After years of anticipation, India’s largest stock exchange, the National Stock Exchange (NSE), has finally taken a crucial step towards its stock market debut by filing its Draft Red Herring Prospectus (DRHP) with market regulator SEBI.

The long-awaited move has naturally sparked comparisons with its listed rival, BSE, whose shares have delivered strong returns over the last few years.

As investors look ahead to one of India’s biggest IPOs, one question is dominating conversations – can NSE replicate the kind of wealth creation that BSE has brought about for its investors?

NSE Vs BSE: How the returns are likely to pan out

The comparison is hard to ignore. While both exchanges operate in the same business, market experts believe the comparison is far more complex than it appears. They argue that the two companies are at different stages of their journey, have different growth drivers and are being valued on different expectations.

So, does that make NSE a safer long-term bet, or does its sheer size limit the possibility of BSE-like returns?

Financialexpress.com spoke to market experts to understand whether investors should expect strong gains or steady compounding, whether an expected valuation discount makes the IPO attractive, and if NSE can strengthen its position after recent changes in the derivatives market.

Here’s a closer look.

A giant enters the market, but can it grow like a challenger?

One of the biggest reasons behind BSE’s strong stock performance has been its ability to grow rapidly from a relatively small base.

According to Vincent K A, Senior Research Analyst at Geojit Investments, BSE’s rally was supported by rapid expansion in its derivatives business, significant gains in market share and regulatory changes that worked in its favour.

He pointed out that NSE presents a completely different investment story.

“NSE is already a mature, dominant franchise with a high share of industry volumes and strong profitability. Its investment appeal lies in earnings stability, operating leverage and exposure to India’s long-term capital market growth,” he said.

Vincent further added, “While the stock may not deliver sharp multi-bagger returns in the near term, it offers the potential for steady, compounding returns, supported by sustained market leadership, resilient cash flows, and a superior margin profile.”

Shweta Rajani, Associate Director at Anand Rathi Wealth, echoed a similar view but added that the difference in size cannot be ignored.

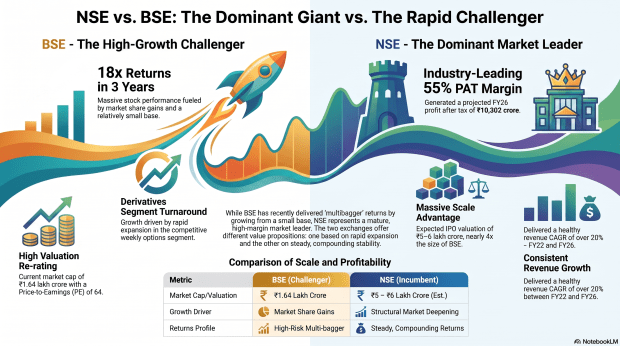

She noted that, “In recent years, BSE has delivered a significant performance with 18x returns in the last 3 years and 4x returns in the last 2 years, with a current market cap of 1.64 lakh cr at a PE of 64. On the other hand, NSE is expected to launch its public offering with an expected valuation of Rs 5–6 lakh crore, which roughly translates into 3.5 to 4x BSE’s market cap at IPO.”

That sheer size, she said, creates a natural base effect.

“BSE’s multibagger performance was primarily driven by strong market share gains in the weekly options segment, strong earnings acceleration, and a significant valuation re-rating from a relatively low base, whereas NSE is already India’s dominant exchange. It generated a FY26 profit after tax of Rs 10,302 crore, operates with an industry-leading PAT margin of around 55%, and has delivered a healthy revenue CAGR of over 20% between FY22 and FY26,” she added.

Because of this, Rajani believes NSE has comparatively less room to generate BSE-like returns. She noted, “NSE has less scope to deliver BSE-like returns due to it’s larger base effect & stage of business cycle, however, NSE will likely grow with steady top-line growth with strong cashflows and market leadership.”

Sunil Jain, Head of Retail Research at Nirmal Bang, also believes NSE’s scale changes the investment equation.

He explained that while BSE benefited from a low base, earnings expansion and successful execution in equity derivatives, NSE is entering the listed space as India’s dominant exchange with leadership across cash markets, futures and primary market businesses.

Jain added, “NSE, however, is entering the market as India’s dominant exchange with over three times BSE’s operating revenue, leadership across cash, futures and primary markets, and a much larger earnings base. While this scale makes BSE-like multi-bagger returns less likely in the near term, NSE offers a more predictable and sustainable long-term growth profile supported by the structural deepening of India’s capital markets.”

