A closer look in the specialty chemicals aisle of the Indian market and you will hear the same worry on repeat. Chinese factories keep dumping fluorochemicals and agrochemicals at prices local firms cannot match. Margins get squeezed, order books turn jumpy, and the China headache refuses to go away. So, some investors have started hunting for corners of the chemical world that China cannot easily flood. One such corner is hiding in plain sight.

Crushed bones, lime, acid and clean water go in. Out comes gelatin and ossein, the raw material behind pharmaceutical capsules, food gelling agents and protein supplements. It sounds unglamorous because it is. But it is also tightly regulated. A gelatin plant that wants to supply drug makers needs years of certification, audits and approvals. You cannot set one up in a weekend. That paperwork is the moat (a barrier that keeps new rivals out), and it is why a handful of Indian firms have the field largely to themselves.

Two of them are listed and small, with no famous investors on its share register. So, this is not a story about whose portfolio they sit in. It is a structural story about pricing power, clean balance sheets and valuations that still look cheap next to the wider chemical pack. Let us dig deeper, and let us also be honest about where the easy headline breaks down.

#1 Nitta Gelatin India: The Capsule Leader the Market Ignored for Years

Incorporated in 1975 and based in Kochi, Nitta Gelatin India is the country’s largest maker of gelatin, ossein and collagen peptide. It is a joint venture with the Kerala State Industrial Development Corporation holding about 32% and Osaka-based Nitta Gelatin Inc of Japan holds about 43%, which together give the promoters a 75% grip.

With a market cap of Rs 1,562 cr, the company manufactures gelatin for pharma and food, di-calcium phosphate for poultry feed, and a consumer collagen range sold under the Wellnex brand.

Decoding the 75% Promoter Grip and the Regulatory Paperwork Moat

We must use the word monopoly a bit carefully here. Nitta is the biggest, but it is not alone. India Gelatine and Chemicals, Narmada Gelatines and a few others share the same small pond. What they all enjoy is a protected pocket. Gelatin for drug capsules must clear strict bio-chemical approvals, and the supply of clean animal bone is itself limited.

So, the barrier to entry is real, even if the monopoly label is too strong. That is the honest version of the moat. On the demand side, Indian drug makers keep buying hard and soft capsules, and the newer collagen and nutraceutical trend gives Nitta a second leg to stand on through its Wellnex range. Demand here is steady rather than explosive, which suits a slow compounder just fine.

The 41% Profit CAGR: Why Margins Masked the Modest Top-Line Growth

Here is where the simple pitch needs a reality check. Nitta’s profits have grown substantially, but its sales have barely moved.

| Financial Year | FY21 | FY22 | FY23 | FY24 | FY25 | FY26 | 5Y CAGR |

| Sales (Rs cr) | 396 | 506 | 565 | 533 | 533 | 588 | 8% |

| EBITDA (Rs cr) | 45 | 64 | 114 | 124 | 105 | 136 | 25% |

| Net Profit (Rs cr) | 18 | 35 | 74 | 84 | 84 | 97 | 41% |

As we can see, sales grew at about 8% a year over five years, which is modest. Net profit, though, compounded at roughly 41%, climbing from Rs 18 cr to Rs 97 cr. EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) rose around 25% a year.

So where did all that profit come from? The answer is Margins. The operating margin jumped from 11% in FY21 to 23% in FY26. That is the whole story in one line. Nitta did not sell much more; it simply earned far more on what it sold.

One caveat is worth flagging. FY25 profit of Rs 84 cr leaned on Rs 23 cr of other income (money earned outside the core business). In FY26 the operating engine did the heavy lifting, with operating profit of Rs 136 cr, which is the healthier kind of growth.

Inside the 27% ROCE: Free Cash Flows, Capex, and Erased Debt

The company has a current Return on capital employed (ROCE), of about 27%, which is almost double of the current industry median of 14%. In simple words, for every Rs 100 of capital the company uses, it generates a profit of about Rs 27 on it, while its peers manage to make only Rs 14.

Borrowings have collapsed from Rs 80 cr in FY21 to just Rs 4 cr, giving a debt-to-equity ratio of 0.01. For practical purposes, the company is virtually debt free. Operating cash flow in FY26 was a strong Rs 122 cr. The company also spent heavily during the year, with a large investing outflow that points to fresh capacity coming up.

That is worth tracking, since new capex will weigh on near-term free cash flow even as it sets up future growth. One honest note keeps this in proportion. ROCE actually peaked near 35% in FY24 and has since cooled to 27%, so the company is past its very best year on this measure.

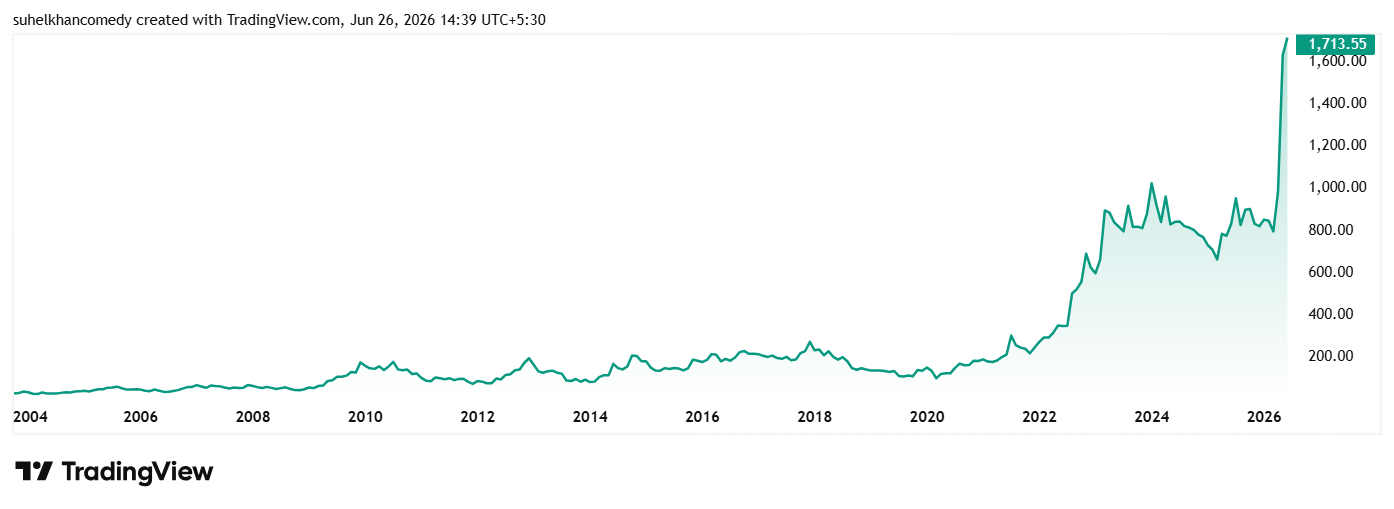

Is the 700% 5-Year Rally Fully Priced In at 16x Earnings?

The share price of Nitta Gelatin was around Rs 215 in June 2021 and as of closing in 25th June 2026 it was Rs 1,720 which is a 700% jump in 5 years. Rs 1 lakh invested in the stock 5 years ago would have been Rs 8 lakhs today.

Regarding the valuation, the company has a current PE of 16x against an industry median of 29x. The company barely made money for much of the past decade and even posted a loss in FY15, so its historical multiple is distorted and best left out. The cleaner point is simpler. Nitta was ignored and genuinely cheap for years. After doubling in the last twelve months, it is now reasonably priced rather than a bargain.

There is also a quieter risk under the hood. The animal material and processing chemicals are commodity inputs, and their prices move. A bad cycle on raw material costs could pull those shiny new margins back down faster than the sales line can cushion them.

#2 Narmada Gelatines: The Rs 286 cr minnow trading at single-digit earnings

Incorporated in 1969 and run out of a single plant in Jabalpur, Madhya Pradesh, Narmada Gelatines is the erstwhile Shaw Wallace Gelatines, renamed in 2002.

With a market cap of just Rs 286 cr, this is a true micro-cap, that makes ossein and gelatin. The promoters hold a tight 75% of the company.

One thing that any investor will see as soon as they look at the company has a current dividend yield of 2.2%, while the industry median is closer to just 0.3%. Let us look at the financials to see how the company manages this.

Replicating the Margin Surge

Narmada’s recent numbers rhyme with Nitta’s. Sales have crept up, while profitability has turned sharply.

| Financial Year | FY21 | FY22 | FY23 | FY24 | FY25 | FY26 | 5Y CAGR |

| Sales (Rs cr) | 135 | 157 | 191 | 182 | 189 | 215 | 10% |

| EBITDA (Rs cr) | 8 | 15 | 20 | 21 | 25 | 41 | 39% |

| Net Profit (Rs cr) | 8 | 12 | 15 | 15 | 17 | 28 | 29% |

These figures are on a standalone basis, because Narmada’s consolidated accounts on Screener only begin from FY25 and do not yet carry a five-year history. Sales grew about 10% a year. Net profit more than tripled, from about Rs 8 cr to Rs 28 cr.

A word of caution though. The five-year profit growth near 39% is a number that leans on a soft FY21. Measured cleanly from start to finish, profit compounded closer to the high-20s%. Either way the direction is the same. The operating margin climbed from 6% to 19%, and most of the jump landed in FY26 alone.

2.2% Yield and the Cushion of a ₹41 cr Investment Book

The balance sheet is reassuring for a company this small. Borrowings are just Rs 8 cr, debt to equity is about 0.06, and ROCE for the latest year is close to 28% (about 30% on a consolidated basis). The industry median as we saw in Nitta above is 14%.

The company also sits on an investment book of roughly Rs 41 cr, which is large relative to its size and acts as a cushion. Its current dividend yield is 2.2% in a market that averages 0.3%. The board has proposed Rs 11 per share for FY26.

For a micro-cap, that is a healthier profile than most. There is a flip side, though. With promoters owning 75%, the freely traded float is thin, so the price can swing hard on small volumes. The investment book and the dividend are the comfort here; the poor liquidity is the risk.

The 10x P/E Dilemma: Thin Liquidity Risks vs. Deep-Value Discounts

The share price of Narmada Gelatines was around Rs 185 in June 2021 and as of closing on 25th June 2026 it was Rs 473 which is a 155% jump in 5 years.

The stock has jumped 35% from Rs 350 to Rs 473 in the last 6 months, but is currently still trading at a discount of 16% from its all-time high of Rs 566.

As for the valuation, Narmada has a current PE of 10x against an industry median of 29x. That is cheap, full stop, and cheaper than both Nitta and the closest pure peer, India Gelatine and Chemicals, which trades near 10 times. A true 10-year median PE is, once again, not worth quoting, because the earnings base was too erratic for the multiple to mean much.

Set against a specialty chemicals industry trading in the thirties, the discount is striking. But cheap is rarely an accident. Narmada is tiny and thinly traded, runs a single plant, depends on commodity-priced inputs, and has a lumpy past. Its ROCE was stuck at just 4 to 5% as recently as FY17 and FY18. The margin surge is barely a year old.

Structural Shift or a Peak Cyclical Margin Play?

Strip away the hype and a clear, defensible picture remains. India’s gelatin makers sit in a regulated, capital-light niche that China cannot easily flood. They are debt free, they throw off cash, and they trade at a fat discount to the wider chemical sector. The parts of the original pitch that do not survive scrutiny are worth saying out loud.

There is no smart money cornering anything here, because no marquee investor owns either name. The word monopoly is too strong for what is really a small, protected club. And the eye-catching profit growth is a margin recovery riding on flat-ish sales, not a revenue machine.

So, the real question is narrow and important. Are these fat new margins structural, or just a good patch in a cyclical business? If the margins hold, both companies are cheap. If they slip back toward the single-digit operating margins of a few years ago, today’s low PE will look a lot less generous. Nitta is the quality leader that has already re-rated. Narmada is the deeper-value, higher-risk minnow. Neither is a free lunch, and both look better suited to a watchlist than a blind buy.

Disclaimer:

Note: We have relied on data from http://www.Screener.in and http://www.trendlyne.com throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Suhel Khan has been a passionate follower of the markets for over a decade. During this period, he was an integral part of a leading Equity Research organisation based in Mumbai as the Head of Sales & Marketing. Presently, he is spending most of his time dissecting the investments and strategies of the Super Investors of India.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article. The website managers, its employee(s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein.