In this edition of Dividend Hunter, we look at the world’s largest manufacturer of motorcycles and scooters. The business creates regular operating cash flows and follows a clear policy for distributing dividends to its shareholders.

This week’s Dividend Hunter company is a leading player in the two-wheeler automobile industry. At the end of FY26, the company’s domestic market share was 27.9%. In the fourth quarter of FY26, its market share in the entry-level segment reached 65%, the highest in more than a year.

To keep their lead, the management is taking steps to prepare for changes in transportation technology. They are actively building their electric vehicle lineup with new scooters and investing in commercial electric three-wheelers. These newer business areas provide the company with a reliable basis for future sales volumes.

The company we are focusing on today is Hero MotoCorp Limited.

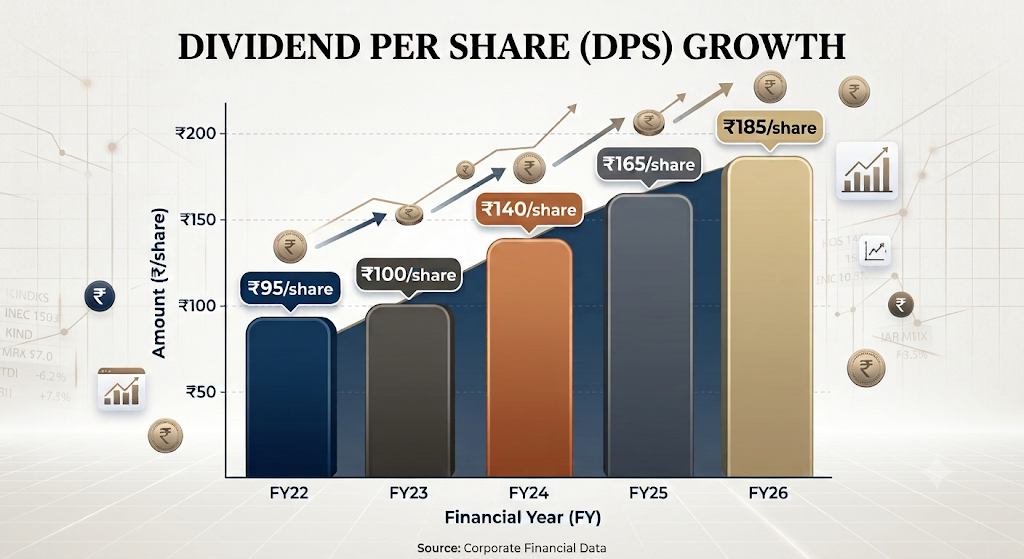

Hero MotoCorp increased its total dividend to ₹185 per share in FY26, compared with ₹165 per share in FY25, reflecting a year-on-year increase of 12.1%. Hero already has a track record of not only paying dividends but also increasing them annually.

When we look at the data, the company has kept a steady habit of returning capital, keeping its dividend payout ratio between 64% and 82% over the last five financial years ending FY26. For investors seeking regular income, this implies that Hero returns at least 69% of its net profit to shareholders.

This raises an important question: can Hero MotoCorp sustain its high dividend payout over the long run? The answer depends on the underlying factors that will continue to support its cash flows, earnings, and capital allocation.

Deconstructing Hero MotoCorp Business

Hero is the world’s largest manufacturer of motorcycles and scooters, a prestigious position it has maintained for 25 consecutive years. It serves a base of over 13 crore customers across 53+ countries.

To meet global demand, Hero operates eight state-of-the-art manufacturing facilities (six within India, one each in Colombia and Bangladesh) with a total annual production capacity of around 94 lakh units. Its business is supported by a highly penetrated distribution network of over 11,000 customer touchpoints worldwide.

The company dominates the entry-level and mass-commuter categories (100 cc) in India with iconic brands such as Splendor+, HF Deluxe, and Passion. However, it has failed to make a meaningful impact in the 125cc, 150cc, and 225cc segments.

Most of its revenue comes from motorcycle and scooter sales, followed by the high-margin Parts, Accessories, and Merchandising segment.

Volume Acceleration: How FY26 Revenue Hit ₹46,830 Crore

Over the last 5 years, Hero MotoCorp’s standalone net profit grew at a 14% CAGR, reaching ₹5,268 crore in FY26. Revenue in FY26 rose by 14.9% year-on-year to ₹46,830 crore, driven by a 10% increase in overall sales volume to 64.7 lakh units.