Ratiraj Tibrewal, CEO of Choice Wealth, perhaps summed up the comparison in the simplest way.

He said investors should avoid comparing the two companies as though they represent the same opportunity.

“The big gains seen in a smaller exchange came from a specific situation. It was gaining market share in options from a low base, profits were rising quickly and there was a turnaround story behind it. A large, established exchange works differently. It grows steadily through an already strong position, healthy margins and the fact that most trading already happens there, ” Tibrewal said.

According to him, one investment is based on rapid expansion while the other is built around steady compounding. Neither is better than the other – they simply appeal to different types of investors.

Does a lower valuation automatically make NSE attractive?

Another question that has emerged ahead of the IPO is whether NSE could list at a valuation discount to BSE because of recent regulatory changes that have affected derivatives trading.

Experts, however, caution investors against looking only at valuation multiples.

Vincent believes the current comparison between the two exchanges has been influenced by BSE’s stronger recent growth trajectory, creating a temporary divergence.

He expects this gap to narrow over time.

According to him, the recent pressure on NSE’s trading volumes and margins appears largely temporary, driven by policy interventions and one-off costs. He noted, “The current relative positioning of NSE vis-à-vis BSE appears distorted, influenced by BSE’s stronger recent growth trajectory, which may create some near-term divergence in stock performance.”

“The long-term investment thesis remains anchored in NSE’s dominant market leadership, superior profitability and exposure to India’s structural capital market growth,” he said.

Future re-rating, he added, will depend on several factors including recovery in trading volumes, margin normalisation after regulatory costs, returns from recent technology investments and the exchange’s ability to maintain leadership in derivatives.

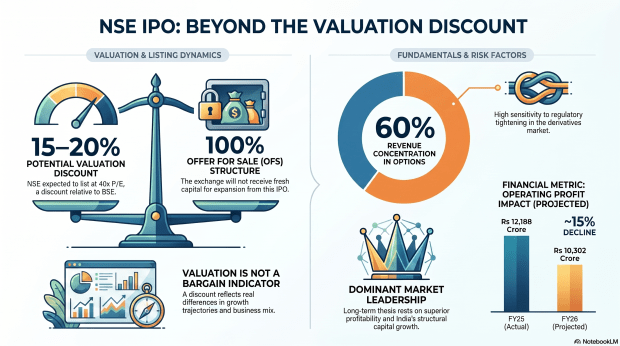

Rajani from Anand Rathi Wealth also acknowledged that NSE could list at nearly 40 times earnings. She noted, “NSE expected to launch its IPO with a market cap of 5 lakh cr, which translates into 40x PE, which indicates a 15 to 20% discount to current BSE valuation multiples.”

However, she warned investors against assuming that a discount automatically makes the IPO attractive.

She highlighted that NSE’s FY26 profit declined around 15% year-on-year to Rs 10,302 crore from Rs 12,188 crore in FY25, largely because of regulatory changes affecting the derivatives market.

She further pointed out that nearly 60% of NSE’s operating revenue still comes from options trading, making it sensitive to any future regulatory tightening.

Another aspect investors should remember, she said, is that the IPO is entirely an Offer for Sale (OFS), meaning the company itself will not receive fresh capital for expansion.

For long-term investors, Rajani believes it may be wiser to closely monitor business performance over the coming quarters before drawing conclusions about the long-term impact of recent regulatory changes.

Sunil Jain also believes valuation should never become the sole investment argument.

“A valuation discount alone should not be the investment thesis; it needs to be viewed alongside earnings quality, business fundamentals and growth,” Jain added.

He noted that despite the regulatory changes, NSE continues to dominate across most trading segments with diversified revenue streams and robust profitability.

He further noted, “If the IPO is priced at a reasonable discount to BSE while reflecting these strengths, it could offer an attractive risk-reward proposition for long-term investors.”

Ratiraj Tibrewal made a similar point.

According to him, an exchange’s valuation depends on factors such as the stability of its income, the diversity of its revenue streams, regulatory exposure, margins and future growth potential.

” When two exchanges are valued differently, that gap usually reflects real differences in their growth and their business mix. It does not automatically mean one is cheap and the other is expensive. So one should be cautious about treating a lower valuation as a bargain by itself. What really matters is what one is paying compared to how dependable the earnings are,” added Tibrewal.

He added that until the IPO pricing is officially announced, debates around whether NSE is cheap or expensive remain premature.

Can NSE reclaim its derivatives dominance?

Perhaps the biggest question for investors is whether NSE can regain the market share it has lost in equity options after recent regulatory changes, or whether BSE will continue enjoying a growth premium.

