careful look.

Mukul Agrawal has picked up a 2.7% stake in a freshly listed Lucknow EPC company. Ashish Kacholia has bought a 1.2% stake in an oilfield services firm that is finally pulling itself out of a long slump. Is this the start of a quiet small-cap value hunt as the broader market wobbles?

The picks tell their own story. Both companies feed off government-linked infrastructure spending. Both have shaky histories marked by significant improvement in recent quarters. And both are small in size but heavy on hope. One is so new that its first listing bell rang only on April 13. The other has been listed since the 1990s but is only now showing the financial discipline that long-term investors had been waiting for.

Are these textbook contrarian buys? Or are they early reads of the next leg of India’s capex cycle? Let us pull up the screener and look at each name carefully.

#1 Mukul Agrawal’s Lucknow Bet: 2.7% Stake in Safety Controls & Devices Ltd

Incorporated in 2015, Safety Controls & Devices Ltd is an EPC company that began with fire-fighting systems and has since moved into power substations of up to 400 kV and utility-scale solar plants. The company is based in Lucknow and counts state power utilities, central PSUs and renewable energy developers among its main clients. Its IPO opened on April 6, 2026 and the stock listed on the BSE SME platform on April 13.

With a current market cap of Rs 188 cr, this is a clean small-cap story. Mukul Agrawal, the founder of Param Capital, has picked up a 2.7% stake in the firm as per the post-issue exchange disclosures. The stake is worth a little over Rs 5 cr at the current price.

For a man whose disclosed portfolio is worth over Rs 7,105 cr, this is small in absolute terms. But the conviction shown in an SME-listed company priced barely above its IPO band is what investors should focus on.

Let’s not forget that SME stocks come with a warning of “Buyer Beware’, with the limitation of trading in lots and liquidity problems.

High Growth Meets the ‘EPC Trap’

The company has logged a compounded sales growth of 40% in the last 4 years, jumping from Rs 27 cr in FY21 to Rs 103 cr in FY25.

EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) tells the same story, with a compound jump of 71% in the same period, from Rs 2 cr in FY21 to Rs 17 cr in FY25, with the operating margin lifting from 7% to 17%.

Net profit followed suit. The company went from Rs 1 cr in FY21 to Rs 9 cr in FY25, growing at a compounded rate of 73%.

This is a clean doubling of margins inside four years, which suggests the order book is now made of better-priced contracts.

A quick note here. Because the company listed in April 2026, the long ten-year financial trail that one usually expects is not available on screener.in. So, a 5-year CAGR and 10-year median PE comparison cannot be drawn yet. We will come back to this point.

The ROCE for the company is 29%, while the industry median when compared to peers is just 18%. Which means for every Rs 100 the company uses as capital, it generates a profit of Rs 29, while its peers manage only about Rs 19.

The ROE is over 30%, which for a working-capital-heavy business like EPC, is noteworthy.

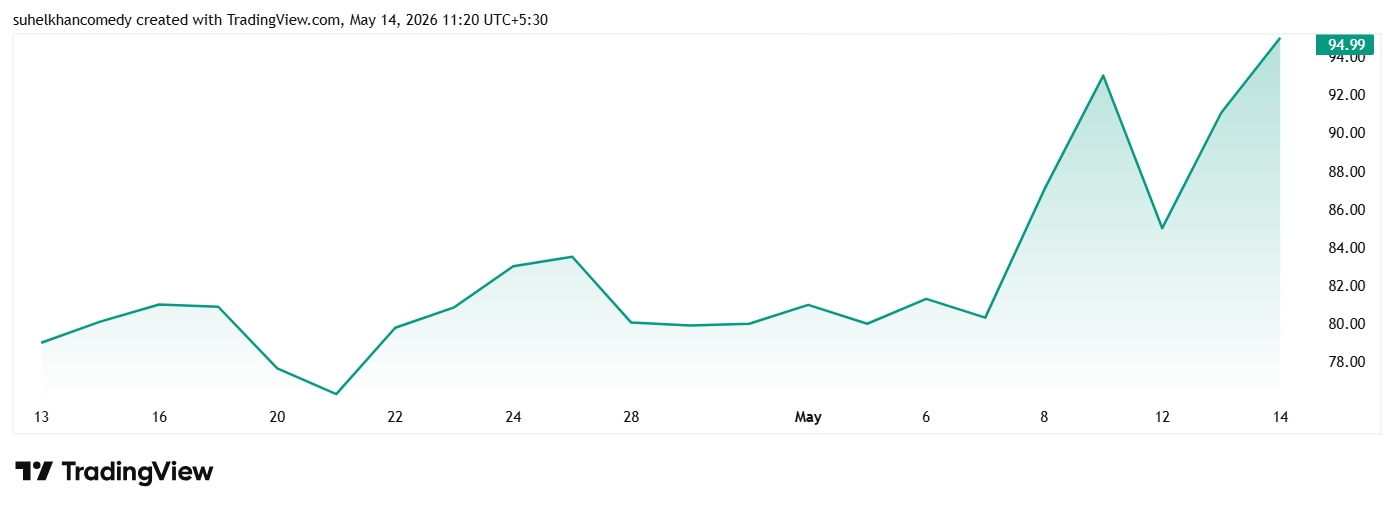

The share price of Safety Controls & Devices Ltd was Rs 79 when listed in April 2026, and as on 14th May 2026, it was Rs 95.

The stock trades at a PE of 17.6, which is at a discount to many listed civil construction peers. Since this is a freshly listed SME, the long-term 10-year median PE for the firm is not available. The peer industry currently trades closer to the mid-twenties on a price-to-earnings basis, which leaves some room for re-rating if execution holds.

Liquidity Check: The 311-Day Debtor Reality

The cash flow story is less flattering. The company has had negative operating cash flow every year since FY22. In FY25, cash from operations was a negative Rs 7 cr, even though net profit was Rs 9 cr. The reason is debtor days. As per the latest screener data, debtor days stand at 311. That means the company is waiting nearly a year on average to collect what it has billed. This is the classic EPC trap. Profits look good on paper while the actual money is stuck with clients, mostly government bodies.

Borrowings have climbed from zero in FY21 to Rs 34 cr in FY25. The company has used part of the IPO proceeds for repayment of debt and working capital, which should ease the strain.

The promoter group holds 46.4%. That is on the lower side for an SME, but the company has no pledged shares as per the latest disclosures.

Mukul Agrawal has a history of getting in early. He has done it with Bella Casa Fashion, Autoriders International and TAAL Tech, all of which were under-the-radar names when he took meaningful stakes. The Safety Controls bet has a similar flavour. Small size, government-linked order book, asset-light scaling, and a fragmented industry where execution is the moat.

The risk is straightforward. EPC stories live and die by cash collection. If the receivable cycle stretches further, even a 30% ROCE will not save the stock from a re-rating downward. But if the company can convert FY26 profits into actual cash, the upside could be steep. The FY26 figures are awaited, and most investors will be watching the cash flow line as closely as the revenue line.

#2 Ashish Kacholia’s Oilfield Re-entry: A 1.2% Stake in Asian Energy Services

Asian Energy Services Ltd, formerly Asian Oilfield Services, has been around since the 1990s. The company is one of the few in India offering an end-to-end service package for upstream oil and gas, covering land and well seismic services, reservoir imaging and operations and maintenance for oilfields. The new name reflects a wider mandate including hydrocarbon and mineral sectors.

The company’s current market cap is Rs 1,502 cr. Ashish Kacholia picked a 1.2% stake in the company via the conversion of preferentially allotted convertible warrants. Which made Kacholia among the top non-promoter subscribers. At the current market price, the stake is worth close to Rs 18 cr.

A Multi-Year Turnaround in the Gas-and-Mineral Pivot

Sales have logged a compounded growth of 11% in the last 5 years, moving from Rs 273 cr in FY20 to Rs 465 cr in FY25. But the more interesting line is the TTM (trailing-twelve-month) sales figure of Rs 668 cr, which is up 81% over FY25. The company has clearly stepped into a higher gear.

EBITDA shows the volatility one expects in oilfield services. Operating profit was Rs 67 cr in FY20, dipped to a loss of Rs 19 cr in FY23, and recovered to Rs 66 cr in FY25. The TTM EBITDA is now Rs 79 cr.

On a 5-year compounded basis, EBITDA has stayed roughly flat at low single digits. Margins have compressed from 24% in FY20 to 14% in FY25, which is the real cost of growing into a competitive contract base.

Net profit has had a similar journey. It went from Rs 29 cr in FY20 to a loss of Rs 44 cr in FY23, and back to Rs 42 cr in FY25. The 5-year compounded profit growth is just 4%. The third quarter of FY26, ending December 2025, brought sales of Rs 235 cr and net profit of Rs 18 cr, the best three-month showing in years.

ROCE for FY25 is 17%, up from 13% in FY24 and a negative number in FY23. ROE is 12.4%. These are reasonable for the sector but not eye-popping. The dividend yield is a modest 0.39%, and the payout ratio is just over 3.5% of profits over the last three years.

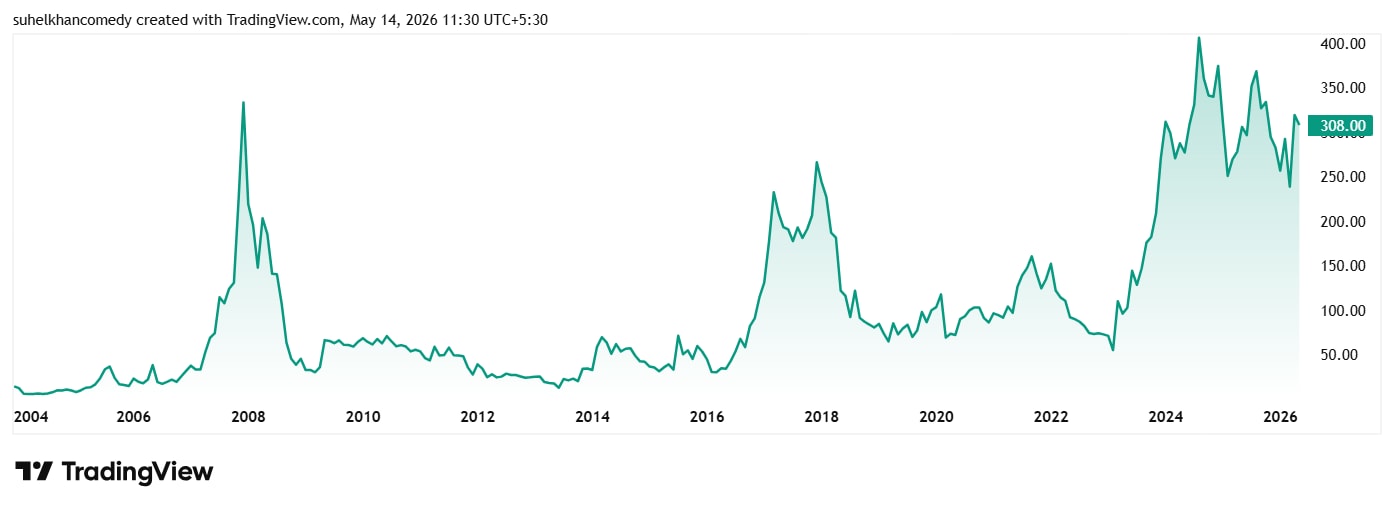

The share price of Asian Energy Services Ltd was Rs 100 in May 2021 and as on 14th May 2026 it was Rs 309, which is a 209% jump in 5 years.

The stock trades at a PE of 32x while the industry median is 13x. The 10-year median PE for the company sits closer to 24x and the industry median for the same period is 12x. So, at the current price, the stock is on the richer side of its own history.

But the long-term shareholder has not been disappointed. The 10-year share price CAGR is 24%. The 5-year CAGR is 19%, and the 3-year CAGR is a punchier 47%. So, Kacholia is buying into a stock that has rewarded patience, not chased momentum.

Kacholia is best known for spotting niche industrial and engineering plays before the market catches on. He did it with Mold-Tek Packaging, Shaily Engineering and Jain Resource Recycling. The Asian Energy bet fits the same template, with two extra layers. The first is the consolidation play, where the Oilmax merger could meaningfully expand revenue and capability. The second is the gas-and-mineral pivot, where the company is moving beyond just upstream oil into a broader resources story.

The Execution Test: What to Watch in the Next Two Quarters

Mukul Agrawal’s Safety Controls pick and Ashish Kacholia’s Asian Energy buy point in the same direction. Both investors are paying for execution that has just started to show up in the numbers. Both are buying into government-linked infrastructure demand, one through power and solar EPC, the other through oil and gas services. And both are willing to look past one or two soft quarters because the longer trend is bending the right way.

The lesson for retail investors is not to copy the trade. The data on screener.in tells you these are still small-cap stories with cash flow questions, valuation tightness or both. The lesson is in the framework. Find businesses with widening margins, improving capital efficiency and a clear demand tailwind, and then ask if the price gives you enough of a margin of safety.

The next two quarterly results will be the real tell. For Safety Controls, the metric to watch is cash from operations. If it turns positive in FY26, the story holds. For Asian Energy, the merger timeline and Q4FY26 margins will decide whether the recent rally is the start of a multi-year run or a relief bounce.

A simple way to stay on top of these names is to add them to a watchlist and track the quarterly filings.

Disclaimer:

Note: We have relied on data from www.Screener.in and www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.

– Stock Insights News")