Operating leverage further boosted operating profitability. The company’s EBITDA (earnings before interest, tax, depreciation, and amortization) increased 17% to ₹6,871 crore. This was driven in part by a 30 bps margin expansion to 14.7%, driven by a favourable product mix and cost efficiencies. In FY26, Net profit also rose 14% to reach ₹5,268 crore.

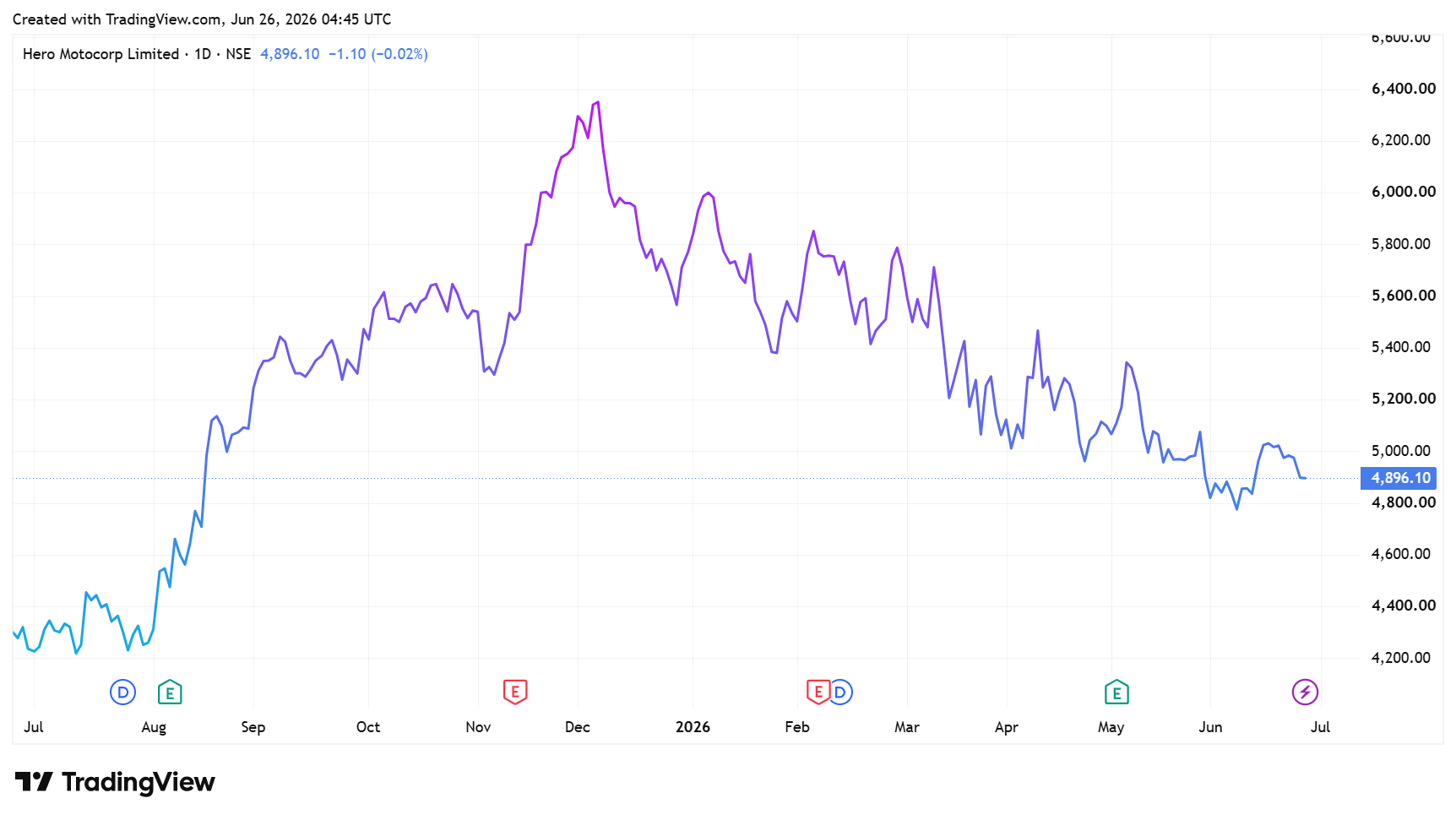

The company’s market cap is ₹97,968 crore, as of 26th June 2026.

Hero MotoCorp Share Price

Return Ratios Audited: The Operational Drivers Behind a 34.1% ROCE

Hero MotoCorp has a debt-free balance sheet. This combination allows the business to report stable return ratios year after year. The company’s return on average equity stands at 25.9%. This suggests that the company is generating healthy profitability from the capital invested by its shareholders.

Return on capital is also strong at 34.1%. This means that Hero consistently generates value from the capital employed in its operations. This strong financial foundation provides the company with the cash flow and financial flexibility needed to sustain its dividend payments over the long term.

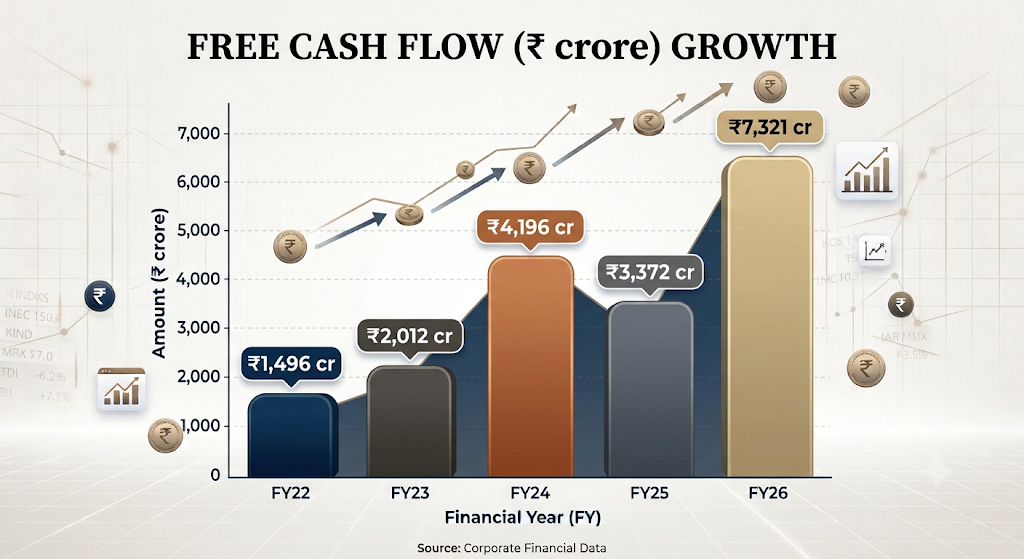

Cash Conversion Reality: Tracking Hero MotoCorp’s ₹7,321 Crore Free Cash Engine

Hero MotoCorp aims to fund its dividend payouts directly from internally generated cash. To see whether they can maintain this practice, it is helpful to examine how their reported profits translate into actual cash, as well as the state of their overall reserves.

Working Capital Dynamics: How Deferred Payables Bolstered Cash Reserves

During FY26, Hero’s net cash flow from operations increased 98.8% to ₹8,314.9 crore. Effective management of working capital drives this cash flow. For example, it took longer to pay its suppliers, which increased trade payables to ₹1,952.6 crore. At the same time, it collected ₹1,081.2 crore from its customers during the year.

A ₹418.5 crore reduction in direct taxes paid also supported the net cash generation during the year. Hero then uses a portion of this cash to fund its factories and develop products. For FY26, it spent ₹1,005.9 crore on property, plant, equipment, and intangible assets. The company also received ₹12.2 crore from the sale of Property, Plant, and Equipment.

If we subtract these capital expenditures from net operating cash, Hero maintains a strong free cash position of ₹7,321.3 crore. This isn’t a one-time event, as Hero has consistently generated free cash flow for at least 10 financial years.

This surplus of liquid capital ultimately enables the company to sustain its high dividend payouts while maintaining a debt-free balance sheet. In FY26, Hero paid ₹3,501 crore in dividends, up from ₹2,799.8 crore in FY25.

These payouts were fully covered by free cash flows, indicating that dividends were funded by internally generated cash rather than debt or reserves. This aligns with the company’s goal of funding its regular dividend payouts directly from internally generated cash.

Further, generating this much cash indicates that earnings are reliable, giving the company the financial flexibility to continue rewarding its shareholders.

Historical Dividend Trajectory: The Math Behind the ₹185 Per Share Payout

Regarding its dividend per share, the company paid ₹185 per share in FY26. At the current share price of ₹4,896, the dividend yield is 3.8%. The historical payout pattern is very interesting and has consistently grown over the years.

Hero paid a dividend of ₹165 per share in FY25, up from ₹140 (including a special dividend of ₹25) in FY24. The FY24 payout was also higher than the ₹100 per share distributed in FY23 and ₹95 per share in FY22. The company currently pays dividends twice a year (interim and final), with ex-dividend dates in February and July.

Additionally, Hero MotoCorp’s regular dividend payout ratio has remained stable at over 69%. In FY22, it paid out 77% of its earnings per share as dividends, a ratio that has remained between 69% and 71% during FY23-FY26.

This payout also aligns with the company’s dividend policy of distributing 68% to 77% of its earnings as dividends. This suggests that the company is returning a larger share of its earnings to shareholders. Consequently, as profitability increases, Hero is likely to not only pay dividends but also continue to increase them.

At the same time, Hero MotoCorp is also funding its capital expenditure.

Capital Reinvestment Strategy: Balancing the Imminent ₹1,500-Cr Infrastructure Spend

After spending a substantial sum in FY26, management has planned a larger capital expenditure of over ₹1,500 crore to expand production capacity for scooters and electric vehicles. Even with these planned investments, cash from daily operations and free cash flow is sufficient to cover these costs.

Going forward, Hero MotoCorp aims to balance the objectives of rewarding shareholders while maintaining sufficient capital to fund future business projects and expansion plans. On the expansion front, its FY27 investment is highly targeted toward fast-growing segments where the company has historically been underrepresented.

The company has already increased the capacity for the Destini 125 by 50% and is in the process of doubling the manufacturing capacity for its highly successful Xoom scooter lineup. It’s also focusing on ramping up the EV business (VIDA) by improving unit economics.

Capacity Milestones: Doubling VIDA EV Manufacturing Before End-FY27

The company’s EV volumes expanded 2.5 times over the previous year in FY26. VIDA is set to expand its capacity by 50% by the beginning of FY27, and plans to double its total EV production capacity before the end of FY27.

The planned doubling of production capacity, along with the expansion of its retail network to more than 360 cities, is expected to improve operating leverage and reduce per-unit EBITDA losses. In addition to vehicle manufacturing, Hero is investing over ₹700 crore to build a second parts plant in South India.

The facility will essentially double its parts capacity, allowing it to capture a larger share of the high-margin aftermarket business. Management estimates it can currently service only 50% of the actual demand. Hero sees strong headroom in its international business.

Beyond Commuter Bikes: The Geopolitical and Premium Product Roadmap

Following a record 41% wholesale growth in FY26, Hero plans to maintain this momentum into FY27. The company plans to commence operations in Brazil, the largest market in Latin America. Hero is also expanding into new African markets, following a successful re-entry into Nigeria.

It also aims to expand into the remaining 50% of the unaddressed market in Bangladesh and rapidly scale its newly launched retail operations in the Philippines and Sri Lanka. On the product front, Hero has a pipeline of launches across commuter bikes, premium motorcycles (Harley-Davidson X440 and Karizma 250), scooters, and the VIDA brand.

The Valuation Disconnect: Why Hero Trades at an 18.3x Discount to Peers

Valuation-wise, Hero MotoCorp trades at a price-to-equity (P/E) multiple of 18.3x, a discount to not only its 10-year historical median (19.6x) but also to the sector median (37.5x) and peers like Bajaj Auto (25.5x) and TVS Motors (55.6x). This gap has persisted due to the faster growth of its peers and their stronger presence in the premium motorcycle segment.

The Dividend Hunter Verdict: Is Hero an Absolute Income Fortress?

The key takeaway is that Hero MotoCorp is well-positioned to sustain its dividend payouts. Because Hero MotoCorp has no debt, stable profitability, and consistently generates surplus funds, it has the financial stability to sustain its dividend payments over time. As long as those strengths remain intact, the payout appears well protected.

Dividend hunters should add this stock to their watchlist.

Disclaimer:

Note: Throughout this article, we have relied on data from http://www.Screener.in and the company’s investor presentation and conference call. Only in cases where the data were unavailable have we used an alternative, widely accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.

About the Author: Madhvendra has been deeply immersed in the equity markets for over seven years, combining his passion for investing with his expertise in financial writing. With a knack for simplifying complex concepts, he enjoys sharing his honest perspectives on startups, listed Indian companies, and macroeconomic trends.

A dedicated reader and storyteller, Madhvendra thrives on uncovering insights that inspire his audience to deepen their understanding of the financial world.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities, or other related investments of issuers and/or companies discussed therein. The articles’ content and data interpretation are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources, and only after consulting such independent advisors as may be necessary.