Vincent added, “BSE’s recent gains in the equity options segment have been driven primarily by regulatory-led market share shifts and a low-base effect, rather than a structural displacement.”

According to him, NSE’s moderation in derivatives activity should also be viewed in context, as it came after an exceptionally strong period.

He expects NSE to retain overall leadership because of its deep liquidity, established participant ecosystem and dominant market position.

While BSE may continue reporting stronger growth rates in the near term, Vincent believes those growth numbers are likely to normalise over the medium term.

Rajani offered a more detailed explanation of the competitive landscape.

She acknowledged that BSE’s success in Sensex and Bankex weekly options significantly boosted trading activity and earnings. The exchange reported around 88% growth in FY26 profit after tax and delivered an impressive three-year PAT CAGR of about 124%.

A major contributor, she said, was SEBI’s rationalisation of weekly expiries, which changed the competitive dynamics of the options market.

Even so, Rajani believes investors should distinguish between market share gains in one segment and leadership across the entire exchange business.

She noted that NSE still commands nearly 93% of cash market turnover, almost 100% of equity futures trading, over 99% of currency futures and close to 75% of equity options premium turnover.

She noted, “Going forward, NSE is unlikely to fully regain the monopoly it once enjoyed in weekly index options due to the expiry framework being driven by regulation rather than competition. While NSE is expected to launch new products, such as electricity derivatives and the expansion of GIFT City to diversify its revenue streams, they may not completely offset the structural changes in the options market.”

Sunil Jain also believes BSE deserves recognition for strengthening its position in equity options, adding, “BSE has clearly emerged as a stronger competitor in equity options and deserves credit for improving its market position.”

However, he pointed out that NSE continues to dominate the broader exchange ecosystem through its leadership in cash equities, futures, capital raising and overall revenues.

Its deeper liquidity and stronger network effects continue to give it a competitive advantage.

According to Jain, “Going forward, BSE may continue to enjoy a growth premium, but NSE is well positioned to maintain its leadership while both exchanges benefit from the long-term expansion of India’s capital markets.”

Ratiraj Tibrewal believes the recent shift should not be viewed as a simple contest with one clear winner.

“The recent rule changes in the derivatives market, fewer weekly expiries, larger lot sizes, stricter labelling, actually changed the size and shape of the entire options market. So part of that shift in market share is really about the new rules, not a permanent change in who leads. And when a smaller player gains ground from a low base, it will naturally look like the faster grower, which is quite normal,” Tibrewal said.

He added that whenever a smaller player grows from a low base, its growth naturally appears much faster.

At the same time, the advantages enjoyed by the market leader remain significant.

Tibrewal noted, “Trading generally concentrates where liquidity already exists, and that is difficult to disrupt, especially in cash markets and derivatives.”

According to Tibrewal, India’s rapidly expanding investor base provides enough room for both exchanges to grow, although they may continue growing at different speeds and attract different categories of investors.

What investors need to focus

While comparisons between NSE and BSE are inevitable, analysts largely agree that investors should not expect history to repeat itself in the same way.

BSE’s spectacular rally was driven by a combination of low-base growth, market share gains, earnings acceleration and valuation re-rating. NSE, on the other hand, begins its listed journey as India’s largest and most profitable exchange with an already dominant position across several market segments.

That may reduce the possibility of spectacular short-term returns, but it also provides a business built on leadership, scale, stable earnings and long-term participation in India’s growing capital markets.

For investors evaluating the upcoming IPO, experts suggest looking beyond headline valuation comparisons and focusing instead on business fundamentals, regulatory developments and the exchange’s ability to sustain its leadership as India’s financial markets continue to evolve.

Disclaimer: This market analysis column provides comparative insights based on individual market expert opinions regarding the upcoming NSE IPO and its financial performance relative to BSE. The views, projections, and estimates expressed herein belong solely to the independent research analysts and wealth management professionals quoted and do not represent the editorial stance of this publication. This content is for informational purposes only and does not constitute a prospectus, an offer, an invitation, or a solicitation to buy, sell, or subscribe to any securities or IPO shares. Financial markets carry inherent structural, regulatory, and market risks. Past performance of comparable market entities is not a reliable indicator of future results. Investors are strongly advised to read the official Draft Red Herring Prospectus (DRHP) carefully approved by SEBI and consult with a SEBI-registered investment advisor or qualified financial consultant to assess their risk appetite before making any investment decisions. This disclaimer has been generated using AI to support user well-being and responsible content consumption.