When a fund manager who has managed money for over three decades makes four new entries in one quarter, retail investors take note. Madhusudan Kela does not chase tickers. He buys themes, often before the rest of the street notices.

His latest exchange disclosures for the quarter ending March 2026 show fresh stakes in 4 new stocks. Together, the four positions are worth roughly Rs 177 cr. Three are deep-cycle stories where past pain has scared off institutional money. The fourth has given a 100% jump in a year, yet Kela still saw room to take a 7% stake.

Let us take a look at the stocks in question.

#1 The Contrarian’s Choice: Buying the 139% Profit Pivot at Aptech

Incorporated in 1986, Aptech Ltd is a pioneer in non-formal education and training in India, with over 800 centres globally. It runs brands like Arena Animation, MAAC, Lakme Academy and Aptech Aviation Academy.

With a market cap of Rs 636 cr, Aptech is firmly small-cap in which Kela has picked up 6,17,000 shares, or 1.1% of the company, worth Rs 6.8 cr. Rekha Jhunjhunwala, Utpal Sheth and Gopikishan Damani are on the list of promoters of Aptech.

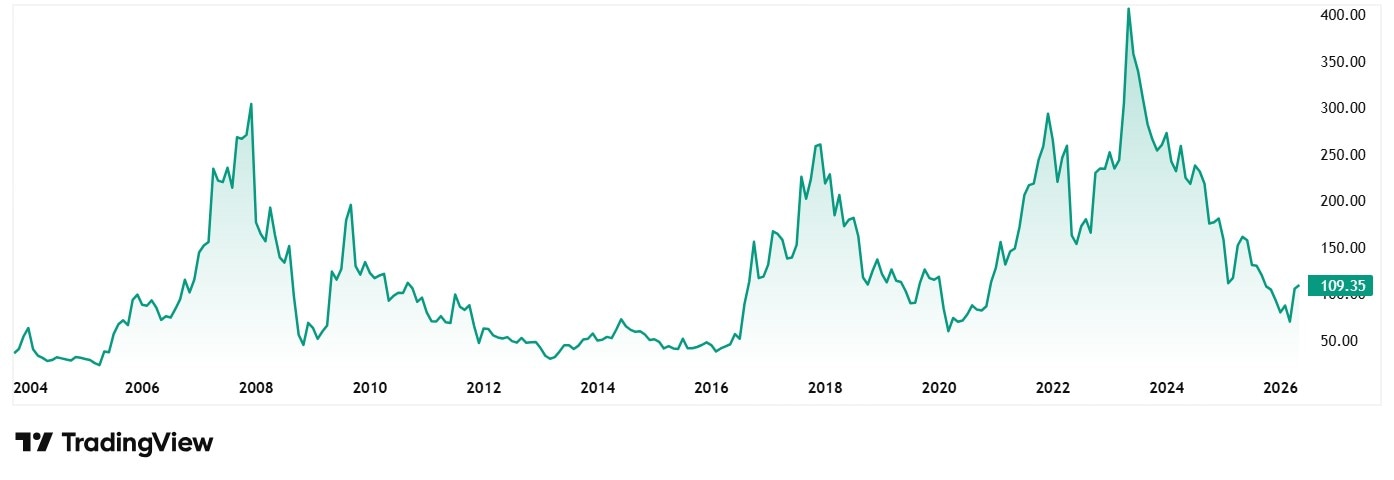

The stock has seen a correction of 30% in a year, sliding from Rs 156 to Rs 109 at the time of his entry. Which hints at this being a beaten-down purchase, not a momentum chase.

However, the recovery is now visible. In Q3 FY26, revenue rose 22% year-on-year to Rs 137 cr and net profit jumped 139% to Rs 8.6 cr. The first six months of FY26 added up to a profit of over Rs 13 cr, almost 25% higher than the same period last year. Two consecutive quarters of profit growth is the kind of inflection a value investor watches for.

The other pull is the dividend. Aptech has a yield of 4.1% in a flat market, with a payout of 88%. In FY25 alone the company paid out Rs 4.50 per share. That is rare in a small-cap, rarer still when the company is also almost debt-free.

The share price of Aptech was Rs 153 in May 2021 and as on 8th May 2026 it was Rs 110, which is a worrisome drop.

The stock trades at a P/E of 22x and the industry median is 28x. The 10-Year median PE is 37x while the industry median for the same period is 24x. The promoter holding is 47.4%, with no pledged shares.

#2 Indiabulls: ₹104 Cr Real Estate Gambit, Banking on a Post-Merger Recovery

Once known as Yaari Digital Integrated Services, Indiabulls Ltd was renamed in October 2025 after a sweeping merger of 17 group companies, including Dhani Services and Indiabulls Enterprises. The company now runs two clean verticals: real estate development across Delhi NCR, Mumbai and Ludhiana, and financial services covering broking, digital lending, payments and asset reconstruction.

This is Kela’s biggest new bet of the quarter. He has picked up 5,15,88,175 shares, or a 2.2% stake, worth Rs 104 cr. The market cap is Rs 4,658 cr.

The numbers tell a striking story. For FY26, the company posted consolidated revenue of Rs 833 cr and a profit after tax of Rs 346 cr. That is a complete flip from FY25, which carried a loss of around Rs 68 cr.

Q4 FY26 alone delivered revenue of Rs 409 cr and PAT of Rs 194 cr, with a margin of 46.4%. Real estate was the workhorse, contributing about Rs 143 cr at the operating level. For the full year, sales bookings touched Rs 2,752 cr, with 909 units sold and 22 lakh sq ft moved.

What probably caught Kela’s eye is the gross development value (GDV) pipeline. The company has guided for over Rs 21,366 cr of GDV across 110.52 lakh sq ft. Management has set a target of doubling real estate profit in FY27 and tripling it by FY28.

The financial services side adds steady income. The broking arm reported FY26 revenue of Rs 124.4 cr, with client assets crossing Rs 68,000 cr. The asset reconstruction business held assets under collection of Rs 3,794 cr and recovered Rs 288 cr in the year.

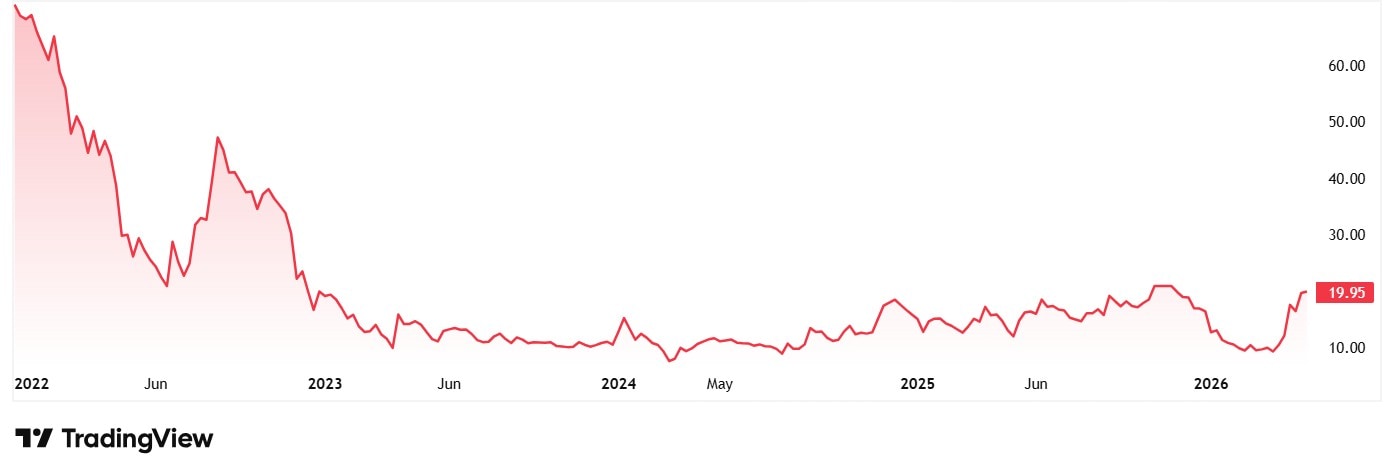

The share price of Indiabulls Ltd was 84 in May 2021 and as on 8th May 2026 it was Rs 20. But it must be noted that the company has gone through a massive merger phase in October 2025, and hence the current prices are adjusted for the same.

The stock currently trades at a PE of 14x and the industry median is 20x. The 10-year median PE for the company is 19x while the industry median for the same period is 24x.

ROE has climbed back to 23% and ROCE to 16% while the company also carries a tax shield of Rs 3,000 cr inherited from the merger.

#3 Simplex Infrastructures: The 102-Year-Old Loss-Making Contractor

Simplex Infrastructures Ltd is one of the oldest construction names in India. Set up in 1924 and run by the Mundhra family of Kolkata, the company has executed more than 2,600 EPC and turnkey projects across transport, power, mining, marine and urban infrastructure. Past delivery includes Mumbai’s Lalbaug Flyover, the Eastern Express Freeway, Delhi’s IGI Airport and the Udaipur airport terminal.

The decade has not been easy. Sales fell at a compound rate of -23.2% over the past five years. The three-year average ROE was deeply negative at -52.5%. Promoters have pledged 33.1% of their holding. Debtor days remain stretched at 220.

Yet Kela has spotted a turn. He has bought 9,55,200 shares, or a 1.2% stake, worth Rs 21.4 cr.

Let us look at the numbers to see what pushed Kela for this move. In Q3 FY26, Simplex reported net sales of Rs 248 cr, up 7.8% year-on-year, and a consolidated net profit of Rs 8.1 cr. That is a sharp turnaround from a loss of Rs 11 cr in the same quarter last year. Q2 FY26 had already shown the lift, with profit at Rs 8.62 cr against a loss a year earlier.

Mutual fund holdings tell the same story. Per Trendlyne, MF participation has risen from zero in March 2025 to 4.55% in the March 2026 quarter. That kind of institutional build-up is rare for a stock still rated cautiously by most brokerages.

The current market cap is Rs 1,807 cr, with revenue of Rs 1,020 cr and profit of Rs 65 cr on a trailing basis. Operating cash flow turned positive in FY25 at Rs 207 cr against a negative figure the previous year. Kela’s cheque size of Rs 22 cr suggests he is testing the thesis rather than betting the house.

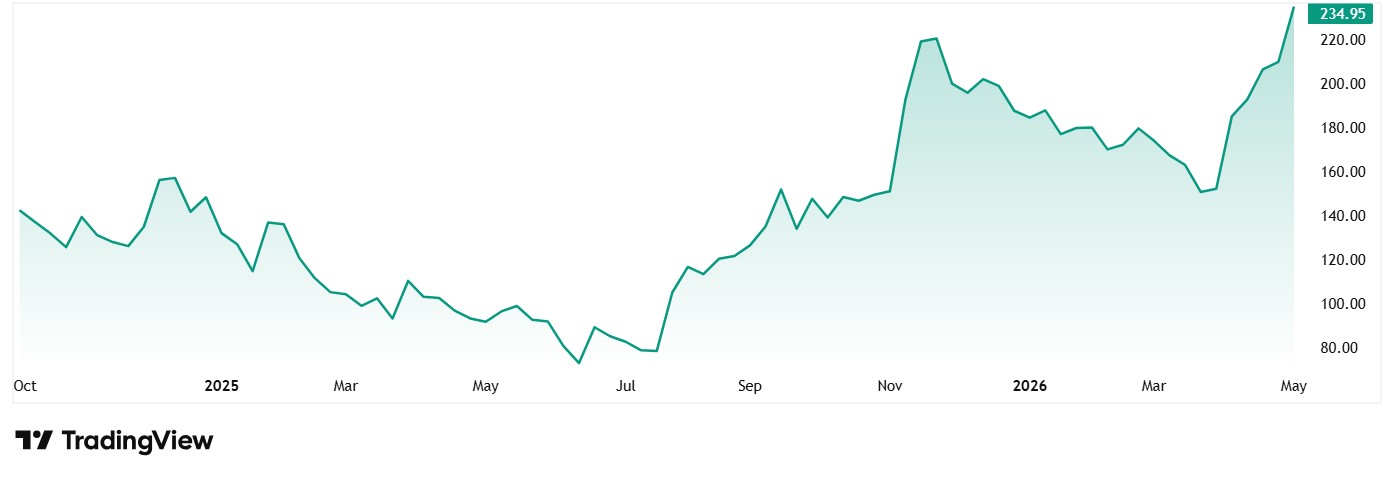

The share price of Simplex was Rs 31 in May 2021 and as on 8th May 2026 it was Rs 224, which is a jump of 622% in 5 years.

The company’s share is trading at a PE of 33x and the industry median is 19x. The 10-year PE for the company is 15x while the industry median for the same company is 17x.

Company is reporting continuous losses for many years resulting in substantial erosion of its net worth. It also defaulted on payment to its lenders, and has overdue payments to operational creditors, out of which certain operational creditors have also applied before the NCLT for debt resolution.

#4 Subam Papers: The 70% Capacity Jump Kela is Doubling Down On

Of the four picks, Subam Papers Ltd is probably a surprise inclusion. The Tirunelveli-based kraft paper and packaging maker listed on the BSE in October 2024 at an IPO price of Rs 152. The stock is up over 100% in the past year. Yet Kela has still gone in big.

He has picked up 19,28,000 shares, or a 7% stake, worth Rs 45 cr. As a percentage of the company, this is the largest of his four new positions.

Subam manufactures kraft paper, duplex board, paper cones, tubes and corrugated boxes. End-uses range from e-commerce packaging to textile yarn winding, FMCG cartons and industrial wrapping. Wastepaper is the primary raw material, which keeps input cost low.

The growth runway is the story. The company’s wholly-owned subsidiary, Subam Paper Boards, started commercial production at a new plant in Tamil Nadu in April 2026. Total consolidated capacity has jumped 70.9% to 3,07,750 MTPA. Management has guided that consolidated production will cross 1,000 metric tons per day after expansion of PM1 (duplex board) to 150 MTPD, PM2 (kraft paper) to 400 TPD, PM3 (multi-grade paper) to 350 TPD and a 100 TPD cone board machine.

The financials back the call. FY26 consolidated revenue came in at Rs 539 cr with profit of Rs 27 cr. Over the past five years, revenue has grown at a CAGR of 17%, against an industry average of 9%.

The stock price currently Rs 201 which is a good jump over Rs 142 5 years ago in May 2021. With a market cap of Rs 552 cr and a P/E of around 14x, the company’s Promoter holding is 59%, down from 70% in September 2025 due to a recent preferential issue at Rs 152, where 42.34 lakh shares were allotted to non-promoter investors.

The one yellow flag is the dividend payout, which is zero. The company is in capex mode, so retained profits are funding new capacity. That is a fair trade-off when the topline is doubling.

Turnaround Tickets or Value Traps?

Madhusudan Kela has not picked four similar stocks. Aptech is a high-yield, low-growth defensive trade. Indiabulls is a structural turnaround in real estate after a corporate clean-up. Simplex is a deep value bet on a beaten-down infrastructure name. Subam Papers is a growth and capex story.

What ties the four together is the absence of consensus. None sit on a typical broker’s hot list. Each requires conviction in a specific catalyst, a profit recovery, a merger payoff, a debt clean-up or a capacity ramp.

Retail investors often see superstar buying and chase the stock the next day. The smarter approach is to study what the buyer saw, then test the hypothesis with one’s own numbers. Two of these companies are still loss-makers if you average the past three years. One has paid no dividend since listing. One trades at a deep discount to its 52-week high.

Kela possibly sees them as turnaround tickets, and turnarounds either work or they do not. The simplest way to track them is to add these stocks to a watchlist and watch the next two quarters of results. Kela has placed his bets. The market will tell us soon enough whether he saw it first.

Disclaimer:

Note: We have relied on data from http://www.Screener.in and http://www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, He was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.