For a good part of 2026, a single stretch of water held the oil market hostage. The Strait of Hormuz, barely 40 km wide at its tightest point, carries close to a fifth of the world’s oil and gas. When the conflict between the United States, Israel and Iran shut it in early 2026, crude prices jumped and India, which imports the bulk of what it burns, felt the pinch at once.

On 18 June, that picture changed. Washington and Tehran signed a memorandum of understanding, that reopens the strait, removes the US naval blockade and starts a 60-day clock for talks on sanctions and Iran’s nuclear programme. This is not a finished peace deal, and the hardest questions, on missiles and enrichment, are still open. But for the first time since February, oil can move freely again.

A reopened strait is not just a diplomatic headline. It is a working reality for the firms that store, move and service India’s energy. Two of them stand out for an odd reason: both currently earn operating margins above 60%, a number most businesses could only strive for. One stores the oil and gas that arrives. The other works under the sea where it is drilled. Here is what the figures actually say, and where the story gets complicated.

#1 Aegis Vopak Terminals: A Toll Booth On India’s Energy Imports

Incorporated in 2013, Aegis Vopak Terminals owns and runs storage tanks for liquefied petroleum gas (LPG) and liquid products such as petroleum, chemicals and vegetable oils. It is a joint venture between India’s Aegis Logistics and Royal Vopak of the Netherlands, a storage specialist with a 400-year history and terminals across 23 countries.

With a market cap of Rs 25,628 cr, it currently operates two LPG terminals and eighteen liquid terminals dotted along India’s ports.

The model is simple and powerful. Aegis does not buy or sell a drop of oil. It rents out tank space and charges for throughput, the way a toll booth charges for cars. When more energy flows through Indian ports, its tanks stay full and its meters keep ticking. A normalised Strait of Hormuz points to exactly that, steadier cargoes of LPG and crude landing on the coast.

India imports a large share of the LPG that fills its kitchen cylinders, and that gas has to be parked somewhere before it reaches a bottling plant. Aegis owns a slice of that scarce storage. The moat is undeniable.

Base-Effect Distortions: Early Zero-Revenue Cycles v/s Growth Metrics

A word of caution before the numbers. Aegis Vopak listed only in May 2025, and its operations really began in 2022-23. In 2021-22 it booked almost no sales at all. So, the neat five-year compound growth figure I normally give would be built on a base of near-zero, and it would flatter rather than inform. I would hence like to show the actual yearly numbers instead.

| Financial Year | FY22 | FY23 | FY24 | FY25 | FY26 |

| Sales (Rs cr) | 0 | 353 | 562 | 621 | 923 |

| EBITDA (Rs cr) | -1 | 229 | 398 | 458 | 686 |

| Net Profit (Rs cr) | -1 | 0 | 87 | 127 | 342 |

Sales rose from Rs 353 cr in FY23 to Rs 923 cr in FY26. EBITDA (Operating profit) climbed from Rs 229 cr to Rs 686 cr over the same period. Net profit moved from roughly breakeven to Rs 342 cr. On screener’s three-year reading, sales have compounded at about 38% a year, which is quick going for an infrastructure business. The net profit for the same period logged in a compound growth of 1,472% per screener, which has to be taken with a pinch of salt as the base was very small.

Structural Valuations: Balancing a 74% Margin Against a Big Debt Load

The margin is the headline act. In FY26 Aegis earned an operating margin of about 74%, and it has held in the low-70s for three straight years. That is the quiet beauty of a tank: once it is built, filling it again costs very little.

The share price of Aegis Vopak Terminals was about Rs 250 when it was listed in June 2025 a year ago, and as on 17th June 2026 it was Rs 234, which is a noteworthy drop.

The stock trades at roughly 84 times earnings and at nearly five times its book value.

Also, the stock is trading at a PE of 84x which is higher than the current industry median of 47x. Because it has barely a year of listed life, there is no ten-year median PE figure to lean on, and any such number would simply be made up. It is possible that investors are plainly paying ahead for the growth.

One more thing to look at is the debt. Building tanks eats capital, and borrowings stood at about Rs 3,731 cr in FY26. That is why the return on equity, near 10%, looks ordinary despite those fat margins. In plain terms, for every Rs 100 of shareholders’ money, the company currently earns about Rs 10.

There is a brighter side to the balance sheet as well. Operating cash flow reached about Rs 702 cr in FY26, and borrowings came down from roughly Rs 4,009 cr a year earlier as money raised at the IPO came in. A capital-heavy business that is starting to throw off real cash is a healthier thing than the headline debt figure alone suggests.

The promoters, Aegis and Vopak, hold a steady 87%, which at least tells you the people who built the business have not lost their nerve and have their skin in the game.

The company has a strong and diverse client base, including leading public sector oil companies like IOCL, BPCL, and HPCL, private sector giants such as Reliance and Nayara, as well as global chemical majors on long term leases.

#2 Dolphin Offshore: A Revival Story with a Long Shadow

Incorporated in 1979, Dolphin Offshore Enterprises provides services to the offshore oil and gas industry, from diving and sub-sea work to marine support and turnkey engineering. It is now part of the Deep Industries group, which is reviving a company that had all but fallen silent. That history matters enormously for anyone reading the accounts.

With a market cap of Rs 1,566 cr, the company has an elite client list that includes companies like Aban Lloyd, Bechtel International Inc., Cairn Energy, Engineers India, Fugro Geonics, Global Offshore, HPCL, IOCL, L&T, Mazgaon Docks.

The Turnaround Blueprint: Dormant to Deep Industries

Look at the revenue line and a startling gap appears. Dolphin recorded essentially no sales in FY22 and FY23. The business had effectively stalled. But under its new owners, it has been switched back on. Here are the yearly numbers.

| Financial Year | FY22 | FY23 | FY24 | FY25 | FY26 |

| Sales (Rs cr) | 0 | 0 | 6 | 74 | 116 |

| EBITDA (Rs cr) | -1 | -1 | 2 | 46 | 72 |

| Net Profit (Rs cr) | 14 | 36 | 6 | 46 | 69 |

This is why, as with Aegis, a five-year or even a three-year compound growth rate is not worth printing. You cannot compound sensibly from a base of zero. Screener’s own ten-year sales figure for Dolphin is actually negative, at about minus 9% a year, a reminder of how far it fell before it turned. The honest way to read this company is forwards, not backwards.

One figure on the old record can trip up the unwary. Dolphin did report a profit in 2022-23, but it came almost entirely from a one-off other income of about Rs 45 cr, not from running the business. Take that out, and the operating picture only really turns positive from FY24 onwards.

Tracking the Risks of a 974-Day Debtor Cycle

Dolphin’s margins look spectacular. Operating margin was about 62% in FY25 and has run higher still in recent quarters, into the 80s and 90s. But in the most recent quarter of March 2026, it dropped to 27%. Hence this needs to be read. Even with those huge percentages, operations rest on tiny, uneven revenue. A single quarter’s sales can swing from Rs 16 cr to Rs 30 cr. High-margin diving contracts pay well, but they arrive in lumps and are hard to forecast.

There is also a red flag on the balance sheet. Dolphin’s debtor days, the time it takes to collect money from customers, ran near 974 in FY25. That is well over two years. In project-based offshore work some delay is normal, but cash locked up in receivables for that long is a genuine worry.

Reviving a dormant company also costs money, and it shows: borrowings have crept back to about Rs 203 cr by March 2026, and the firm has been spending on assets again after years of selling them down.

Post-Resolution Multiples: Balancing a 2,700% Relisting Rally Against Industry Medians

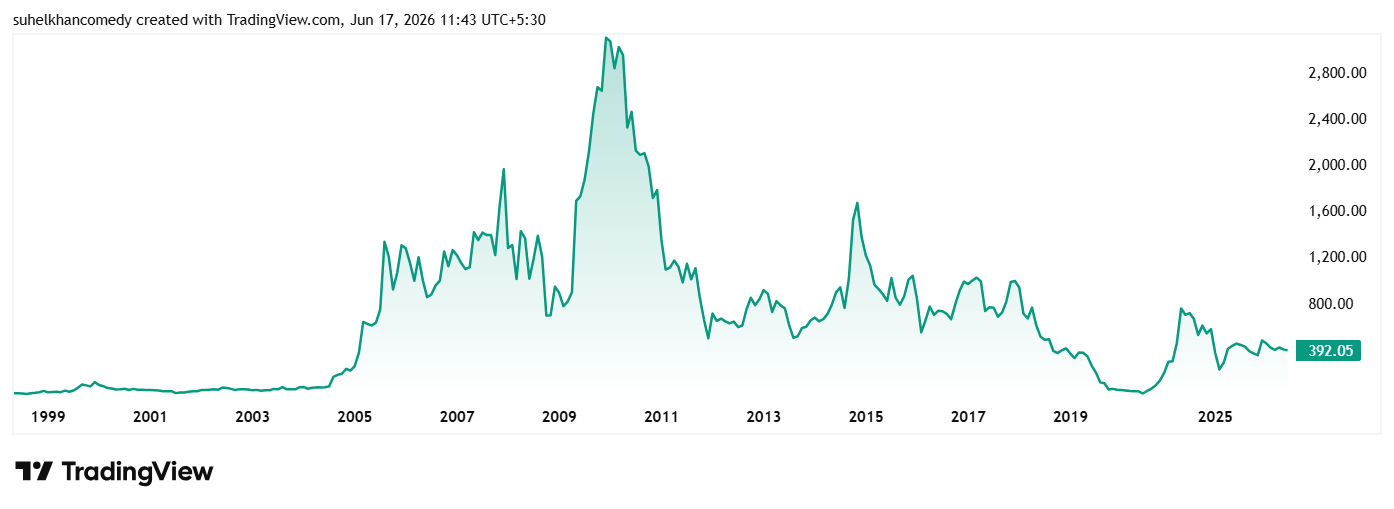

Company was suspended from trading on BSE and NSE from November 4, 2019 due to suspension and penal reasons. Post reduction of share capital as per approved Resolution plan, the equity shares were admitted to dealings on the exchange from August 21, 2023

The share price of Dolphin Offshore was around Rs 14 when relisted in August 2023 and as on 17th June 2026 it was Rs 392 which is a jump of 2,700% in just about 3 years. Rs 1 lac invested at listing would have been close to Rs 28 lakhs today.

At the current price, the stock is trading at a discount of 59% from its all-time high of Rs 949 which it hit around May 2024.

On valuation, the stock trades at a PE of about 23x which is slightly higher than the industry median of 16x. A ten-year median PE band is again not usable here, because the company posted losses and near-zero earnings in several of those years.

The promoter holding sits at about 75%, down from 95% two years ago as the ownership was reshaped under Deep Industries.

Downstream Vulnerabilities to Falling Oil Prices

The thread that runs from a US-Iran thaw to these two stocks is real, but it is not evenly spun.

Aegis Vopak is the cleaner play. It is a toll booth on India’s energy imports, and a busier strait means busier ports. Its margins are genuine, its cash flows steady and its parentage strong. The open questions are price and debt, not the quality of the business.

Dolphin Offshore is the more speculative bet. A calmer oil market could revive offshore activity, which would help it. But this is a small, freshly-revived company with lumpy revenue and a troubling collection record, and its share of any peace dividend is less certain.

One honest caution applies to both. A flood of returning oil could push crude prices down. Cheaper oil is a gift for India’s import bill, yet it can also cool the very offshore spending a company like Dolphin leans on. And the deal initialled this week is a first step, not a settled peace. The strait can shut again as quickly as it opened.

The theme is worth following closely. Whether today’s share prices reward you for following it is, as ever, a separate question, and that homework is yours. Both names, for now, earn a place on the watchlist.

Disclaimer:

Note: We have relied on data from http://www.Screener.in and http://www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, he was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article. The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein.