Artificial intelligence has triggered the biggest spending wave technology has seen in years. Every large company now wants an AI plan, and money is pouring into chips, data centres and software. But for an investor, the exciting story and the profitable investment are not always the same thing. In a gold rush, the steady money is often made by the people selling picks and shovels, not the ones panning for gold.

That idea has a quiet following in India. Over the past two years, foreign investors have been trimming their Indian technology holdings (and much else). Yet one group has been doing the opposite in select names. Domestic institutional investors (DIIs), which is the formal term for our mutual funds, insurers and pension funds, have been raising their stakes in companies that build the plumbing of the AI economy. When local fund managers keep buying while foreign money leaves, it is worth asking what they see.

Two stocks stand out that make real parts of the AI machine. One in hardware and engineering, the other in software. Both have had bumpy share prices of late, which makes the steady domestic buying more interesting. Let us look at what each company actually does, what the numbers say, and whether the funds are onto something.

#1 Cyient: A Chip Designer Quietly Rebuilding Around AI

Cyient, based in Hyderabad and listed since the 1990s, is an engineering and technology firm. In plain terms, it does the detailed design and technical work behind aircraft, trains, telecom networks, medical devices and, increasingly, computer chips. The current market cap is about Rs 9,950 cr.

Hardware Meets Generative AI: The 3-Nanometer Catalyst

Cyient touches AI in two very different ways. The first is hardware. Through its semiconductor arm, the company designs custom chips, the kind that sit inside data centres and specialised devices. This includes application-specific processors built for machine learning, plus high-speed optical links that let chips talk to each other inside a server. AI runs on silicon that never sleeps, and Cyient helps design that silicon at advanced sizes down to three nanometres. This is picks-and-shovels work in its purest form.

The second is software and services. Cyient has built its own generative AI tools to speed up engineering, such as Coddy, which helps move old software to modern code, and CyFAST, which automates testing. In June 2026 the company also agreed to buy TAO Digital, a Santa Clara firm with more than 3,500 staff, for about $218 Mn. TAO is an AI-native data and engineering company, and the deal is meant to help Cyient move its clients from basic digital work to full AI projects. It is a clear signal of where management thinks demand is going.

The Data Disconnect DIIs Are Willingly Ignoring

Cyient grew well for a few years and then hit kind of a speed breaker in FY26.

| Financial Year | FY21 | FY22 | FY23 | FY24 | FY25 | FY26 | 5-Yr CAGR |

| Sales (Rs cr) | 4,132 | 4,534 | 6,016 | 7,147 | 7,360 | 7,268 | 12% |

| EBITDA (Rs cr) | 575 | 818 | 1,003 | 1,303 | 1,138 | 899 | 9% |

| Net Profit (Rs cr) | 364 | 522 | 514 | 703 | 648 | 463 | 5% |

As you can see, sales rose from Rs 4,132 cr in FY21 to Rs 7,268 cr in FY26, a compound rate of about 12% a year. EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) grew about 9% a year to Rs 899 cr. Net profit rose only about 5% a year to Rs 463 cr. The company has a current debt to equity ratio of just 0.08, making it virtually debt free.

But if you notice, sales barely moved in FY26, while both EBITDA and net profit actually fell. This was a soft year, driven by weaker demand and thinner margins. Anyone buying the stock is betting the AI push turns this around, not that the recent trend continues.

The Institutional Accumulation Matrix: DIIs Jump to 41% |

What makes the story interesting is the gradual and consistent increase in DII stake the company saw in the last years. Take a look at how the DII holding shaped up quarter on quarter in the last 2 years.

| Quarter | Jun-24 | Sep-24 | Dec-24 | Mar-25 | Jun-25 | Sep-25 | Dec-25 | Mar-26 |

| DII Holding | 27.08% | 29.72% | 30.32% | 34.13% | 35.63% | 38.42% | 39.51% | 40.98% |

Source:screener.in

Just in the last 2 years, the DII holding has jumped from 27% to 41%. Over the same time, foreign investors cut their holding from about 31% to just over 15%. In simple terms, as foreign money walked out, domestic funds absorbed almost all of it.

The top names that hold a stake are HDFC Tax Saver fund, DSP Regular Saving Fund, ICICI Prudential India Opportunities Fund, Kotak Smallcap Fund, Life Insurance Corporation of India, Nippon India Funds etc.

Promoters have held steady at about 23%. This is the heart of the story. Local fund managers have been the buyers of a beaten-down stock, which suggests they are possibly backing the AI turnaround rather than the recent results.

A 64% Valuation Haircut: Bargain or Value Trap?

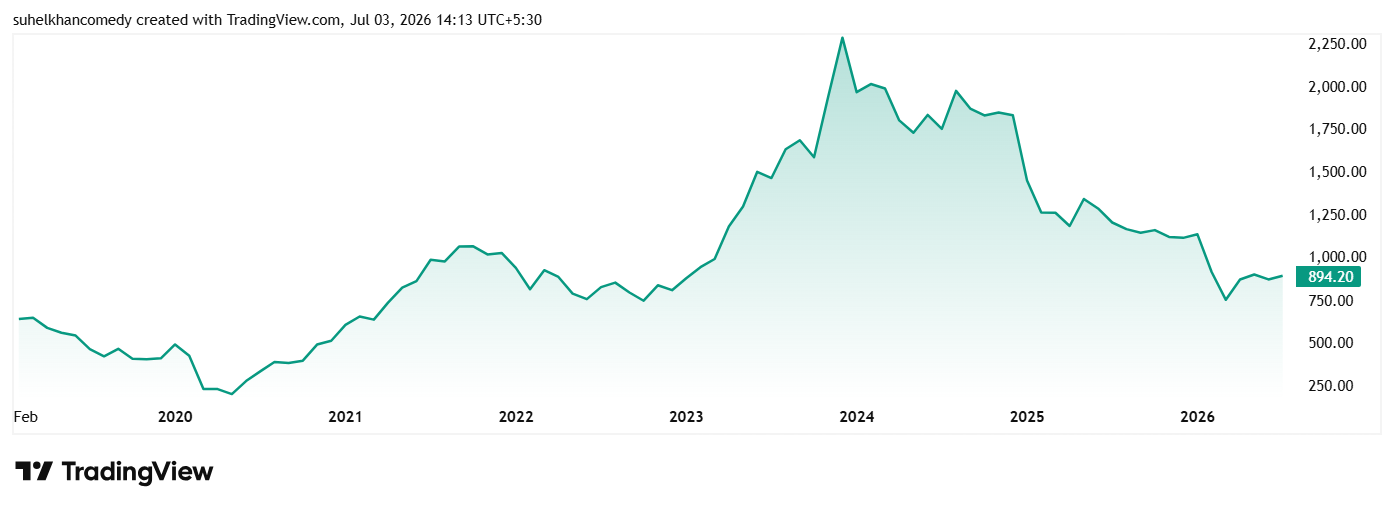

The share price of Cyient was around 850 in July 2021 which climbed up in the coming years to hit its all-time high of Rs 2,459 in December 2023. However, post that the stock has witnessed a brutal battering if I may call it so. As on 3rd July 2026, the price was Rs 895.

At the current price of Rs 895, the stock is down 64% from its all-time high of Rs 2,459 and 32% from its 52-week high of Rs 1,318. The DIIs have probably made full use of this beating the stock has taken, as they bet on the AI theme.

Regarding valuations, the company’s share is trading at a PE of 21x against the current industry median of 24x. The 10-year median PE for the stock is 19x while the industry median for the same period is 32x.

#2 Persistent Systems: The Code-First Growth Engine Targeting $2 Billion

Persistent Systems, based in Pune, is a software services company. Where Cyient leans on hardware and engineering, Persistent lives in code. It helps large firms in banking, healthcare and technology build and modernise their software, and it has made AI the centre of its pitch. Its own tagline is a play on words: Re(AI)magining the World.

The AI Engine Inside Persistent

With a market cap of Rs 74,300 cr, Persistent lists data and AI as one of its main service lines, and it is turning that into real revenue. In a recent quarter, the company reported a jump in sales of AI software licences, which lifted margins. It works closely with the big platform owners such as Microsoft, Amazon and Salesforce, and has even teamed up with IIM Ahmedabad on a framework to help companies measure the returns on their AI spending.

The pitch is straightforward. As enterprises move from AI experiments to full rollouts, Persistent wants to be the firm that builds and runs those systems. In line with that goal, the company recently made its boldest move yet as it agreed to acquire Nagarro, a Europe-focused digital engineering firm, in an all-cash deal worth about 1.27 billion euros.

The aim is to widen its footprint in Europe and push toward a stated goal of $2 billion in annual revenue by FY27.

The Price of Precision: A 33% Profit CAGR Meets a 39x PE Multiple

If Cyient is a turnaround bet, Persistent is the opposite. Its record is one of steady, strong growth, as the consolidated figures show.

| Financial Year | FY21 | FY22 | FY23 | FY24 | FY25 | FY26 | 5-yr CAGR |

| Sales (Rs cr) | 4,188 | 5,711 | 8,351 | 9,822 | 11,939 | 14,748 | 29% |

| EBITDA (Rs cr) | 683 | 958 | 1,519 | 1,676 | 2,058 | 2,795 | 33% |

| Net Profit (Rs cr) | 451 | 690 | 921 | 1,093 | 1,400 | 1,865 | 33% |

Sales more than tripled in five years, from Rs 4,188 cr to Rs 14,748 cr, a compound rate of about 29% a year. EBITDA grew about 33% a year to Rs 2,795 cr, and net profit rose at a similar 33% pace to Rs 1,865 cr. So, every single year is higher than the last on all three measures. The company also earns a strong return on the money it uses, with return on capital employed (ROCE) of 34%, and is virtually debt free with a debt-to-equity ratio of 0.06.

Navigating the 1.27 Bn Euro Expansion Risk

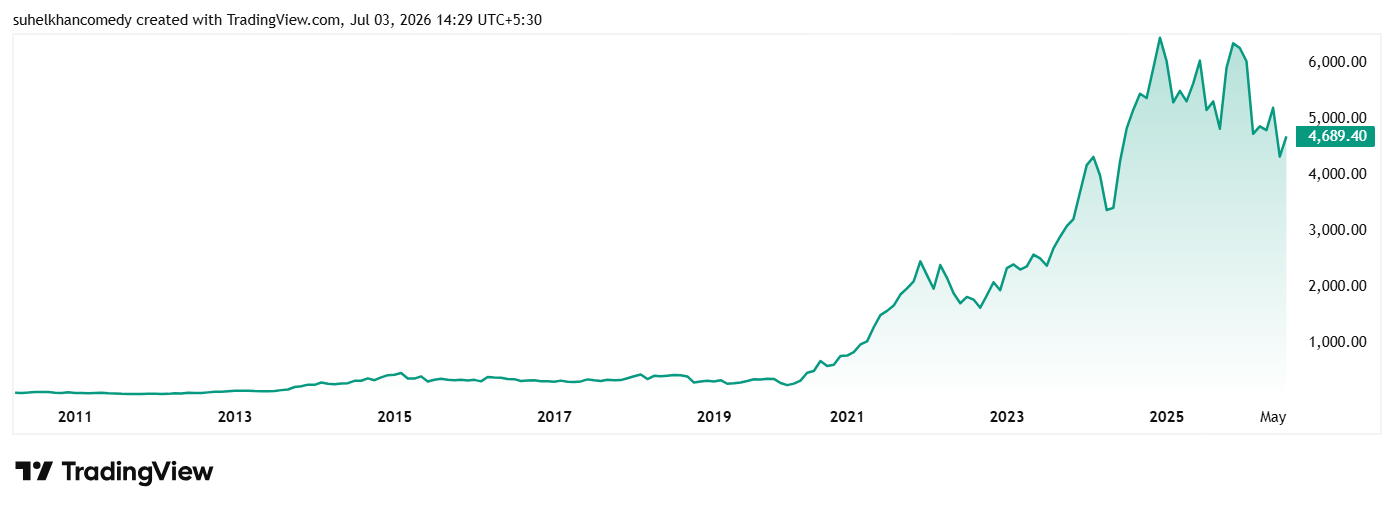

The share price of Persistent Systems was about Rs 1,380 in July 2021 and as on 3rd July 2026 it was Rs 4,710, which is a jump of over 240% in 5 years.

Like Cyient, the share price of Persistent Systems also climbed to its all-time high of Rs 6,789 in December 2025, after which it logged a sharp correction. At the current price of Rs 4,710 the stock is down 30% from its all-time high.

A large part of this correction came right after the Nagarro deal was announced, when the stock dropped sharply in a single session and at least one brokerage cut its rating on worries about how hard it will be to blend a big overseas firm into the business. Large acquisitions can add revenue quickly, but they can also squeeze margins and take years to settle. That risk is now sitting in the price.

Regarding valuation, the share is trading at a PE of 39x against the industry median of 22x. The 10-year median PE for the stock is 36x while the industry median for the same period is 23x. Over the past five years the stock has, on average, traded closer to 55x. By its own recent standards, in other words, it is actually cheaper than usual. Whether that is a fair price still depends on the growth continuing and the Nagarro deal working out.

The Gentle DII Accumulation

Domestic funds have bought in here too, though more gently than with Cyient.

| Quarter | Jun-24 | Sep-24 | Dec-24 | Mar-25 | Jun-25 | Sep-25 | Dec-25 | Mar-26 |

| DII Holding | 28.23% | 27.37% | 26.26% | 26.85% | 27.77% | 30.60% | 29.80% | 30.47% |

Motilal Oswal Midcap Fund, HDFC Mid-Cap Fund, Kotak Midcap Fund, Nippon India Growth Fund, Life Insurance Corporation of India and Aditya Birla Sun Life Flexi Cap Fund are some of the names that show up in the list of DIIs holding stake in Persistent.

A Turnaround Promise vs. A Proven (But Pricey) Winner

The world is only at the start of its AI build-out. Data centres are rising everywhere, enterprises are shifting budgets toward AI readiness, and none of it happens without the chips, the engineering and the software layer underneath. Firms that supply those building blocks today stand to earn for years as the technology spreads from pilots into everyday use.

Cyient sits on the hardware and engineering side of that trend. Persistent sits on the software side. Both are real businesses with real customers, not just AI slogans, and domestic fund managers have clearly decided that both deserve a bigger place in their portfolios.

But a good theme and a good buy are not the same. Cyient offers a cheap price and a hopeful AI pivot, but its recent profit has been shrinking, and the turnaround is a promise, not yet a result. Persistent offers proven, high-quality growth, but at a rich price and with a large, risky acquisition to digest. One asks you to trust a recovery. The other asks you to keep paying up for a winning streak. The funds have placed their bets. Add these stocks to your watchlist to ensure you don’t miss out on any big movement.

Disclaimer:

Note: We have relied on data from http://www.Screener.in and http://www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, he was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article. The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein.