For decades, India’s place in global health care was defined by one remarkable success: the production of generic medicines. Indian pharma companies mastered the art of low-cost manufacturing, developed one of the largest networks of USFDA-approved manufacturing plants outside the US, and grew to cater to about 20% of global generic drug demand.

The formula was simple but powerful: scale and regulatory credibility. This earned India the reputation as the “pharmacy of the world.”

But when it comes to manufacturing world-class medical devices, India lacks similar expertise. It has to depend on costly imports for sophisticated healthcare equipment primarily. Even for advanced diagnostic and surgical devices.

That is beginning to change. A new class of Indian manufacturers is quietly moving into global medical devices, not only by competing purely on cost, but by building capabilities in engineering precision, regulatory compliance, and long-cycle relationships with global healthcare firms.

It’s an emerging export story that looks very different from pharma-led success.

Why Medical Devices Are Suddenly Having Their Moment

The emergence of India’s medical device industry is not a result of a single catalyst. It is the convergence of several forces arriving roughly at the same time.

First Catalyst: Government Policy

In 2020, the government launched the Production Linked Incentive (PLI) scheme for medical devices, with an objective to reduce import dependence and encourage domestic manufacturing. The targeted categories included high-value products such as imaging systems, implants, anaesthesia equipment, and cardio-respiratory devices.

This push was further strengthened in 2023 with the National Medical Devices Policy, which aims to scale up the sector and secure a 10–12% share of the global market over the next 25 years.

This impact is already visible. By September 2025, 22 greenfield projects had been commissioned, producing devices across 55 categories, including MRI machines, CT scanners, mammography systems, and linear accelerators used in cancer treatment. Cumulative sales reached ₹12,344 crore, with exports accounting for nearly half at ₹5,869 crore.

The policy push could have much larger implications over the long term. In a joint report, Boston Consulting Group (BCG), the Association of Indian Medical Device Industry, and the Kalam Institute of Health Technology estimated that India could emerge as a $7 billion contract manufacturing hub for global medical device companies by 2035, provided the ecosystem continues to scale.

Second Catalyst: Geopolitics

For years, global healthcare supply chains relied heavily on China. The pandemic exposed the vulnerability of doing that. Since then, governments and companies have been diversifying their sourcing destinations.

The shift accelerated further in June 2025 when the European Union barred Chinese companies from participating in public medtech procurement contracts valued at €5 million or more. On the other hand, progress on the India-EU Free Trade Agreement has boosted prospects of long-term export growth to the region for Indian manufacturers.

Third Catalyst: Domestic Demand

India’s healthcare burden is structural and increasing. The country now has more than 100 million diabetics and another 136 million fall under a prediabetic condition, 315 million suffer from hypertension, and 450 million are overweight. According to a government study, around 100 out of 1 lakh people are diagnosed with cancer. This creates sustained and compounding demand for consumables, monitoring equipment, diagnostics, and treatment devices.

Together, these forces have created a window of opportunity that did not exist a decade ago. The question now is which companies are best positioned to take advantage of it.

Two Companies, Two Paths Into MedTech

The industry is still in its early stages, with only a handful of listed companies offering meaningful exposure to India’s emerging medtech opportunity. Among them, Poly Medicure and Shaily Engineering Plastics stand out because they represent two very different paths to building globally competitive healthcare manufacturing businesses.

Poly Medicure: The Veteran in the Space

Poly Medicure was founded in 1995 in Faridabad, in Haryana, to make single-use disposables: IV sets, infusion therapy products, catheters, dialysis consumables, blood collection systems, and vascular access devices.

These products are not highly technical, but need to comply with the strict medical standards of various countries. And, because they are disposable, their demand is recurring by nature.

Poly Medicure now exports to more than 125 countries and manufactures over 225 medical devices from 15 manufacturing plants across five countries.

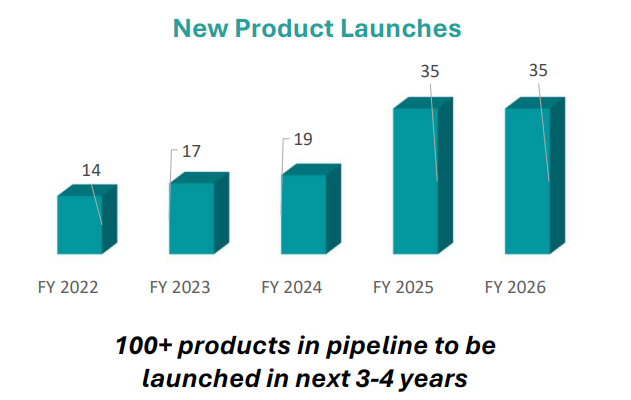

Its in-house product R&D department has more than 390 patents. Poly Medicure launched 35 new products across the group in FY26 and is planning more than 100 product launches in the next 3-4 years.

Poly Medicure New Product Launches

Now, let’s take a look at the key financial metrics

Poly Medicure: Key Financial Metrics

| Metrics | FY25 | FY26 | Change |

| Revenue (₹ cr) | 1,670 | 1,875 | 12.3% |

| Gross Profit Margin (%) | 66.7 | 68.1 | 140 basis points |

| EBITDA Margin (%) | 27.5 | 24.4 | -310 basis points |

| ROCE (%) | 23.0 | 16.0 | -700 basis points |

In FY26, the company reported revenue of ₹1,875 crores, with more than 65% coming from exports. The gross margin profile indicates it enjoys pricing power across its product ranges, which is resulting in higher earnings. However, the return ratios are impacted due to the acquisition of Italy’s Citieffe SRL in 2025, which is present in the orthopaedics segment.

The management is now looking beyond low-cost manufacturing and toward higher-value specialised categories.

Shaily Engineering: An IKEA Supplier Ended Up Inside the Obesity Revolution

Shaily Engineering was founded in 1987 in Halol, Gujarat, and was basically a precision injection moulding company, making complex plastic parts. Its customers included IKEA, Gillette, Procter & Gamble, Hindustan Unilever, and Corvi.

Over the last several years, Shaily has transformed itself into an increasingly important player in drug-delivery devices, particularly in the rapidly growing GLP-1 ecosystem.

GLP-1 drugs such as Ozempic and Wegovy have become some of the most commercially successful pharmaceutical products in the world, driven by growing demand for diabetes and obesity treatments. Every injectable therapy requires a delivery system, creating a parallel opportunity for manufacturers of pen injectors and related devices.

Shaily positioned itself directly in that value chain.

Shaily Engineering: Key Financial Metrics

| Metrics | FY25 | FY26 | Change |

| Revenue (₹ cr) | 787 | 991 | 20.5% |

| Gross Profit Margin (%) | 47.2 | 57.0 | 980 basis points |

| EBITDA Margin (%) | 22.7 | 29.0 | 630 basis points |

| ROCE (%) | 24.4 | 35.8 | 1140 basis points |

In FY26, Shaily Engineering reported 26% growth in total revenue, driven primarily by strong performance in its healthcare division. What began as a small strategic bet has now become the company’s fastest-growing business segment. Shaily Healthcare segment grew 139% to ₹393 crores in FY26.

Shaily Engineering Business Segment Performance

Healthcare contributed 21% of revenue in FY25, but its share has risen sharply to nearly 40% in FY26, reshaping the company’s overall revenue mix.

Both Poly Medicure and Shaily Engineering have a fundamentally different approach to tap the growing MedTech sector.

Poly’s strength lies in recurring hospital consumables with diversified end markets. Shaily’s growth is tied more closely to the evolution of the global drug-delivery ecosystem. That creates greater upside but also introduces greater concentration risk.

Poly Medicure vs Shaily Engineering: Valuation Comparison

Both companies are trading at premium valuations relative to the broader medical equipment industry, reflecting investor enthusiasm for India’s emerging medtech opportunity. However, the market is assigning very different expectations to each business.

PE Multiple Trends

| Company | P/E | 5-yr Median PE | Industry PE |

| Poly Medicure | 51.1 | 60.1 | 37.6 |

| Shaily Engineering | 81.2 | 58.9 | 25.9 |

A stock’s valuation is ultimately a bet on future earnings. The higher the valuation, the higher the growth investors expect.

Poly Medicure currently trades at around 51 times earnings. That is lower than its own five-year median PE of 60 times, suggesting the market has become slightly more cautious.

Even so, investors are still expecting strong growth. Management has guided FY27 revenue to around ₹2,300 crore, implying growth of more than 20%.

Shaily Engineering has a tough road ahead. The stock trades at more than 80 times earnings, well above both its historical valuation and industry average. Such a multiple suggests investors expect several years of rapid growth from the company’s healthcare business, particularly its drug-delivery device segment. The company has expanded manufacturing capacity, secured new contracts, and is building additional capacity in Abu Dhabi.

If these investments translate into sustained earnings growth, perhaps the valuation could be justified. But unlike Poly Medicure, there is less room for execution mistakes.

Here, Poly Medicure is being valued as an established medtech exporter with a long operating history. Shaily is being valued as a future growth story.

Can India Replicate Its Pharma Success in Medical Devices

India’s medtech opportunity is real. The Confederation of Indian Industry (CII) projects it could reach $50 billion by 2030, with exports alone reaching ₹1.7 lakh crore ($20 billion). But the sector still faces several challenges that cannot be ignored.

#1 Regulatory Complexity

Unlike many manufacturing industries, medical devices operate under stringent approval frameworks. Product recalls, compliance failures, or adverse regulatory findings can damage years of accumulated trust.

#2 Government Incentives could end

The PLI programme played an important role in accelerating investment, but those benefits will not last forever. Investors will eventually discover which businesses can sustain their economics without policy support.

#3 Technological Change

Shaily’s exposure to injectable GLP-1 therapies illustrates both the opportunity and the risk. Pharmaceutical companies are actively developing oral versions of these treatments. If adoption shifts meaningfully toward pills over time, demand for injectable delivery devices could evolve differently than current projections suggest.

#4 Ecosystem Constraints

India still imports many critical medical device components. Building a globally competitive industry requires not only successful manufacturers but also a deep supplier network, testing infrastructure, and specialised engineering talent.

Despite these challenges, the long-term opportunity remains significant. Global healthcare demand is rising, supply chains are diversifying beyond China, and India’s domestic healthcare market continues to expand. Companies such as Poly Medicure and Shaily Engineering are already demonstrating that Indian manufacturers can compete in global markets.

India’s share of global medical device exports remains small, at around 3% today. But that is precisely what makes the opportunity worth watching. If the country can replicate even a fraction of its pharmaceutical success, medical devices could become India’s next major healthcare export story. As the sector grows, add these stocks to your watchlist and monitor how they execute on their long-term growth plans.

Disclaimer:

Note: We have relied on data from www.Screener.in throughout this article. Only in cases where the data was not available, have we used an alternate, but widely used and accepted source of information.

The purpose of this article is only to share interesting charts, data points and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educative purposes only.

Deepan Datta has spent over a decade studying stocks and mutual funds. His passion is to uncover interesting stories in the financial markets and share them through his writings with investors at large. He is focused on delivering clear, easy to understand and research-backed insights. Deepan began his career as a Research Associate at S&P Global, where he developed a strong foundation in financial research and data analysis.

Disclosure: The writer and his dependents do not hold the stocks discussed in this article.

The website managers, their employees (s), and contributors/writers/authors of articles have or may have an outstanding buy or sell position or holding in the securities, options on securities or other related investments of issuers and/or companies discussed therein. The content of the articles and the interpretation of data are solely the personal views of the contributors/ writers/authors. Investors must make their own investment decisions based on their specific objectives, resources and only after consulting such independent advisors as may be necessary.