Welcome to the latest edition of Dividend Hunter. In the past few weeks, we have looked at companies where strong cash flows could translate into consistent dividends going forward. This includes a debt-free IT Player offering a 7% dividend yield, aPSU with a 6% yield, and a Maersk-backed private-sector port company offering a 5.4% dividend yield.

In our last edition, we covered a lubricant player with a 5.1% yield that powers 1 out of 3 electric buses in India. This edition of Dividend Hunter covers a business that has long been a cash generator and has a 5% dividend yield.

In a fast-evolving corporate landscape where many technology-forward companies hoard cash to weather economic uncertainties, MPS Limited, takes a radically different, shareholder-first approach.

Operating at the profitable intersection of research, education, and corporate learning, MPS has successfully transformed from a traditional content provider into an AI-driven global platform and learning solutions powerhouse.

But what truly sets this company apart for income-seeking investors isn’t just its robust EBITDA (Earnings Before Interest, Tax, Depreciation and Amortisation) margins or its impressive market expansion.

Rather, it is a management team’s operating philosophy of not sitting on excess cash. Welcome to the story of MPS, a historically debt-free cash generator that leverages its efficient operations to fuel a capital distribution strategy.

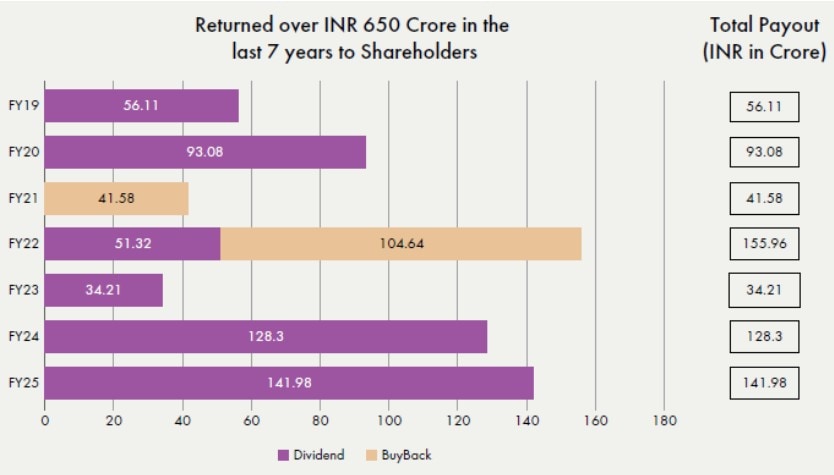

With a strong balance sheet and operating cash flows, MPS has established a track record of wealth creation, returning a staggering ₹650 crore to its shareholders through dividends and buybacks over the last seven years alone.

Returned Over ₹650 crore to Shareholders

For the dividend hunter, MPS represents a future-proof business backed by predictable, steady B2B demand and a commitment to returning surplus capital directly to its investors’ pockets.

At current prices, MPS offers an attractive dividend yield of 5.0% (based on historical payouts). But the moot question is, is this yield sustainable?

Let’s find out.

Business Profile: From Legacy Content to AI-Driven Global Platform

MPS is a global B2B provider of platforms and services for the knowledge management, research, and educational technology industries.

The company’s core competitive moat lies in combining deep subject matter and domain expertise with advanced technology to serve its clients’ entire value chain end-to-end.

Originally built for the science community by Nature (Macmillan’s prestigious journal portfolio), MPS has evolved into a diversified intelligence and content powerhouse. The company operates primarily through three established segments, while a recent acquisition has opened up a fourth major vertical.

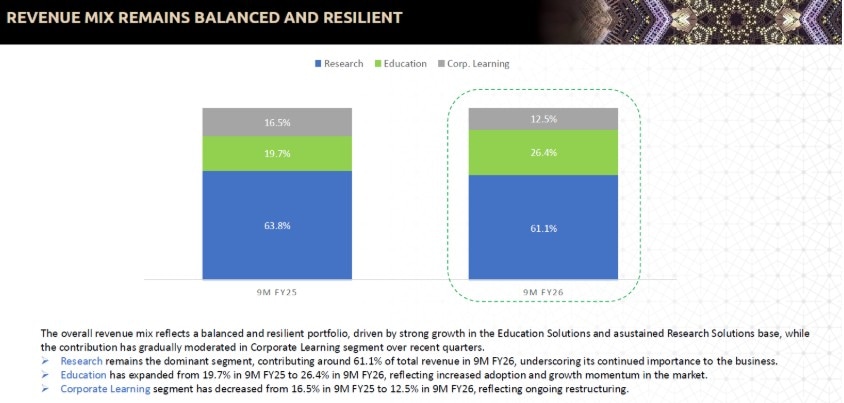

Research Solutions is the core business, contributing over 61% of its revenue in 9MFY26. MPS partners with global publishers and institutions to maintain the integrity of research and the validity of published scientific content.

It provides content and publishing services, scientific editing, formatting, and other editorial services. This segment is expected to perform strongly in FY27 due to new B2B partnerships, including AJE’s recent selection as a preferred vendor for a top international publisher.

The second segment is Educational Solutions, accounting for 26.4% of revenue. MPS is a major player in creating educational products for K-12 and Higher Education customers. It builds courses, develops products, and overhauls legacy content for educational institutions.

This segment is experiencing powerful momentum and is expected to sustain stable, double-digit growth.

AI Pivot: Transforming Research & Education into Agentic Learning Tools

In addition, the company provides corporate learning, which contributes 12.5% of revenue. Operating through brands like MPSi Liberate and MPS Europa, this division provides enterprise training and managed learning services. This is a low-margin business.

Revenue-Mix

Thus, MPS is actively pivoting toward highly complex, experiential learning solutions. Today, they build sophisticated workforce training tools that utilize Virtual/Augmented Reality, immersive training scenarios, AI-agentic bots, and personalized learning pathways.

MPS has also recently entered the healthcare knowledge management business. It recently acquired U.S.-based Unbound Medicine, expanding into the heart of the medical and nursing ecosystem. MPS provides AI-powered digital resources in nursing and medical schools.

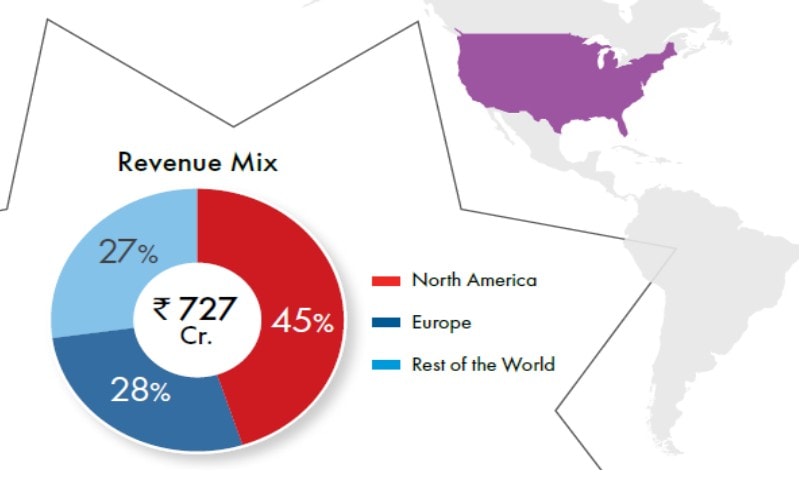

The Concentrated Revenue-Mix

MPS’s business operations are concentrated. About 45% of its revenue comes from North America, 28% from Europe, and the remainder (27%) from other parts of the world. Not only that, but the top 15 clients account for 66% of its revenue.

Geographic-Mix

The 40:40:20 Revenue-Mix Goal

Looking ahead, MPS’s long-term strategic goal is to shift its business toward a “40:40:20” segment mix. This means that 40% of the revenue will be derived from research, 40% from education, and 20% from corporate learning. The Unbound Medicine acquisition will play a big role in achieving this target.

Revenue generated from Unbound will primarily be classified under the Education segment, with a small portion categorized under Research. This will directly accelerate the Education segment’s growth, helping it match the scale of the Research business in the coming years.

Management expects to double Unbound’s revenue over the next few years by leveraging MPS’s global presence in Europe, APAC, and the Middle East to expand Unbound beyond North America. Unbound generates a margin of 14-15%, which is expected to approach the MPS margin of 30% by the end of Q4FY27.

Profitability Update: Internal Automation Driving 29% Margins

The company’s market cap is ₹2,838 crore, as of 02 April 2026.

Historical profit growth has been above 5%. Over the last 3/5 years, however, net profit has grown at a 18%/22% CAGR. Revenue rose by 33.4% to ₹727 crore in FY25.

EBITDA surged 24% to ₹211 crore, with a 29.0% margin. Net profit surged 25.2% to ₹149 crore, driven by internal optimisation and the use of automation. Further, the financials also grew strongly in 9MFY26.

Revenue increased 3.4% year-on-year to ₹563.2 crore in 9MFY26, driven by business expansion and growth momentum in the Education Solutions segment. EBITDA grew 8.7% to ₹168.3 crore, with a 29.9% margin. Net profit grew 23.9% to ₹126.2 crore.

Capital Efficiency: ROCE and ROE Gains Reflect Strong Core Performance

The company’s return ratios remain robust. Return on Capital Employed (ROCE) has risen to 36.6% (up from 29.6% in FY24), and Return on Equity stands at 31.7% (compared to 26.8% in FY24). These ratios indicate that it is effectively utilizing its capital and equity to generate profit.

The Asset-Light Engine: Turning 29% Margins into Shareholder Cash

MPS has a strong and consistent track record of rewarding its shareholders through robust capital distribution policies. Management believes that excess cash should not be hoarded. Consequently, the company prioritizes returning its surplus capital to its investors through dividends and buybacks.

The primary engine supporting the company’s dividend policy is its massive cash flow from operating activities. In FY25, its net operating cash flow stood at ₹101 crore, down from ₹118 crore in FY24.

Since this company operates in the B2B knowledge management and educational technology sectors, it enjoys predictable, stable demand from institutional clients. This business is also ‘asset-light,’ enabling the company to convert its earnings into reliable cash flow.

MPS optimized working capital ensures that profits rapidly convert into liquid cash. The company boasts an impressive Cash Turnover Ratio of 11.5. This allows it to meet its current liabilities entirely through internal accruals while simultaneously maintaining high cash reserves.

The company’s balance sheet has remained entirely debt-free. As a result, the maximum portion of operating cash flow becomes available to be returned to shareholders. As of 31 December 2025, the company reported a total cash and cash equivalents position of ₹143 crore.

The cash flow directly translates to dividends because of the management’s operating philosophy: they do not believe in “sitting on excess cash”. The Board evaluates MPS’s strategic growth requirements over a 6-12-month horizon.

If there is no immediate appetite or need to deploy capital for acquisitions or internal investments within that window, the surplus cash is systematically distributed to shareholders as dividends or buybacks.

This systemic approach has allowed it to return over ₹650 crore to its shareholders over the last seven years through dividends and buybacks.

Dividend Track Record: 5.0% Yield and a Growing Payout Pipeline

On the back of such cash flow, the company has already paid an interim dividend of ₹33 in FY26 Year-To-Date (YTD). This translates to a dividend yield (at ₹1,659 per share) of 2% YTD in FY26.

Historically, MPS has paid dividends each year for the past four financial years. Furthermore, the dividend has been increased every year from FY22 to FY25. It paid a total dividend of ₹83 in FY25, translating into a dividend yield of 5.0%.

In FY24, it paid a total dividend of ₹75, ₹20 (FY23), and ₹30 (FY22). The dividend payout has consistently been less than the 100% threshold required by our filter. The dividend could continue to rise as MPS financials accelerate in the coming years.

Going forward, MPS’s strategic outlook is governed by its “Vision 2027”, which targets a revenue of over ₹1,500 crore by FY28. It plans to achieve this through new customer acquisition, consistent investment in new technology capabilities, and the acquisition of growing assets.

Valuation: Is MPS Limited Trading at a Discount to Sector Peers?

Valuation-wise, MPS trades at a price-to-equity multiple of 17.3x, at a discount to the 5-year historical median of 20.7X. The valuation is at a discount to Veranda Learning (52.6X) and Jaro Institute (19.5X).

The Verdict: Should Dividend Hunters Add MPS to Their Watchlist?

MPS meets the key Dividend Hunter filters. It has a steady profit growth, strong cash flows, and a payout ratio within thresholds.

Given a yield of 5.0%, growing profitability, and a historical record of dividend payments, it appears likely that the dividend payout trend will continue. Dividend hunters should add this stock to their watchlist and see if it continues to reward shareholders with a lucrative dividend yield.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation. Only in cases where the data were unavailable have we used an alternative, widely accepted, and widely used source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.